Of the 31 states which have expanded Medicaid under the Affordable Care Act, only a handful issue regular monthly or weekly enrollment reports.

Back on February 28th I noted that ACA Medicaid expansion enrollment across three states (Michigan, Louisiana and Pennsylvania) had grown by about 35,000 people since mid-January, to 667K, 406K and 716K people respectively.

Today, a month later, I decided to take another look at all three states, along with Minnesota (which I forgot to check last month). Sure enough, enrollment has continued to grow in all four, albeit at a slower pace:

As noted a few weeks ago, Humana has already decided that regardless of what actions Donald Trump, Tom Price or Congressional Republicans end up doing (or not doing), they expect the 2018 individual market to be a big mess they want no part of...either on or off the exchanges:

...based on its initial analysis of data associated with the company’s healthcare exchange membership following the 2017 open enrollment period, Humana is seeing further signs of an unbalanced risk pool. Therefore, the company has decided that it cannot continue to offer this coverage for 2018. Through the remainder of 2017, Humana remains committed to serving its current members across 11 states where it offers Individual Commercial products. And, as it has done in the past, Humana will work closely with its state partners as it navigates this process.

Again, it's important to stress that Humana isn't just bailing on exchange participation, but to the best of my knowledge, they're pulling up stakes off-excahnge as well.

So The Plague is wreaking havoc on the world's population. Maybe Super Flu has killed millions, or some unknown biological agent is causing people to snap and kill each other. Heck, maybe we even have a good old fashioned Zombie Apocalypse on our hands. Either way, it's safe to say that for most of humanity, these are not fun times. How could things get much worse, you ask?

By the revelation that the disease in question has been manufactured by genetic engineering, and possibly is distributed by humans. The untold amount of death and destruction has been directly caused by the foolish or malicious action of Man himself.

It may have been designed for use as a biological weapon, or an unexpected result of an experiment gone wrong. Perhaps we just shouldn't have let monkeys watch TV for too long. However it came to be, it has now been unleashed on humanity at large, and has almost certainly gone far beyond what its designers had originally intended.

There's been a lot of talk, by myself and others, about just which populations would be screwed over by a full repeal of the Affordable Care Act. Analysts, reporters and pundits have sliced and diced the numbers every which way...by race, income level, geography and of course political leanings.

Of course, this gets awfully messy right out of the gate because some ACA provisions apply to everyone in the country, such as the cap removal on annual/lifetime coverage limits; the reassurance that you can't be denied coverage for having pre-existing conditions (which applies to those covered by employer insurance as well, I should note, since many of them may have to switch jobs or be without one at some point in their lives), and so on. Other benefits apply to subgroups which aren't talked about much, such as the Medicare fund being extended by years and the Medicare Part D "donut hole" being closed.

The Trump administration has pulled the plug on all Obamacare outreach and advertising in the crucial final days of the 2017 enrollment season, according to sources at Health and Human Services and on Capitol Hill.

Even ads that had already been placed and paid for have been pulled, the sources told POLITICO.

...Individuals may still sign up for Obamacare plans until the Jan. 31 deadline — but the Trump administration isn't advertising that fact any longer.

It is also halting all media outreach designed to spur signups in the days leading up to the deadline. Emails are no longer being sent out to individuals who visited HealthCare.gov, the enrollment website, to encourage them to finish signing up. Those emails had proven highly successful in getting stragglers to complete enrollment before the deadline.

Ron Pollack, executive director of Families USA, a consumer group that supports the law, called the decision "a mean-spirited effort that can only result in fewer people getting coverage who need it."

President Trump called my cellphone to say that the health-care bill was dead

President Trump called me on my cellphone on Friday afternoon at 3:31 p.m. At first I thought it was a reader with a complaint since it was a blocked number.

Instead, it was the president calling from the Oval Office. His voice was even, his tone muted. He did not bury the lede.

“Hello, Bob,” Trump began. “So, we just pulled it.”

...The Democrats, he said, were to blame.

...Trump said he would not put the bill on the floor in the coming weeks. Instead, he is willing to wait and watch the current law continue and, in his view, encounter problems. And he believes Democrats will eventually want to work with him on some kind of legislative fix to Obamacare, although he did not say when that would be.

It tacks on an additional one-time $15 billion to the "State Stability Fund", supposedly to cover maternity, newborn care and mental health services.

It pays for the above by holding onto the existing 0.9% Medicare tax on people earning over $200,000 for another 6 years

And, most significantly, it would get rid of the requirement that all qualifying healthcare policies cover the 10 Essential Health Benefits mandated by the federal government.

The original version of the AHCA would have resulted in older Americans having to pay exhorbitant premiums due to the idiotic restructuring of the tax credit system and the 5:1 age band change. This led the AARP to unleash their army to understandable scream bloody murder at Congressional town halls nationwide.

In response, the GOP added an oddly-worded amendment which "instructed" the Senate to pony up $85 billion which would be used to "increase tax credits for 50-64 year olds" in some vague fashion. Why they didn't simply cross out "$4,000" and replace it with "$10,000" in the language of their own text I have no idea, but whatever. The point is that they gummed up the works for older enrollees, got screamed at for it, and responded by throwing a boatload of cash at those folks to get them to STFU.

UPDATE: 7:42 p.m.: President Donald Trump is demanding a vote Friday in the House on the Republican plan to repeal and replace Obamacare, White House Budget Director Mick Mulvaney said. If the bill fails, Trump is prepared to move on and leave Obamacare in place, Mulvaney said.

In the case of Donald Trump, however, he could mean it. He doesn't actually give a rat's ass about healthcare or helping people anyway; the only reason he wants to repeal the ACA is because a) it'd let him stick it to Barack Obama; b) it'd give him another tax cut and c) he'd get to brag about "winning" by finally slaying the mighty Obamacare Beast, etc.

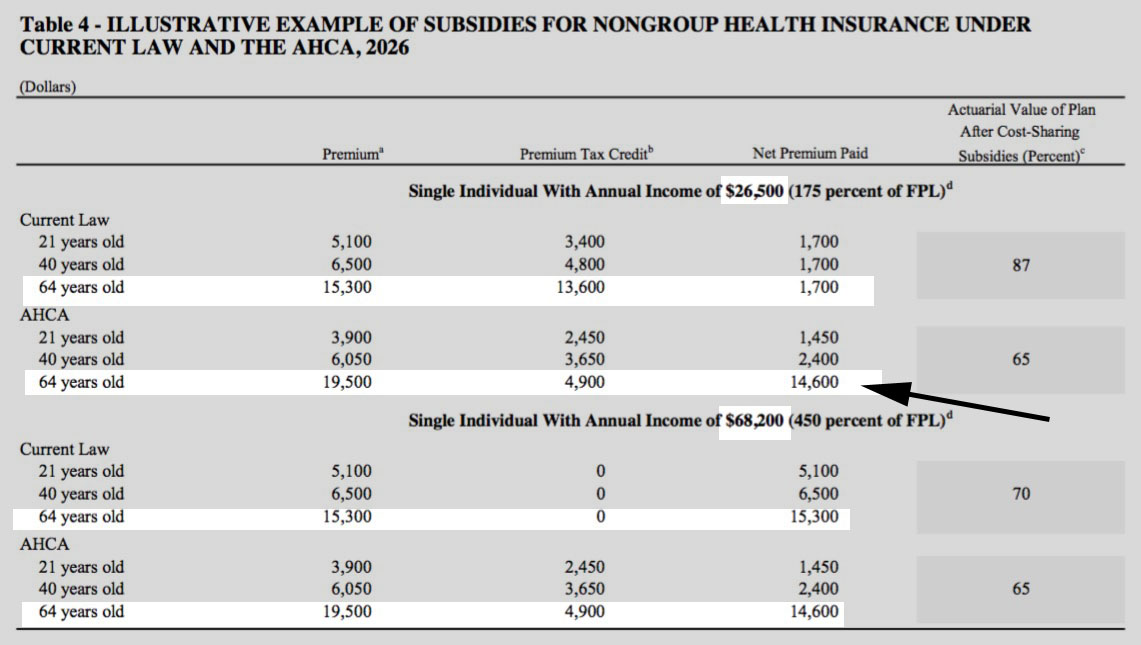

A couple of weeks ago, the Congressional Budget Office projected that Trumpcare 1.0, aka the "American Health Care Act" or AHCA would kick 14 million people off their healthcare coverage next year alone, followed by an additional 10 million getting the boot by 2026. It would, however, save the federal government around $336 billion over that time period, which was pretty much the only positive part of their analysis.

This didn't go over too well with the "moderate" wing of the House GOP, as the AARP crowd wouldn't stop screaming at them during town halls nationwide. Meanwhile, the "Freedom Caucus" (basically, the ultra-batcrap insane wing as opposed to the only-kinda-insane members) was angry because the Trumpcare bill didn't hurt enough people quickly enough.

House leaders postponed a vote Thursday on their plan to overhaul the nation’s health care system, as they struggled to meet demands of conservative lawmakers who said they could not support the bill.

Earlier Thursday, conservative House Republicans had rebuffed an offer by President Trump on Thursday to strip a key set of mandates from the nation’s current health-care law, raising doubts about whether House Speaker Paul D. Ryan (R-Wis.) had the votes.

Trump met at the White House with the most conservative House Republicans, hoping to close a deal that would help ensure passage of the party’s health-care plan by shifting it even further to the right. But the session ended with no clear resolution, and some lawmakers said they needed more concessions before they would back the bill.

March 23, 2017 - U.S. Voters Oppose GOP Health Plan 3-1, Quinnipiac University National Poll Finds; Big Opposition To Cuts To Medicaid, Planned Parenthood

American voters disapprove 56 - 17 percent, with 26 percent undecided, of the Republican health care plan to replace Obamacare, the Affordable Care Act, according to a Quinnipiac University national poll released today. Support among Republicans is a lackluster 41 - 24 percent.

If their U.S. Senator or member of Congress votes to replace Obamacare with the Republican health care plan, 46 percent of voters say they will be less likely to vote for that person, while 19 percent say they will be more likely and 29 percent say this vote won't matter, the independent Quinnipiac (KWIN-uh-pe-ack) University Poll finds.

(Granted, most of the 46% who say they're less likely to vote for them are most likely Democrats anyway, but still).

Republican Pete Sessions just literally said "Nobody is going to lose their coverage, you'll be able to keep your same doctor," "same plan." pic.twitter.com/nn0f4dFloc

Seven years ago, President Obama repeatedly made an infamous promise: That under the Affordable Care Act, "If You Like Your Plan, You Can Keep It...If You Like Your Doctor, You Can Keep Them."

As a big fan of Obama and a supporter of the ACA, this statement has been making me, and any intellectually honest Democrat, wince ever since.

The changes in question appeared to include a) hurting even more poor/disabled people more quickly than before by speeding up the Medicaid expansion cut-off and block-granting non-ACA Medicaid...but also a vague reference to beefing up the individual market tax credits for older enrollees.

Now the Medicaid cruelty aside, I've long been an advocate of beefing up the indy market subsidies myself, so this isn't necessarily a terrible idea, although the devil would be in the details. I assumed, for instance, that Ryan & Co. planned on changing the age-based structure from this:

UPDATE: After thinking about it all day, I've decided to remove the "scrotum" nickname from the headline. I reserve the right to keep it in the body of this and future posts, however.

After being lambasted by pundits, reporters and politicians across the political spectrum for pushing an ACA replacement bill which would effectively raise insurance premiums on older enrollees up to eight times higher than they would be otherwise (eating up over 50% of their annual income in some cases)...

I've spent the past two months painstakingly crunching the numbers in an attempt to project just how many people would likely lose their healthcare coverage if the ACA were to be: a) fully repealed; b) with immediate effect; and c) without any substantive replacement policy put into its place.

My conclusion, after much analysis, double-checking and updating, is that the grand total would be roughly 24 million people: Around 8.2 million current exchange enrollees, nearly 15 million via Medicaid (expansion or otherwise), and the 750,000+ people enrolled in BHP programs in Minnesota and New York.

When I was 18 years old, my father died of a brain tumor.

A few weeks after the funeral, I left for college at Michigan State University. Freshmen were required to room blind, so I had no idea who my roommate would be. When I met him, a tall blonde guy named Brian, I was still wearing the Kriah ribbon--a small torn piece of black cloth.

We shook hands, introduced ourselves, and then Brian asked me what the torn ribbon was for. I explained that my father had recently passed away, and that Jewish custom was for mourners to wear torn black cloth as part of the mourning process.

His response?

"Oh, I'm sorry to hear that he's burning in hell right now."

I should note that this was less than 5 minutes after we had met. I was assigned to live in the same room as this guy for the next 9 months.

For 2017, the weighted, average, unsubsidized (that's critical!) premium rate increase for ACA-compliant individual market healthcare policies was roughly 25% nationally.

There were plenty of reasons for this, including normal inflation/healthcare costs; the discontinuation of two of the three stabilization programs (Reinsurance and Risk Corridors, although the RC program had already been sabotaged a year earlier anyway); correction for under pricing by many carriers in the first couple of years of the ACA exchanges; and, of course, the fact that the ACA exchange risk pool continues to be worse than hoped for in numerous states/counties.

Of course, for the roughly 10 million exchange enrollees who are receiving tax credits, this didn't really impact them much at all:

On average, ACA marketplace consumers receiving tax credits are literally paying exactly the same this year as last year -- $106 per month. pic.twitter.com/WzqA6DsWRN

You may have noticed that I haven't been posting as many blog entries the past week or two. This has been partly due to our 5-day power outage, of course, as well as various other personal odds & ends. The main reason, however, is that I've been driving around the metro Detroit area giving a PowerPoint presentation about the ACA and Trumpcare to various groups. Last night was my 4th or 5th presentation, and while it was kind of sloppy and scattershot the first few times, I'm streamlining and modifying for each new event.

Even so, I'm cramming a lot of information into an hour or so, and several people at each event have asked if I could upload the slideshow to the website for easy download.

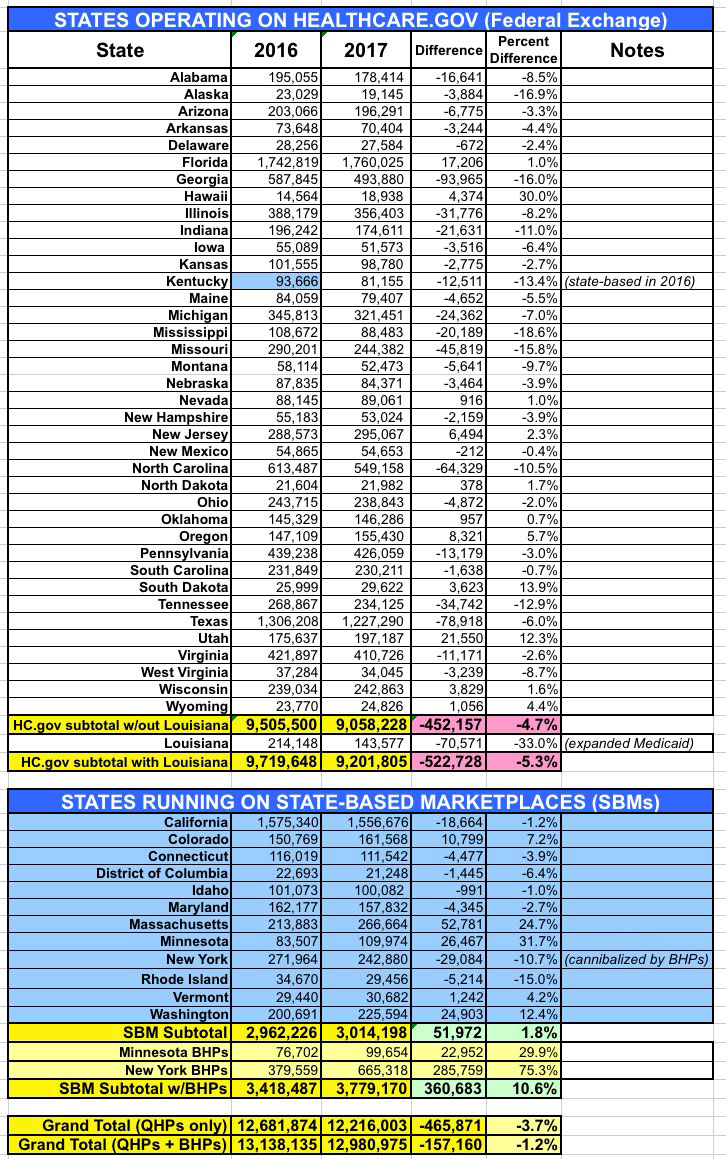

Of course, it's impossible to prove that the Trump executive-order/ad-kill combo was the cause of the numbers petering out at the end of the enrollment period...but I have some pretty strong evidence that it did.

How? Well, remember, the 12 state-based exchanges, which cover around 1/4 of all Qualified Health Plan (QHP) selections nationally, were not hurt by the ads being killed. The executive order might have had some impact, but the actual HC.gov ads being yanked shouldn't have hurt them much since these exchanges have their own, separate branding, marketing budgets and outreach programs.

I therefore decided to compare how the 39 HC.gov states performed relative to the 12 state exchanges...the results are pretty telling.

...UPDATE 3/16/17: I've updated the tables and chart below with the final, official 2017 Open Enrollment Period numbers from CMS.

As I noted earlier today, CMS has released the official 2017 Open Enrollment Period report, along with a whole mess of State, County and Zip Code-level breakouts and related demographic information, including APTC/CSR recipients, Metal Levels, Income Levels and so on.

On the one hand, this will take some time, so please bear with me. It took nearly 2 months to compile this data for all 50 states; it might take another week or so to update them with the latest numbers. Also note that it may only be the 39 states on the federal exchange which get updated, unless some of the state-based exchanges release their own updated reports.

On the other hand, it's important to note that for most counties/congressional districts, the numbers are likely to be fairly close to where they already are. For example, I've already completed Michigan; here's a before/after comparison:

In addition, unless I'm mistaken, most of the actual staff...the career employees at CMS/HHS, many of who've been there through more than one administration, will likely remain, and will do their jobs to the best of their ability, including trying to compile and publish data as accurately as possible.

Yesterday the CBO pretty much torpedoed the Trumpcare bill. Everyone from across the political spectrum now seems to agree that it's a complete disaster, with the exception of Paul Ryan and Tom Price (hell, even an internal Trump White House analysis apparently concluded that even more people would lose coverage than the CBO did...26 million vs. the CBO's 24 million).

However, there's one part of the AHCA which should be kept: The $100 billion that they currently have allocated to throw at the states to stabilize the individual market. As the CBO noted:

After five days, my power still hasn't been restored, and it's no fun typing with freezing fingers on a cold keyboard, but I had to make an exception for this: The CBO has officially scored the Trumpcare bill.

As noted this morning, our power is out and isn't expected to be back up for several days, so my posts will be spotty and brief while we deal with stuff like our kid being out of school, keeping the generator running, etc. However, I just had to post this one.

You've probably already seen this clip, but it's so staggeringly idiotic that I have to repost it here.

Do I even need to explain how gob-smackingly stupid this claim by Paul Ryan is?

...things have been a little hectic around these parts...

I'll try to post an update later this afternoon but, power might not be restored until as late as Sunday, so I have to deal with a whole mess of stuff (including my official day job, of course).

UPDATE 3/13/17: Nope, still out.

UPDATE 3/14/17:

WOO-HOO!!!

Yup, as of 8:12pm Monday evening, we finally got our power back. Yeesh.

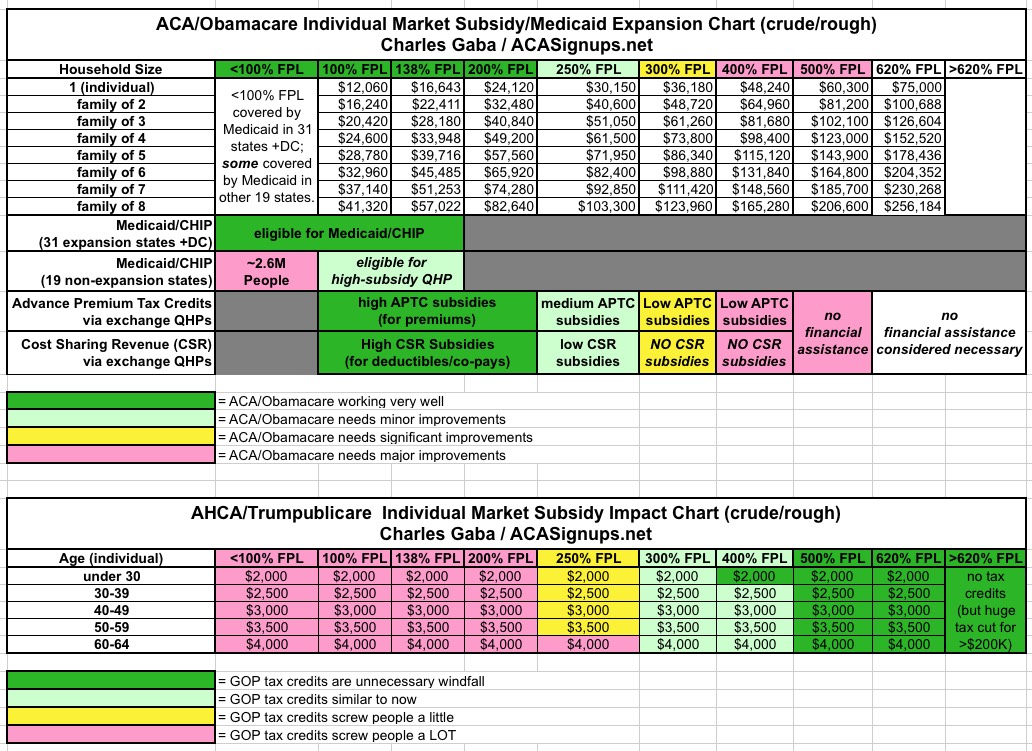

Back in January, being a spreadsheet guy but not being a particularly good graphic artist, I put together a crude table which attempted to give a general idea of which groups of people the Affordable Care Act is, in general, working out for fairly well vs. which groups the ACA isn't working for, by income threshold. A couple of days ago, with details about the GOP's "replacement plan" popping up all over, I posted a similar version of the table which tried to compare the winners/losers between the two plans, and the contrast was remarkable: Nearly a complete reversal.

Last night, with the GOP's plan finally, officially revealed, I made some minor adjustments so that the two tables were more of an apples-to-apples and came up with the following:

So, it's finally here. After seven years and over 100 entries, Huffington Post healthcare reporter Jeffrey Young can finally shut down (or at least archive) his famous "JUST IN TIME!" Storify collection, which has been chronicling the endless empty promises of the Republican Party insisting that their "replacement plan" for the Patient Protection and Affordable Care Act was going to be revealed at any moment.

Yes, after seven years, it's finally here (Part 1)and here (Part 2). It has a catchier title than the ACA ("The American Health Care Act"), which is typical of Republican bills. Remember George W. Bush's "Healthy Forests Initiative", which actually opened previously protected forest areas to logging, often unnecessarily or under false pretense?See, it has the word "American" right there in the title, so it must be good, right? I'll be abbreviating tthis as "AHCA", although they're already annoying me by spelling "healthcare" as two words (I strongly believe it should be one).

Here's the stuff which supposedly can't be changed via the reconciliation process, and is therefore might not be touched...yet. That is, these are changes which would suppposedly either require 60 votes in the Senate or would require the GOP to kill the filibuster entirely to push through:

Guaranteed issue (no pre-existing condition denials)

Community rating (can't charge different people more for the same policy outside of a tight set of parameters)

The ACA's preventative benefits (I'm not sure if this list changes, but I'd imagine not)

No lifetime or annual limits on coverage (a few people have stated otherwise, but this seems to be the consensus)

Required essential benefits for every plan on the private market (ie, group or individual)

Limits on out-of-pocket costs for enrollees

Young adults 19-25 being allowed to stay on their parents' plan (I've noted before that I always suspected this would survive any repeal effort)

"Removing the lines" to allow carriers to "sell insurance across state lines" (at least not any more so than the ACA already allows them to)

The "Grassley Amendment": Congressional staffers will still have to enroll via the DC exchange in order to receive tax credits.

The 80/20 Medical Loss Ratio (requires insurance carriers to refund the difference to enrollees if they spend more than 20% of premium costs on anything other than actual, legitimate medical care)

All of the above sounds great at first glance...but again, keep in mind that for the most part this is only because they can't touch them without 8 Democratic Senators agreeing to do so...or killing the filibuster, which they could still do. That's a hell of a Sword of Damocles to be hanging over everyone's head.

OK, so what would change via the AHCA, assuming they manage to pass it with simple majorities in the House and Senate, and Trump signs it (which I'm certain he would)?

Initially, the story seemed to be about a man who railed against Obamacare while both taking absolutely no responsibility for failing to take advantage of the benefits of the law which he was entitled to and simultaneously blaming President Obama for the failure of his own GOP-controlled state to expand Medicaid under the law. Several people wrote up articles ripping Mr. Lang to shreds over his seeming hypocrisy, myself included.

In addition to all of the other horrific details which are oozing out of the House Republican's "Basement Bill" to replace the ACA, something else has been nagging at me for a few days now, but I couldn't quite put my finger on it until today.

The issue was sort of coalescing in my brain all afternoon, but it was a couple of other folks who laid it out first:

If you widen the age rating bands for health insurance and then scale the tax credit based on age, haven't you kind of done nothing?

Obviously there's no way of being 100% certain about this because the GOP still hasn't actually presented their ACA replacement bill (and in fact, have been playing a rousing game of Where's Waldo with it all afternoon), but we do have a pretty good idea of what it's gonna look like, thanks to a recent draft version of the bill which was leaked a couple of weeks back.

The Kaiser Family Foundation has crunched the numbers and compared what things look like financial assistance-wise under the ACA, the HHS Secretary Tom Price's "Empowering Patients First" bill and the recent "House Discussion Draft" bill to see how the GOP versions size up...and it's not pretty.

“But the plans were on display…”

“On display? I eventually had to go down to the cellar to find them.”

“That’s the display department.”

“With a flashlight.”

“Ah, well, the lights had probably gone.”

“So had the stairs.”

“But look, you found the notice, didn’t you?”

“Yes,” said Arthur, “yes I did. It was on display in the bottom of a locked filing cabinet stuck in a disused lavatory with a sign on the door saying ‘Beware of the Leopard.”

--― Douglas Adams, The Hitchhiker's Guide to the Galaxy