UPDATE: The 2018 Michigan ACA Exchange Enrollment Challenge! (Scenario 1: Young Family)

Sat, 10/14/2017 - 9:22pm

IMPORTANT: I need to stress that I am not in any way supportive of having CSR reimbursement payments cut off. I've written dozens of blog posts for the past year and a half about the danger this poses and I've repeatedly explained why this is a reckless, dangerous move by Donald Trump, I've even repeatedly noted how incredibly easy it would be to resolve the issue with a simple, one paragraph bill. Having said that, assuming the payments do stop being made, this is an explainer of how to turn it into a "lemonade out of lemons" situation for as many people as possible. Make no mistake, however: Millions of people will still be hurt by this...just not the people Trump thinks he's hurting.

Healthcare wonks like David Anderson, Louise Norris, Andrew Sprung, Josh Schultz, Wesley Sanders and I have been yammering on for weeks or months now about both the massive downside and the potential upside of Donald Trump pulling the plug on Cost Sharing Reduction (CSR) reimbursement payments. Now that it's a done deal*, it's time to take a good hard look at how this would work in real life starting November 1st.

*(Although maybe not...a whole mess of state Attorneys General have already filed lawsuts, so there could still be an emergency court injunction; it's also conceivable--though highly unlikely--that the Republicans in Congress will actually take 5 minutes out of their day to simply pass the damned 1-paragraph bill necessary to appropriate the payments already and put this nonsense to rest.)

Therefore, I've decided to demonstrate how CSR loading (along with the non-CSR factors causing unsubsidized premiums to increase for 2018) would impact different households here in Michigan. Why Michigan? For one thing, it's my home state. For another, Michigan is one of at least 28 states using the "Silver Load" approach to the CSR reimbursement cut-off dilemma, the most common path chosen by most states.

I plan on writing up scenarios for 6 different household scenarios for both 2017 and 2018 to see how their premiums would change year over year, and why.

- 1. Family of 3: 2 adults aged 30 each, 1 child age 5

- 2. Family of 4: 2 adults aged 40 each, 2 children ages 10 and 12

- 3. Family of 5: 2 adults aged 50 each, 3 children ages 17, 20 and 23

- 4. Family of 2: 2 adults aged 60 each, no children under 26

- 5. Family of 2: 1 adult age 28, 1 child

- 6. Single adult age 28, no children

In all cases, I'm assuming that no one smokes, and that all of the families above live in Oakland County, Michigan.

In addition, for each scenario, I'll plug in 7 different household income levels: $30,000, $40,000, $50,000, $60,000, $70,000, $80,000 and $90,000.

Finally, for each scenario, I'll see what they'd end up paying for the lowest-price Bronze plan, the benchmark Silver plan and a mid-range Gold plan.

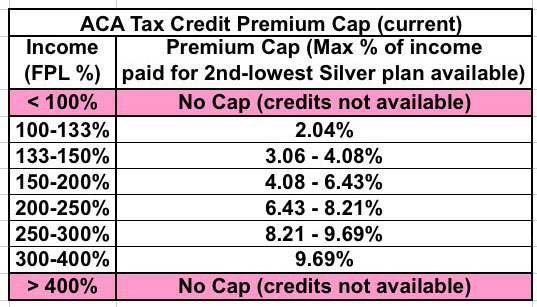

First of all, here's the 2017 Advance Premium Tax Credit (APTC) formula table:

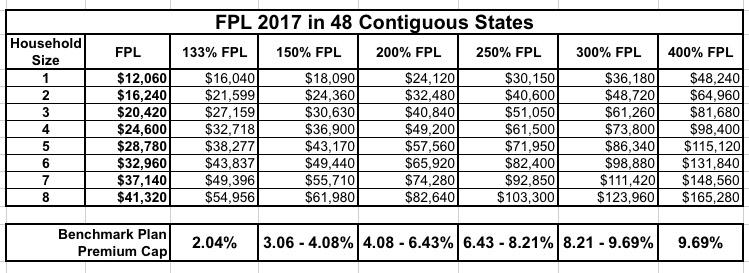

...and here's the table showing where the income brackets are for the different Federal Poverty Level ranges:

OK, got all that? Let's get started.

SCENARIO ONE: Family of 3: Two adults aged 30 each with one 5-year old child.

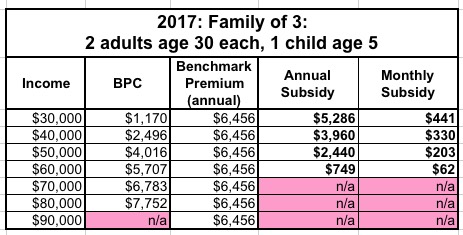

First, we need to find out what this family's Benchmark Premium Cap (BPC) is at the different income levels:

- At $30,000/year, they're at 147% FPL, so their BPC is around 3.9% of their total income, or around $1,170/year.

- At $40,000/year, they're at 196% FPL, so their BPC is around 6.2% of their total income, or around $2,496/year.

- At $50,000/year, they're at 245% FPL, so their BPC is around 8.0% of their total income, or around $4,016/year.

- At $60,000/year, they're at 294% FPL, so their BPC is around 9.5% of their total income, or around $5,707/year.

- At $70,000/year, they're at 343% FPL, so their BPC is 9.69% of their total income, or around $6,783/year.

- At $80,000/year, they're at 392% FPL, so their BPC is 9.69% of their total income, or around $7,752/year.

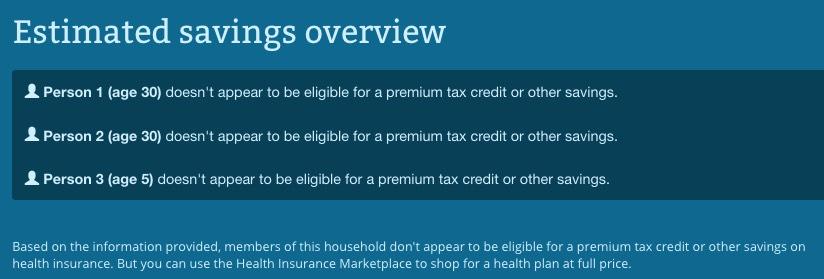

- At $90,000/year, they're at 441% FPL, so they receive no tax credits and have to pay full price no matter what.

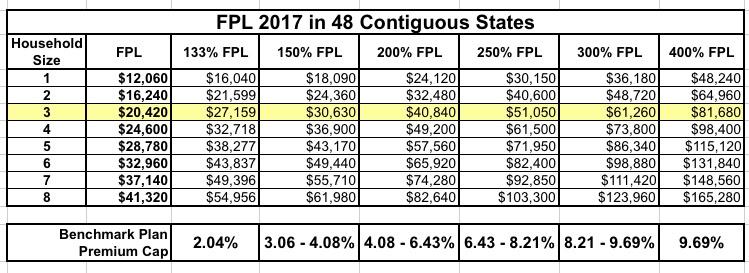

Next, let's see what the Benchmark Plan (2nd lowest-cost Silver plan) is in Oakland County, Michigan.

I can find this by plugging the family's info into HealthCare.Gov's window shopping tool, but deliberately listing the income as over 400% FPL to see what the cost is at full price. Then I limit my selection to SILVER plans only, sort them by premium and see what the 2nd one down is:

$538/month x 12 is $6,456/year. Whatever the difference is between $6,456 and the BPC amount should be the amount they receive in tax credits, which can be applied to any exchange plan (not just Silver):

As you can see, in 2017, this family will receive $441/month in tax credits at $30K/year, $330/month at $40K, $203/mo at $50K, $62/month at $60K and nothing at $70K and up because at that point, the cost of the benchmark plan costs less than their BPC. This is why "being below 400% FPL" doesn't guarantee that you receive a tax credit; it's just the maximum income you can have and still possibly receive one. For the $30K - $60K scenarios, remember that the tax credits can be applied to any plan on the exchange, not just the benchmark Silver.

OK, now let's plug this info into HealthCare.Gov and see what we get.

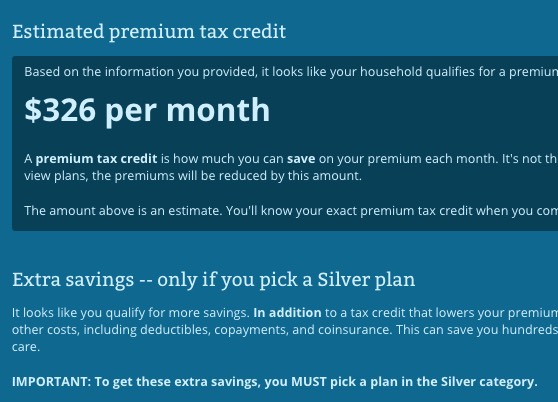

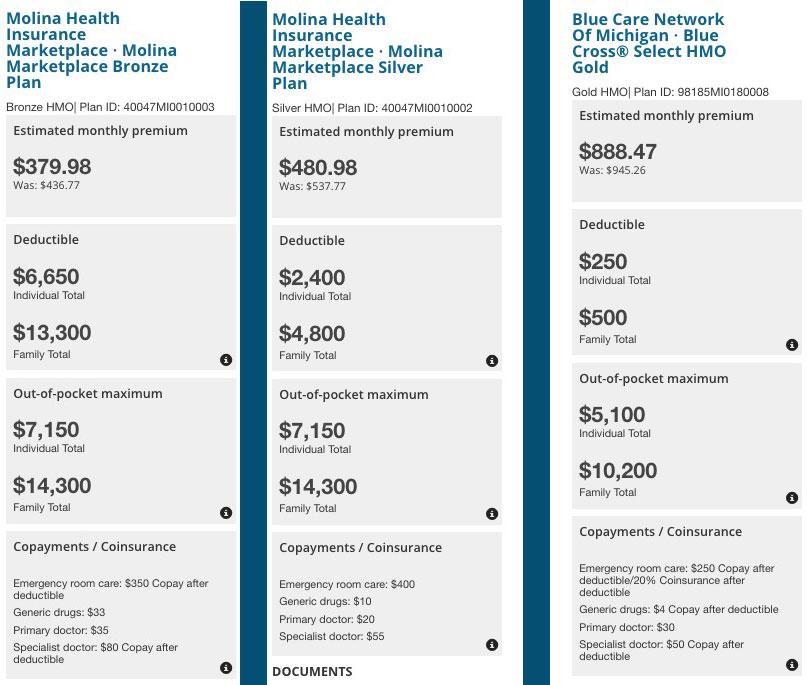

$30,000/year (147% FPL):

UPDATE: Thanks to Dave Anderson and Louise Norris for solving a weird little mystery for me: I couldn't figure out why the unsubsidized Benchmark Plan showed up as costing $420/mo instead of $538/mo at the $30K and $40K income levels, but they pointed out that in Michigan, the CHIP program covers children up to 212% FPL, which means that in these scenarios, the child is automatically subtracted from the policy, since the assumption is that they'll be enrolled in CHIP instead. Therefore, the $420/month premium only covers the two adults, not the child as well:

Of course, considering that CHIP program funding was just allowed to expire two weeks ago and there's no way of knowing if/when it'll be renewed, that raises a whole other problem...but let's focus on the current situation for the moment:

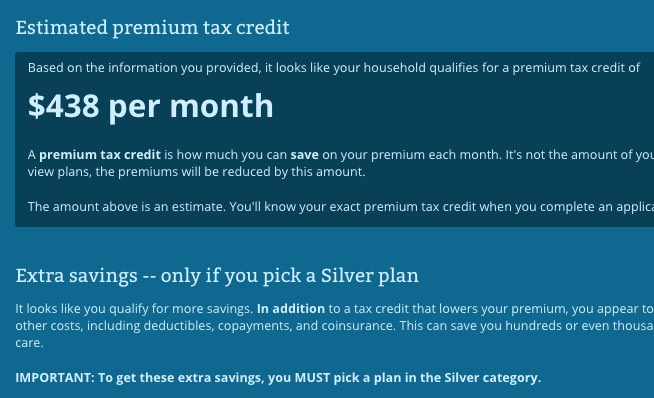

OK, I was slightly off...they actually get $438/month. In addition, they're below 250% FPL, so they also qualify for CSR assistance as long as they choose a Silver plan.

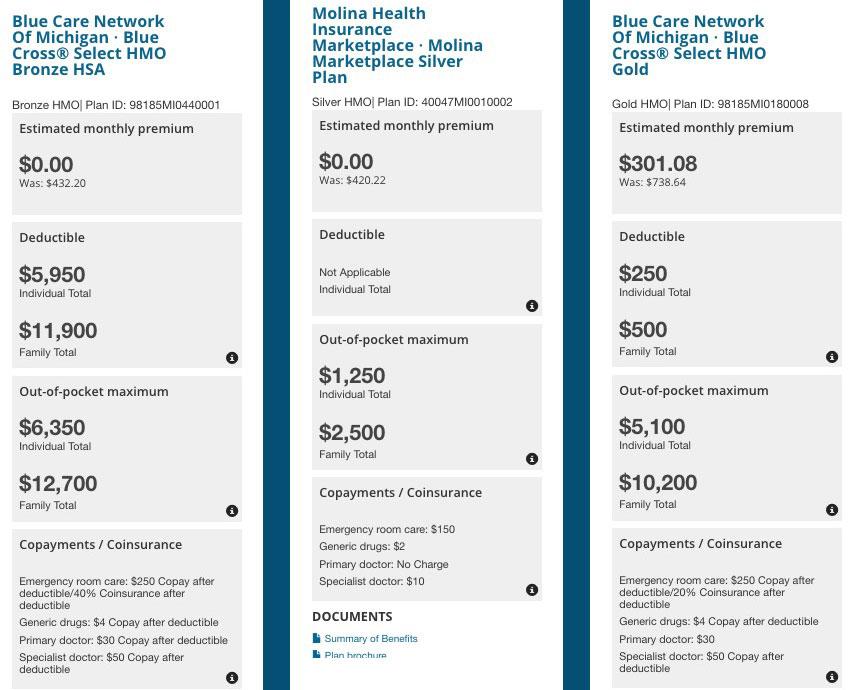

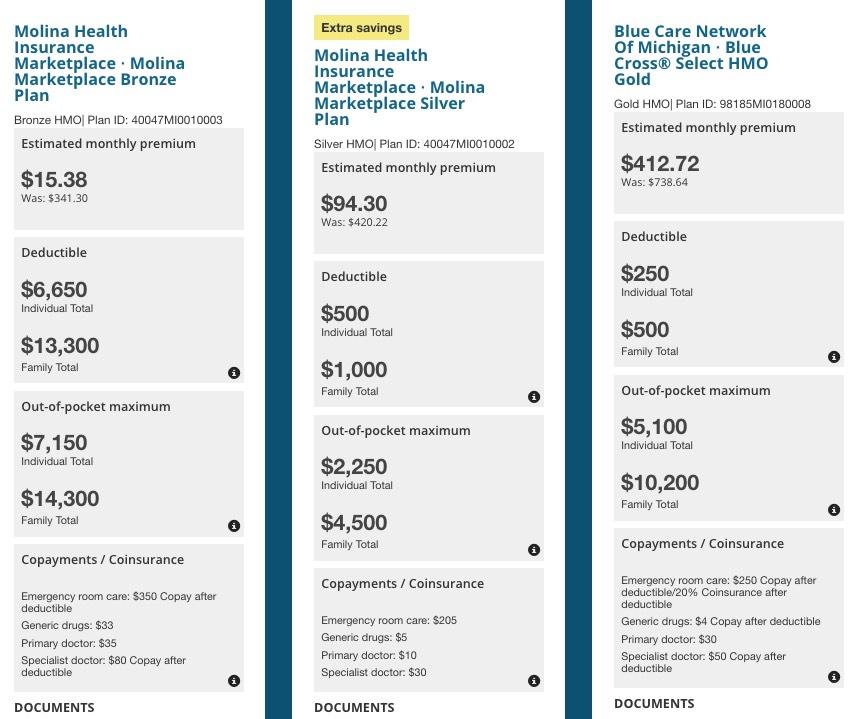

Here's their Bronze, Silver and Gold options. Remember, I'm going with the cheapest Bronze, 2nd cheapest (Benchmark) Silver and mid-range Gold in all cases:

As you can see, this family is much better off choosing the Benchmark Silver Plan for 2017. They won't have to pay a dime for the premiums, and thanks to the CSR assistance, their deductible has been completely wiped out. Furthermore, again thanks to CSR help, their total out of pocket cost is only $2,500 for the year no matter what. Their absolute worst-case scenario would mean total healthcare costs of no more than $2,500 for the year, or 8.3% of their total income.

$40,000/year (196% FPL):

Again, I was slightly off, but very close; and again, they're below 250% FPL, so they still qualify for CSR assistance on Silver plans:

At $40,000, the tax credits have dropped enough that the family will have to start paying at least some of the premiums. They can get the Bronze plan for a nominal $15/month, but would be hit with a $13,300 deductible, ouch. They're still much better off paying $94/month for the Silver plan. That'll cost them $947 extra for the year, but the deductible is only $1,000, and their out of pocket maximum is only $4,500 (vs. $14,300 for Bronze). The absolute most they'll have to pay for everything combined in 2017 is $5,632, or 14% of their total income.

$50,000/year (245% FPL):

Slightly off again. They're just barely below the CSR cut-off, however.

At $50,000/year, the choice starts to become a bit less obvious, although the Silver plan is still pretty clearly the way to go: It costs $100 more per month in premiums, but the deductible is still far lower than the Bronze thanks to the limited CSR assistance, and the maximum out of pocket cost is still thousands lower as well. A Gold plan still probably makes no sense, since the premiums alone would cost 18% of the household income.

$60,000/year (294% FPL):

At this point we're well over the CSR threshold, and the tax credits have dropped off rapidly (also, again, I'm off by a few dollars in my estimates).

With CSRs out of the loop, it becomes a tougher call between Bronze, Silver and Gold. Bronze will only cost 7.6% of their income...but they'll have a $13,300 deductible. Silver will cost 9.6% of their income, but the deductible drops to $4,800. Gold will cost 17.8% of their income (ouch!) but only has a $500 deductible. If they know they'll have a lot of expensive ailments/treatments, they should go for the gold, but otherwise Bronze or Silver would be better.

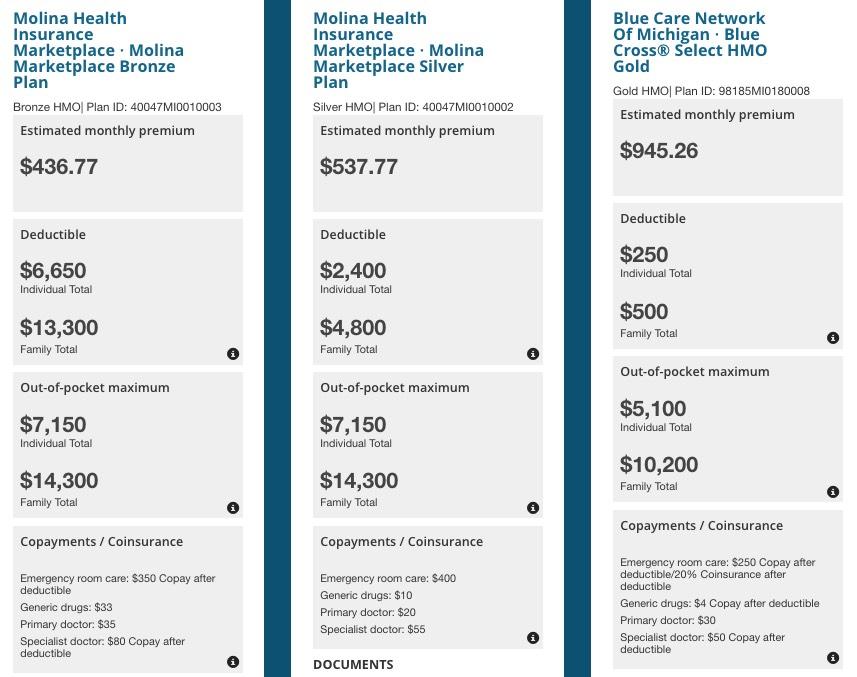

$70,000/year or higher:

I've already noted that even though $70K is still less than 400% FPL for this family, they still won't qualify for any tax credits at all since the benchmark plan now costs less than their BPC, so they'll have to pay full price no matter what:

Again, at this point it really depends far more on the famly's specific medical situation than anything else. Either Bronze, Silver or Gold might be their best bet. At $70,000, it'll cost anywhere from 7.5 - 16.2% of their total income in premiums, pls $500 - $13,300 in deductibles depending on how things play out.

OK, but what about 2018?

Unfortunately, I have no idea what the benchmark plan will cost yet in 2018, but I can take a pretty good guess:

- BCBSMI would be raising rates around 27% if CSRs were paid, but is also adding about 10% onto their Silver plans specifically, so they'll cost roughly 37% more on average at full price.

- Blue Care Network would be raising rates 13.8%, but is adding another 14.8% to Silver plans (around 28.6% more at full price).

- Meridian would be raising rates around 30%, but is adding another 37.9% to Silver plans (67.9% more at full price).

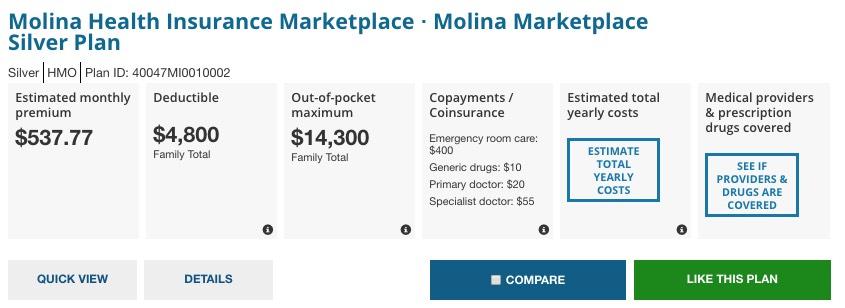

- Molina--this year's Benchmark plan holder--would be raising rates about 20% but is adding another 33.4% to Silver (53.4% more at full price).

- Physicians Health Plan would be raising rates 16.3%, but is adding another 20% to Silver (36.3% more at full price).

- McLaren would be raising rates 16.9% but is adding another 19% to Silver (35.9% more at full price).

I'm missing a couple of carriers, and the actual rate increase varies widely from plan to plan, but it's safe to assume that whatever the Benchmark Plan in Oakland County, Michigan will be for 2018, it will likely be something like 40% more at full price than it is this year. For this particular family, that would mean the benchmark plan would go from $538/month to around $753/month.

Since this post is getting so long/complicated as it stands, I'm going to assume that the family in question chose the benchmark Silver plan in all cases above for 2017, and is considering whether to renew it for 2018. I'm also assuming that all the 2017 policies are still available in 2018.

Remember, we're assuming that the family's household income stays the same year over year, they don't have any more children and so forth. The only change is that they're each a year older (which does nudge the rate for both adults up a couple percent all by itself, I should note).

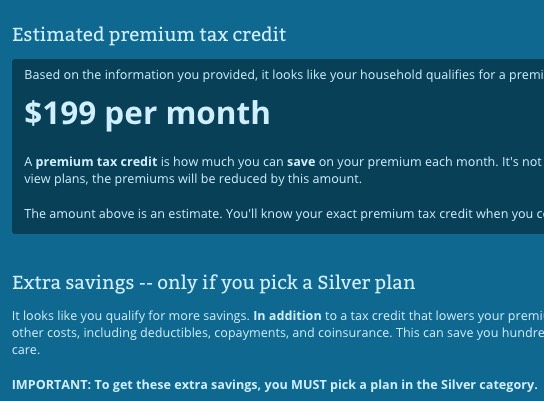

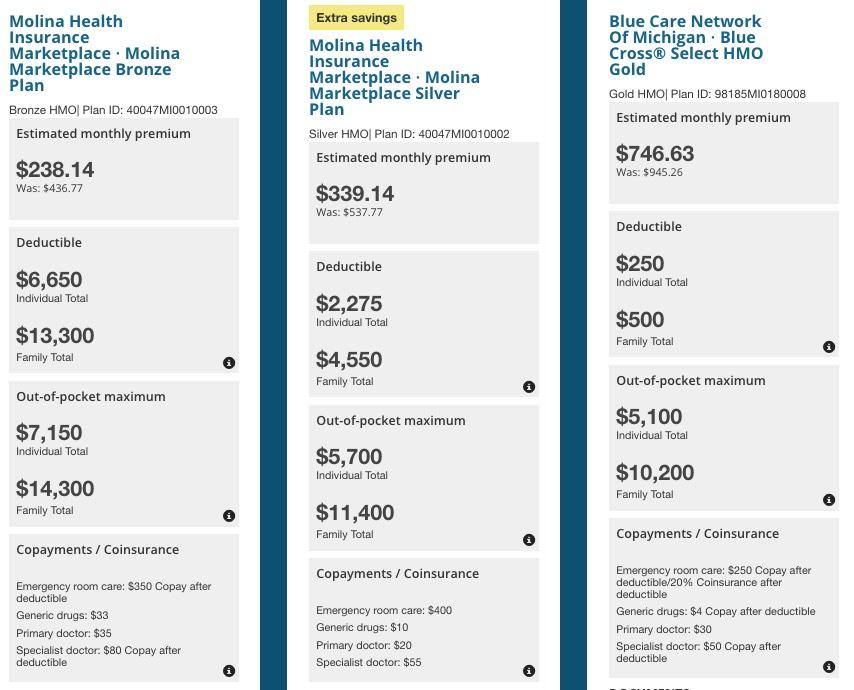

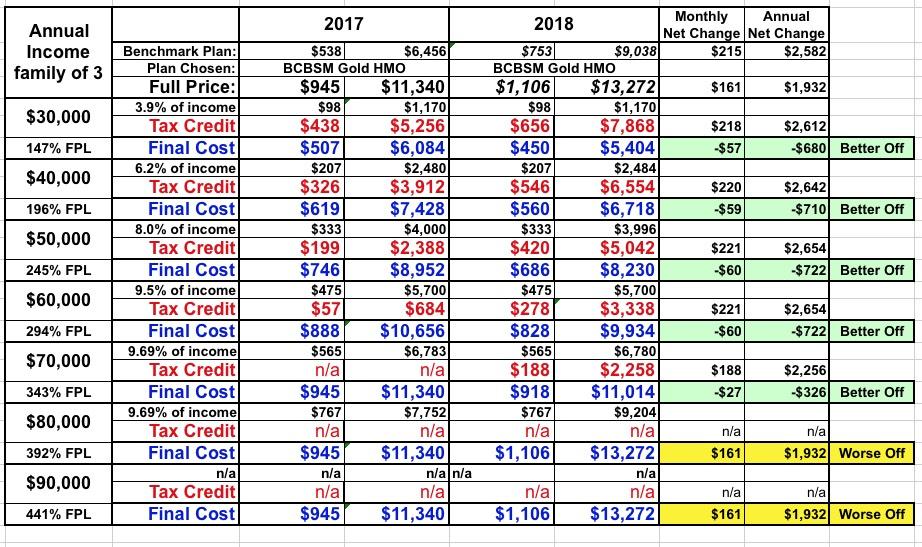

Assuming the Benchmark Plan increases by about 40%, here's what the 2018 costs would look like if they stick with the same plan before and after tax credits are applied:

As you can see, the unsubsidized premiums have shot up by $215/month...but the tax credits have also gone up to match (or even potentially a bit higher), meaning that all the way up to $60,000, they'll actually pay virtually the same amount after tax credits are applied. At $70,000, they will start to see a small increase of $27/month, but that's still much better than $215/month. Unfortunately, at $80,000 and $90,000, they still won't receive any tax credits to cushion the blow at all.

This is the situation for over half the states: Anyone earning less than 400% of the federal poverty level should either be better off (or at worst, should hold about steady in most cases)...and more people should become eligible for at least modest tax credits...but anyone earning more than 400% FPL will be hit with a nasty rate spike...and it'll be especially nasty for current Silver plan enrollees.

Another 12 states are going the full Silver Switcharoo route. For these folks, Silver enrollees who are subsidized may see an even more impressive increase in their tax credits (since the CSR load will be even more concentrated)...but unsubsidized Silver enrollees, both on and off the exchange, will have the option of simply switching to a nearly identical off-exchange Silver plan instead which won't have any CSR load. Again, there may be other rate increases to contend with...but the CSR load won't be among them.

That leaves a handful of states which are either spreading the CSR load across all metal levels on and off the exchange or which assumed CSRs would continue to be paid and are now scrambling to refile their 2018 rates. It would be great if they all went Full Silver Switcharoo, but my guess is that most of these will do what Michigan and over half the other states are doing in the end.

However, what happens if the family above decided to choose the GOLD plan in 2017? How much will they pay in 2018?

Remember, the unsubsidized Benchmark Silver plan shot up by 40%...but BRONZE, GOLD and PLATINUM plans will only be going up around 17% on average. For the Gold BCBSM policy, that means the unsubsidized price will likely increase from around $945/month to $1,106/month.

That gives something like the following for 2017 and 2018:

As you can see, since the benchmark Silver plan (which tax credits are based on) shot up 40% but the Gold plan only increased by 17%, the tax credits result in a nice little bonus for the first four scenarios. Instead of Gold premiums going up by 17%, they actually drop by about $60/month, saving subsidized Gold enrollees about $700 for the year. At $70,000 income, that savings is cut in half to about $27 per month, but it's still a tidy unexpected savings.

Unfortunately, again, unsubsidized enrollees in this scenario are indeed hit with the full $161/month rate hike on the Gold plan (17%).

The other really important thing to take note of is that this family qualifies for tax credits in 2018 with a $70,000 income even though they didn't in 2017. This is why it's vitally important that everyone actively shop around on the ACA exchange instead of passively auto-renewing or just assuming that they won't be eligible and buying the same policy off-exchange instead.

In this scenario, if this family earns $70,000 this year and expects to earn the same amount in 2018, they might assume that because they didn't qualify for any assistance for 2017, they won't next year either...and instead of saving $326, they'd end up spending $1,932 more...losing out on $2,256 in savings.

BOTTOM LINE: SHOP AROUND, SHOP AROUND, SHOP AROUND!

Advertisement