UPDATE: It looks like this issue may be limited to a single carrier in New Mexico; I've changed the headline and graphic accordingly...but it might be an issue in other states as well; if so I may have to change it back again...

Insurers That Filed Wrong Rates Told By CMS They Can't Sell Plans Through Mid-November

An issuer whose final CMS-approved rates don’t account for the loss of cost-sharing reduction payments is being told by the agency that they won’t be able to sell plans until healthcare.gov data is refreshed– even though this would mean the carriers are even more crunched for time to sell their plans during the shortened open enrollment period.

The very first bullet starts off ripping on the 37% average rate hike on benchmark Silver plans...

Benchmark Premiums: The average monthly premium for the second-lowest cost silver plan (SLCSP), also called the benchmark plan, for a 27-year-old increased by 37% from plan year 2017 (PY17) ($300) to PY18 ($411).

Premium Growth: For the first time, annual growth in the average monthly premium available to a 27- year-old for the SLCSP, at 37%, outpaced that of the lowest-cost plan (LCP), at 17%.

Of course, there's pretty obvious reason for that: Trump's cut-off of Cost Sharing Reduction (CSR) reimbursement payments. The ASPE report does go into this, but not until Page 6. Meanwhile, it's immediately undermined anyway (at least regarding subsidized enrollees) in the very next bullet:

With the 2018 Open Enrollment Period coming up just 5 days from now, it's time to put this to bed: After 6 months of painstaking research and analysis, I've compiled a comprehensive analysis of the weighted average rate changes for unsubsidized ACA-compliant individual market policies in 2018, including both the on- and off-exchange markets. It's already been confirmed by a different analysis by healthcare consulting firm Avalere Health, which used a completely different methodology to arrive at the exact same conclusion: The national average increase isbetween 29-30%, ranging from as low as a 22% average premium drop in Alaska(thanks to their successful reinsurance program) to as high as a painful 58% increase in Virginia.

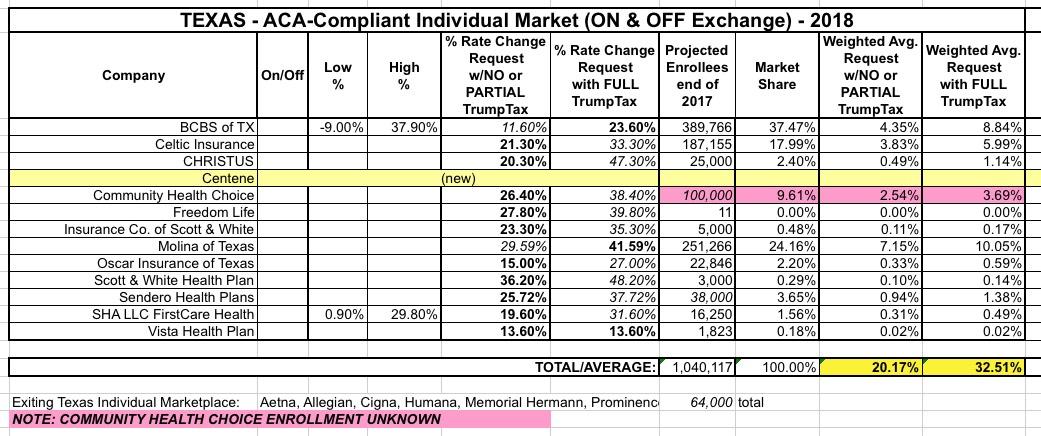

I've saved Texas for last because, frankly, I haven't been able to make heads or tails out of their actual average rate increases for next year (and unlike smaller states which might not move the needle on the national average anyway, Texas has one of the largest populations in the country, so a substantial error here can also impact the national numbers significantly).

Back in early August, I pieced together a rough average of the requested rate increases for the Lone Star State of around 20% if CSR payments are made or 32.5% if they aren't:

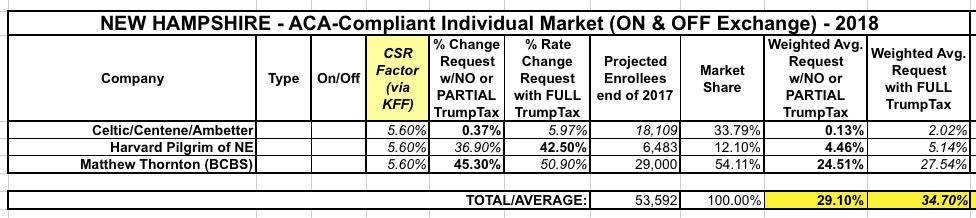

As noted earlier today, I've now managed to plug 48 states (plus DC) into my 2018 Rate Hike Project spreadsheet. This leaves just two states missing: New Hampshire and Texas. I'm still waiting to clarify some things for each, so this analysis could still change, but I really want to wrap this up, so here's what I have for New Hampshire right now:

When I first ran the numbers for New Hampshire'srequested 2018 rate increases, it seemed pretty straightforward: 3 carriers on the individual market. 2 listed rate changes assuming CSRs would be paid; one assumed they wouldn't. This gave the following:

With only 5 days to go before the launch of the 2018 Open Enrollment Period, time is rapidly running out for me to wrap up my 2018 Rate Hike Project. I started this, as I have for 3 years now, back in late early May with the very first requested rate changes out of Virginia, and have been tracking all 50 states as the summer and fall have passed, following every twist and turn of the insane repeal/replace circus in Congress, Trump's bloviating and blathering about "blowing things up" and "letting Obamacare explode", the last-ditch "Graham-Cassidy" sideshow and everything else, right up to and through Trump lowering the boom on cutting off CSR reimbursement payments.

I'm still missing final 2018 rate data for 6 states, but in the meantime I'm also doing some cleanup of some of the states I thought I already had final data for. Today both my home state of Michigan as well as Washington State released their official, approved increase tables.

However, I do give the Michigan Dept. of Insurance & Financial Services huge credit for making it incredibly easy for me to plug their data in. Look at that...they list all carriers, whether they sell on or off exchange, the exact average rate increases, and even include the number of affected enrollees, which is usually the hardest number for me to track down. Thanks, MI DIFS!!

Still, I don't like loose ends, and those 8 missing states are bugging me, so I still want to fill them in for completeness' sake. The only big state remaining is Texas, but I'm also missing Alabama, Hawaii, Iowa, Missouri, New Hampshire, Oklahoma and Wyoming.

A week or two later, the ASPE department of CMS issued a report putting the average at 22%...except that they were missing 7 states, only included benchmark Silver plans and didn't include off-exchange policies. The missing states had higher average premiums on the whole, so I'm pretty sure the actual overall average was pretty close to 24-25% in the end.

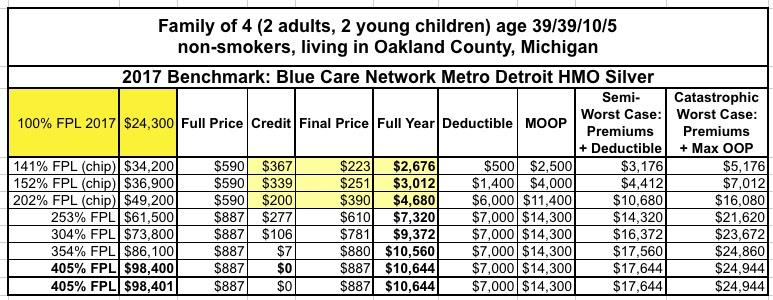

Let's suppose that you and your spouse were 39 years old last fall, and you have two young children. None of you smoke, and you live in Oakland County, Michigan. Let us further suppose that you decided to enroll your family in a standard Silver policy via the federal ACA exchange, HealthCare.Gov. Blue Cross Blue Shield of Michigan is the biggest carrier in the state, and Blue Care Network is their HMO division, so you decide to go with them.

How much of a tax credit will they receive, and how much would they end up paying for 2017 at different income levels after applying tax credits?

Several of the states operating their own ACA exchanges have already had their 2018 Window Shopping tools up and running for several weeks now, including Covered California, Your Health Idaho and the Maryland Health Connection, so this really shouldn't be that big of a deal, but given the insanity and uncertainty surrounding this years' Open Enrollment Period and especially the fact that HealthCare.Gov is responsible for 39 states (while being operated by the federal government under the thumb of an openly-hostile Trump Administration), it's pretty important news regardless.

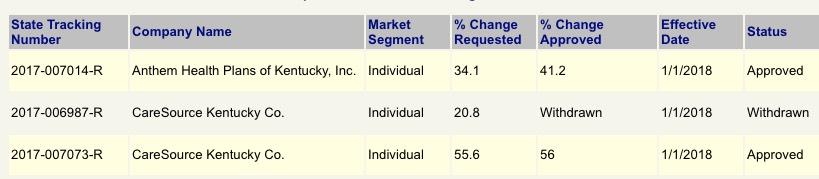

When I ran the requested rate hike numbers for Kentucky in early August, it looked like the only 2 carriers participating in the individual market next year (CareSource and Anthem BCBS) were asking for pretty hefty hikes of around 30.8% on average...and that assumed CSR reimbursement payments would be made next year. If they aren't, based on the Kaiser Family Foundation's estimates, I tacked on an additional 13.8% for a requested average of 44.3%. Ouch.

Washington, D.C. – The District of Columbia Department of Insurance, Securities and Banking (DISB) approved health insurance plan rates for the District of Columbia’s health insurance marketplace, DC Health Link, for plan year 2018.

Insurers filed their initial rates with the Department in May. Since then, DISB engaged in its rate review process resulting in two out of the four insurers revising their rates down from their initial filings, one as much as half of what was proposed. The Department also held a public hearing during the rate review process to allow residents to provide input in the rate review process.

Back in August, I posted a rough analysis of the requested rate increase situation for Wisconsin's individual market carriers. However, I cautioned at the time that I was missing the enrollment market share numbers for four of the carriers (Aspirus, Compcare, Wisconsin Physician Service and WPS), and therefore had to guess at how the rate hikes for those carriers would impact the statewide average. I estimated the numbers assuming CSR payments are made at 21.7%, and from that assumed the impact of CSR reimbursements not being made would be around 7.8 additional points being tacked onto the average.

A couple of weeks ago, the state insurance commissioner announced the approved rate increases. The good news is that I overestimated on the "CSRs paid" front. The bad news is that I underestimated on the "CSRs not paid" front: It's actually 20% and 36% respectively:

On November 10, 2016, at 4:30 in the morning, I was still in a bit of a dazed state trying to absorb the reality that a racist, misogynistic, xenophobic con-artist sexual predator moron was about to become the next President of the United States. We were 9 days into the 2017 Open Enrollment Period, and I realized that there was absolutely no way of knowing what sort of impact the election results might end up having on how many people would sign up for coverage.

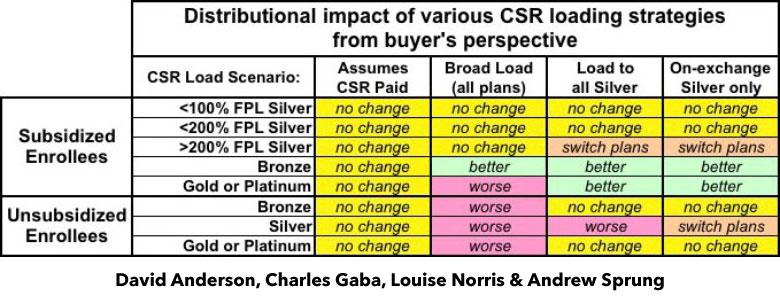

I've written a lot in recent weeks about the real world impact that Trump cutting off CSR reimbursement payments will have on 2018 premiums in various states depending on how they choose to load the additional cost. As I've noted repeatedly, there are basically four strategies they can take: They can assume the payments will continue; they can spread the load across all ACA-compliant policies; they can load all of the cost onto Silver plans only; or they can load all of the cost onto on-exchange Silver plans only, while also creating (if one doesn't exist) a special off-exchange-only Silver plan as a backstop for unsubsidized Silver enrollees (aka the "Silver Switcharoo").

Up until a week ago, the possibility of Donald Trump pulling the plug on Cost Sharing Reduction reimbursement payments was a looming threat every day. While it hadn't actually happened yet, most of the state insurance commissioners and/or insurance carriers themselves saw the potential writing on the wall and priced their 2018 premiums accordingly (or at the very least prepared two different sets of rate filings to cover either contingency).

A few spread the extra CSR load across all policies, both on and off the exchange. This seems like the "fairest" way of handling things on the surface, but is actually the worst way to do so, because it hurts all unsubsidized enrollees no matter what they choose for 2018 and can even make things slightly worse for some subsidized enrollees in Gold or Platinum plans.

Our timing couldn't have been more fortuitous: Less than 48 hours after we posted the piece, Donald Trump announced that, sure enough, he's finally following through on his threat to pull the plug on CSR payments, effective immediately.

The approved rate increases for NJ were just released, and the numbers appear to be pretty close to that, if a bit higher: 9.9% and 22.0% respectively.

Truth be told, I only have the hard numbers for the exchange-based carriers...and even those aren't technically official; they come from this NJ.com article:

TRENTON -- New Jersey residents who bought their own health coverage from Horizon Blue Cross Blue Shield through the Affordable Care Act could pay an average of 24 percent more next year, according to state-approved rates released on Tuesday.

Horizon is one of three insurance companies in New Jersey participating in the Obamacare marketplace in 2018. But it is the most dominant, insuring 72 percent of the 244,000 individual policy holders this year.

I first looked at Rhode Island's proposed rate hikes back in early July. At the time, the average increase for the two carriers participating in RI's individual market was 10.5% assuming CSR reimbursement payments are guaranteed for 2018. If they weren't guaranteed, however, I estimated at the time that an additional 19 percentage points would be added into the mix, based on an estimate by the Kaiser Family Foundation.

However, I realized a little later on that I was misinterpreting KFF's analysis; they were referring to how much they estimated silver plans would go up due to the lost CSR funds, not all metal levels. Furthermore, for Medicaid expansion states (which includes Rhode Island) they estimated the average was only 15%.. Based on these factors, the impact across the board on Rhode Island should have only been around 10.3%.

Way back in May, Blue Cross Blue Shield of North Carolina submitted their initial 2018 rate requests to the state insurance department, and noted at the time that they'd normally only be requesting an 8.8% average rate increase...but that due specifically to Donald Trump's threat to cut off CSR reimbursement payments, they were asking for a 23.3% increase instead. I noted that this meant that about 60% of their increase request was caused by Trump's CSR threat.

Then, in August, they gave a somewhat more positive news update: They were lowering their requested rate hike to 14.1%. Basically, their latest numbers had come in and the balance sheet was doing quite a bit better than they had previously thought:

Blue Cross said May 25 that the 22.9 percent rate increase was based on the subsidies ending, along with claims data from the first quarter of 2017. It projected an 8.8 percent rate increase with the subsidies remaining in place.

OK, I was in on the Breaking News a few hours ago; unfortunately a) I had to pick my kid up from school and b) our power went out. (I'm currently online via our generator). As a result, I haven't actually posted anything here at the site about the just-announced Alexander-Murray deal until now.

Sen. Lamar Alexander says he and Sen. Patty Murray have reached a deal to fund the Affordable Care Act's cost-sharing subsidies in exchange for giving states more regulatory flexibility with the law. Shortly after Alexander announced the deal to reporters, President Trump called it a "good short term solution."

OK, right off the bat: I guarantee you that Donald Trump (who just yesterday ranted about how "Obamacare is 'dead' and 'gone') doesn't have the slightest friggin' clue whether this (or any other deal) is "good" or "bad". He hasn't read it and he wouldn't understand any of it if he tried to anyway.

Medica Leaving North Dakota Individual Health Insurance Exchange in 2018

Post date: Sep 28, 2017

BISMARCK, N.D. – Insurance Commissioner Jon Godfread today confirmed that the Insurance Department was informed late Wednesday, Sept. 27, that Medica does not intend to sign an agreement with the federal government to offer coverage on the Affordable Care Act (ACA) Exchange for their individual health insurance in North Dakota for 2018.

“We have had numerous conversations with Medica over the course of the past few months, and given the uncertainty that currently exists around cost sharing reductions, they are unable to move forward in the Federal Exchange,” Godfread said.

Things were looking pretty dicey for two of Montana's three insurance carriers participating on the individual market the past few days. One of the three, Blue Cross Blue Shield, saw the writing on the wall regarding Cost Sharing Reductions (CSR) likely being cut off and filed a hefty 23% rate hike request with the state insurance department. The other two, however (PacificSource and the Montana Health Co-Op, one of a handful of ACA-created cooperatives stll around, assumed that the CSR payments would still be around next year and only filed single-digit rate increases.

I'm not going to speculate as to the reasons why they both did so when it was patently obvious that having the CSRs cut off was a distinct possibility, although I seem to recall the CEO of the Montana Co-Op said something about their hands being tied since CSR reimbursement payments are legally required, after all. Basically, it sounds like he was genuinely trying to avoid passing on any more additional costs to their enrollees than they had to.

Pennsylvania is the first state which has released their approved 2018 rate hikes since Donald Trump officially pulled the plug on CSR reimbursement payments last Friday. It's also one of just 16 states which had yet to do by then. Most of the remaining states are small or mid-sized, so plugging Pennsylvania into the 2018 Rate Hike Project leaves just Texas, North Carolina and New Jersey as missing states with more than 8 million residents.

Insurance Commissioner Announces Single-Digit Aggregate 2018 Individual and Small Group Market Rate Requests, Confirming Move Toward Stability Unless Congress or the Trump Administration Act to Disrupt Individual Market

IMPORTANT: I need to stress that I am not in any way supportive of having CSR reimbursement payments cut off. I've written dozens of blog posts for the past year and a half about the danger this poses and I've repeatedly explained why this is a reckless, dangerous move by Donald Trump, I've even repeatedly noted how incredibly easy it would be to resolve the issue with a simple, one paragraph bill. Having said that, assuming the payments do stop being made, this is an explainer of how to turn it into a "lemonade out of lemons" situation for as many people as possible. Make no mistake, however: Millions of people will still be hurt by this...just not the people Trump thinks he's hurting.

As in most states, the Michigan Dept. of Financial Services, seeing the potential writing on the wall, sent out a memo to all individual market insurance carriers instructing them to submit two different sets of rate filings for 2018: One assuming CSR payments would continue, the other assuming they won't:

President Donald Trump plans to cut off subsidy payments to insurers selling Obamacare coverage in his most aggressive move yet to undermine the health care law, according to two sources.

The subsidies, which are worth an estimated $7 billion this year and are paid out in monthly installments, may stop almost immediately since Congress hasn’t appropriated funding for the program.

Covered California Keeps Premiums Stable by Adding Cost-Sharing Reduction Surcharge Only to Silver Plans to Limit Consumer Impact

In the absence of a federal commitment to continue funding cost-sharing reduction (CSR) reimbursements through the upcoming year, Covered California health insurance companies will add a surcharge to Silver-tier products in 2018.

However, because the surcharge will only be applied to Silver-tier plans, nearly four out of five consumers will see their premiums stay the same or decrease, since the amount of financial help they receive will also rise. Those who do not get financial help will not have to pay a surcharge.

Financial help means that in 2018, nearly 60 percent of subsidy-eligible enrollees will have access to Silver coverage for less than $100 per month — the same as it was in 2017 — and 74 percent can purchase Bronze coverage for less than $10 per month.

California and individual markets across the nation still need a clear commitment that the federal government will continue to make CSR payments to promote lower premiums, save taxpayer money and ensure health insurance companies participate.

Note: This post is a joint effort with colleagues who have closely tracked the CSR chaos induced by Trump and Republicans in Congress. Dave Anderson is a former health insurance analyst, now a healthcare scholar at Duke, and a blogger at Balloon Juice; Louise Norris is co-owner with her husband Jay of a unique health insurance brokerage for individual market customers, and a top source of marketplace information and analysis at her own blog as well as at healthinsurance.org and elsewhere. Andrew Sprung writes about healthcare policy on his blog, xpostfactoid, as well as at healthinsurance.org and other publications.

In August I reported that the three individual market carriers in West Virginia (CareFirst, Highmark BCBS and Health Plan of the Upper Ohio Valley) were requesting average rate hikes of around 17.8% assuming CSR payments are made or 27.8% assuming they aren't.

The West Virginia Insurance Commission approved rate increases for Highmark West Virginia and CareSource Insurance’s services sold in the “Obamacare” exchange.

MetroNews learned Tuesday premiums for Highmark West Virginia will increase by 25.6 percent, while CareSource Insurance will have a 19.6-percent increase in its rate.

The article goes on to falsely conflate the 2017 and 2018 rate increases, however:

I noted back in August that there will only be one insurance carrier offering policies on the Nebraska individual market next year (Medica), with Blue Cross Blue Shield dropping out.

Medica has 35,269 members on their ACA-compliant individual market plans in 2017. But all of the current Aetna enrollees, as well as off-exchange BCBSNE enrollees, will need to switch to Medica plans at the end of 2017, as Medica will be the only insurer offering plans in Nebraska’s individual market for 2018.

A week or so ago, there was some confusing news about how Donald Trump may or may not be planning on signing a new healthcare-related executive order. I didn't write about it earlier because at first it sounded like he was talking about a meaningless "sell across state lines" decree...meaningless because the ACA already allows carriers to sell ACA-compliant policies across state lines, as long as the states in question sign onto an interstate compact.

Ambetter ("Sunflower State") is new to the state, so there's no "rate hikes" to speak of. My confusion was regarding BCBSKS, which is already on the KS exchange but didn't appear to submit any actual "rate change" request last time I checked. Louise Norris has cleared up this mystery:

On October 11, 2013, I posted a diary over at Daily Kos citing CNBC report which made it sound like over 84,000 people had managed to enroll in healthcare policies via the ACA exchanges in the first week and a half, in spite of the massive technical problems at HealthCare.Gov and some of the state exchanges.

It would later turn out that the numbers cited in the article were pretty misleading; while a few states which ran their own exchange websites were indeed off to a good start, some of the data only referred to applications (not actual plan selections), while the numbers out of the main website (HealthCare.Gov) were pathetic at first due to the technical mess (it turned out only six people actually slogged their way through the entire process at HC.gov on Day One).

In U.S. politics, the Hyde Amendment is a legislative provision barring the use of federal funds to pay for abortion except to save the life of the woman, or if the pregnancy arises from incest or rape. Legislation, including the Hyde Amendment, generally restricts the use of funds allocated for the Department of Health and Human Services and consequently has significant effects involving Medicaid recipients. Medicaid currently serves approximately 6.5 million women in the United States, including 1 in 5 women of reproductive age (women aged 15–44).

...The 2016 platform marked the first time the Democratic platform had an explicit call to repeal the Hyde Amendment. On January 24, 2017, the House of Representatives passed H.R. 7, which, according to the press office of Speaker Paul Ryan, "makes the Hyde amendment permanent."

The Cost Sharing Reduction (CSR) payment controversy has been sucking up a huge amount of oxygen over the past 9 months. Most of this is due to Donald Trump repeatedly threatening to cut off the monthly reimbursements to insurance carriers since January, but some of the concern was already there before he even took office. Why? Because the whole reason the CSR payments are at risk of being discontinued in the first place is a federal lawsuit filed by John Boehner on behalf of the House Republican Caucus back in 2014.

The case slowly ground it's way through the judicial process mostly under the radar for a couple of years. Law experts like Nicholas Bagley of the University of Michigan took the view that the case actually had some merit to it on the surface, but should still be shot down due to a lack of standing:

Highmark Blue Cross Blue Shield's 2018 Affordable Care Act marketplace prices will rise by 25 percent, less than it had requested.

The insurer had asked the Department of Insurance for a 33.6 percent increase in June, one month after Aetna announced it would pull out of Delaware's marketplace. The withdrawal will end its coverage of 11,854 Delawareans and make Highmark the only insurance provider in the Delaware marketplace.

...Right now, about 27,000 Delawareans have health insurance through the marketplace. The rate increases will not affect Medicare, Medicaid or coverage by private and government employers.

...Highmark's rate request was based on the uncertain future of Obamacare, especially whether the federal government would or would not enforce the mandate that makes uninsured people either opt in or pay a tax penalty, or continue to make the cost sharing reduction payments, which helps reduce prices for low-income Americans.

NY State of Health Enrollment Tops 4 Million

Open Enrollment for Qualified Health Plans to Begin November 1, 2017

ALBANY, N.Y. (October 5, 2017) - NY State of Health, the state's official health plan Marketplace, today announced that more than 4 million people have signed up for health insurance through the Marketplace. Enrollment in the Essential Plan continues to grow, with more than 680,000 enrolled. The Marketplace is ready for its 5th Open Enrollment Period, which begins November 1, 2017 and has been extended to January 31, 2018, beyond the federal deadline of December 15, 2017, to allow New Yorkers sufficient time to enroll.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Here's something refreshing: U.S. Senator Angus King (I-ME) giving a floor speech in which he lays out at least a half a dozen different types of deliberate sabotage of the ACA's upcoming 2018 Open Enrollment Period by the Trump Administration to date. Start at 4:30:

On Senate Floor, King Discusses “Sabotage” of the Affordable Care Act

“Why does anyone want to have fewer people with insurance?”

WASHINGTON, D.C. – U.S. Senator Angus King (I-Maine) today spoke on the floor of the U.S. Senate to address threats to the Affordable Care Act’s healthcare marketplace.

“I’m rising today in sadness, but also in some anger because there’s a lot of talk about the Affordable Care Act collapsing,” said Senator King in his speech. “Mr. President, it is not collapsing – it’s being mugged. It’s being stabbed in the back. It’s being sabotaged, deliberately and consciously by the actions of the Administration. And I want to emphasize – this isn’t about ideology, it’s not about politics… this is about people.

Back in July, I had originally estimated the requested rate increases for New Mexico to average roughly 24.2% with partial Trump Administration sabotage or 37.2% with full sabotage (no CSR payments, full mandate enforcement threat). However, figuring out NM's approved rate hikes is proving to be frustrating.

On the one hand, they have a handy database lookup tool right there on the NM Insurance Dept. website, and they even have the actual premium amount listings for every plan from every carrier in every rating area available. Unfortunately, the premium listings don't give a year over year comparison (or an average percent increase), and the database tool seems not to have been fully updated as of this writing, making it kind of useless. I have some info for a couple of the individual carriers but even that's a bit confusing.

To the best of my knowledge, there are only 2 insurance carriers offering ACA-compliant insurance policies in Arizona next year: Blue Cross Blue Shield of AZ and Centene (branded as HealthNet).

Back in early August, BCBSAZ announced that they were asking for a relatively modest 7.2% rate increase next year in the 13 counties (out of 15 total) where they were offering individual plans. They also explicitly stated that if it weren't for their concerns over whether or not the Trump Administration would guarantee reimbursing their CSR expenses, they'd be keeping the 2018 rates flat year over year. Granted, this is after a massive rate increase for 2017, but it was still welcome news, and once again underscored how much damage the Trump sabotage factor is.

Three days after allowing Children's Health Insurance Program funding to run out for 9 million kids across America, House Republicans are supposedly working on a bill to lock in 5 full years of funding for the program, along with a substantial initial funding infusion to help out Puerto Rico after the devastation of Hurricane Maria:

Republicans on a leading House health-care committee are proposing to send $1 billion in extra Medicaid funding to Puerto Rico as it deals with severe hurricane damage, as part of a five-year plan to fund the federal health insurance program for children.

In a year when every state's 2018 Open Enrollment situation is messy to say the least, Minnesota's is far more so:

Last year they were facing massive rate hikes, especially for unsubsidized enrollees (yeah, I know, I know, don't say it), and came very close to having all of their carriers bail

In response, they agreed to let most of them put a maximum enrollment cap on a First Come First Serve, with Blue Plus (BCBSMN) agreeing to take the "overflow".

However, the unsubsidized individual market enrollees were royally screwed, so the state legislature and governor slapped together a special, one-time 25% premium rebate specifically for them. The money came directly out of other portions of the state general fund, I believe. MNsure, the state exchange, also added an extra 8-day special enrollment period for these folks to jump in and get in on the rebate.

This got them over the 2017 hump, but clearly it was a sloppy, stopgap measure only, so earlier this year Minnesota decided to take advantage of the ACA's 1332 Waiver provision, which allows states to make significant changes to how they implement the ACA as long as the changes can be proven to provide at least as many people with similarly comprehensive coverage without increasing the federal deficit in the process...a provision which (former) HHS Secretary Tom Price encouraged states to do.

MarylandHealthConnection.gov has already been loaded with plans and prices for 2018, one month before open enrollment begins. The upcoming open enrollment period will run November 1 - December 15. Health coverage will start on January 1, 2018.

How do I get an estimate for 2018 health insurance plans?

You can compare plans and prices through a desktop computer browser or by downloading our mobile app, Enroll MHC, on your iPhone or Android.

Click on “Get Started”- this will take you to the application portal. Next, click “Get an Estimate” on the application site. Finally, enter basic information like your county, age and income to see what coverage and financial help you may qualify for. If you choose to get an estimate, the site will take you through a scenario of what plans and pricing you could receive for 2018. You won’t actually be applying for coverage.

As for CSR payments not being made, however, the press release accompanying the rate tables was more vague; it stated that they would be "up to" 14 points higher, but didn't clarify whether that would apply to every individual plan or only the Silver policies, which is how most other states appear to be handling it. I assumed the "no-CSR" average would be roughly 32.9% if the load is only dumped on Silver plans, but 40.7% if spread across all metal levels.

Preview Health and Dental Plans on Your Health Idaho

Shorter Enrollment Period November 1 - December 15

BOISE, Idaho – Today, Idahoans can get a preview on YourHealthIdaho.org of the 299 health and dental insurance plans being offered on the exchange in 2018, and how much help may be available to them.

“Insurance rates will be higher next year, but tax credits will increase to keep pace. Idahoans are often surprised at how much they can save on their health insurance through the exchange. “By going online now, consumers can check to see if they are eligible for tax credits to lower the cost of premiums,” said Pat Kelly, Your Health Idaho executive director. Consumers can take the savings information to comparison shop for the right plan.

Over the years I've repeatedly pointed out the importance of NOT simply "autorenewing" your policy. Yes, it's convenient (you don't have to do anything!), but you could be hit with a nasty pricing shock even if nothing has changed at your end (that is, even if your household size, income, etc has stayed the same). Even if your current policy is still available, due to the way APTC subsidies are calculated, you could see your financial assistance drop substantially or increase substantially from year to year...and there may be a better deal available even if there wasn't last year. ACTIVELY SHOP AROUND.