NOTE: In light of some serious discussion with IBD's Jed Graham and a lot of thought afterwards, I've decided to run the "attrition" numbers two ways: "Current vs. April Paid" and "Current vs. April Total", for reasons I'll explain soon.

The main thrust of this article is general hand-wringing over how the state of Rhode Island plans on funding their ACA exchange after this year, although it's a bit confusing since it sounds like the problem has nothing to do with having the funding and everything to do with having permission to use it:

Enrollment starts on Nov. 15.

Not long after, the state will have to make its own big decision: how to finance the exchange.

Of the $23.4 million in federal funds budgeted for HealthSource RI this year, only $1,353,570 has been spent so far. The state anticipates — but does not yet have — federal permission to spend any of the remaining dollars after Dec. 31.

However, there's one data point that pops up smack in the middle of my current "mini-project", trying to lock down the current QHP enrollments in each state:

The numbers ranged from as poor as Florida losing 12% of their enrollments in just 2 months to as well as Maryland and Oregon seeing a 30%+ net increase in enrollees over the past 6 months.

Today I can add Kentucky to the latter list. She couldn't provide an exact current count, but according to the woman I spoke with at the kynect exchange (that's "Obamacare", Mitch!), the number of Kentuckians currently enrolled in private policies via kynect is "right around the same number it was at last spring, between 80-85 thousand".

Why has the law been such a flop in a state that had so much to gain from it? When I traveled across Mississippi this summer, from Delta towns to the Tennessee border to the Piney Woods to the Gulf Coast, what I found was a series of cascading problems: bumbling errors and misinformation; ignorance and disorganization; a haunting racial divide; and, above all, the unyielding ideological imperative of conservative politics. This, I found, was a story about the Tea Party and its influence over a state Republican Party in transition, where a public feud between Governor Phil Bryant and the elected insurance commissioner forced the state to shut down its own insurance marketplace, even as the Obama administration in Washington refused to step into the fray. By the time the federal government offered the required coverage on its balky HealthCare.gov website, 70 percent of Mississippians confessed they knew almost nothing about it. “We would talk to people who say, ‘I don’t want anything about Obamacare. I want the Affordable Care Act,’” remembered Tineciaa Harris, one of the so-called navigators trained to help Mississippians sign up for health care. “And we’d have to explain to them that it’s the same thing.”

OK, this is gonna be difficult for people to see, since the Medicaid spreadsheet is so wide (the link goes directly to the spreadsheet itself, which should help somewhat). First, scroll all the way to the right. Then scroll to the bottom. In the lower-right corner, you'll see the following:

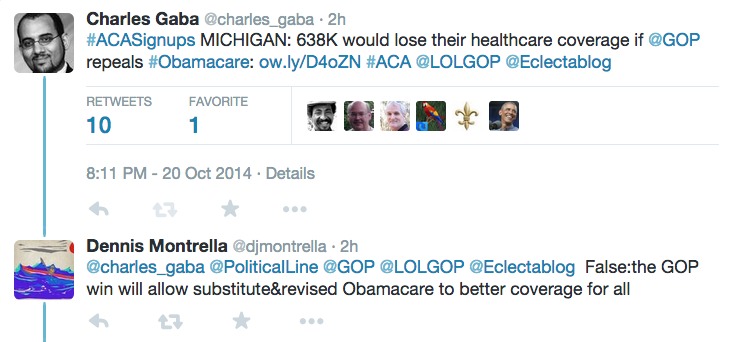

Last week I crunched the numbers and pointed out that if the Republican Party ever successfully completes repealing the Affordable Care Act, tearing it out "root & branch" as Mitch McConnell is so fond of putting it, that 638,000 Michiganders would lose their healthcare coverage in one shot.

Beneficiaries with Healthy Michigan Plan Coverage: 433,469

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of October 27, 2014

*Updated every Monday at 3 p.m.

Yup. We're up to over 646,000 Michigan residents who'd be pretty much screwed if the GOP gets its way.

In spite of their ugly technical problems, Cover Oregon was surprisingly consistent and reliable with their off-season enrollment updates, issuing them about once a week throughout the entire spring and summer. This came to a halt on September 29th, however; they didn't issue any updates at all throughout all of October. I assumed that this was because they were too busy shutting down the state exchange and moving everything over to Healthcare.Gov for the 2nd Open Enrollment period, and I'm sure they are. However, tonight I was pleasantly surprised to see that they have issued one more update after all, taking things all the way through...today:

October 28, 2014

Update: Private coverage and Oregon Health Plan enrollment through Cover Oregon

Medical enrollments through Cover Oregon: 416,056 Total private medical insurance enrollments through Cover Oregon: 105,055

Oregon Health Plan enrollments through Cover Oregon: 311,001

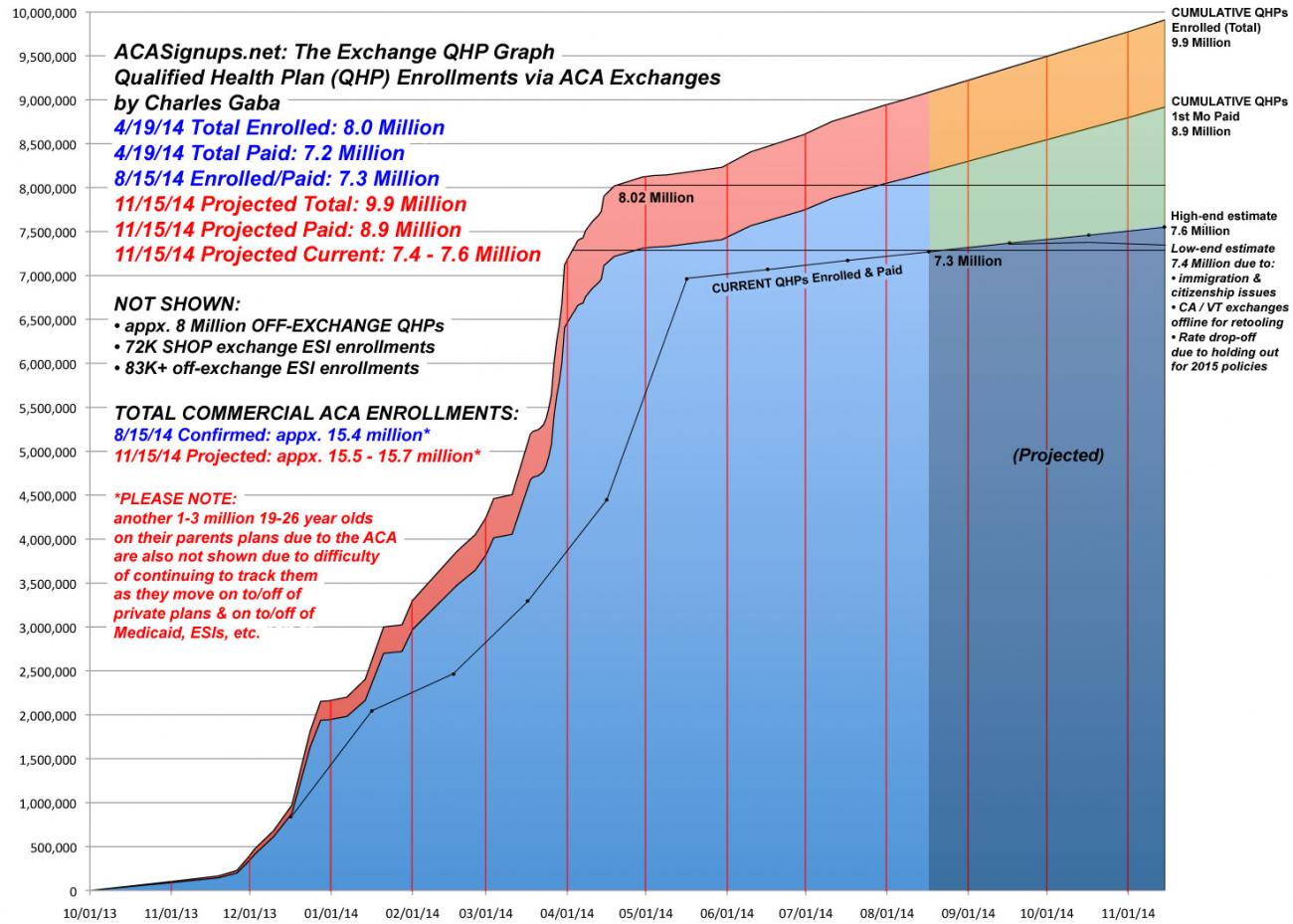

When HHS Secretary Sylvia Burwell finally revealed that 7.3 million people were enrolled in policies as of August 15th, most of my assumptions were confirmed...except that the attrition rate, which I had been assuming was around 3% per month, now seemed to be even lower, at 2%. However, I wasn't sure about this until now.

Today I added a whole slew of updated state-level current enrollment numbers, and now I have these for 10 states, comprising nearly 3.2 million of the original 8.02 million enrollees through 4/19/14, or almost 40% of the total. This strikes me as being a pretty good base to extrapolate the other 40 states (+DC) from.

I addressed Nevada's apparent attrition rate about a month and a half ago. At the time, it appeared to be a fairly ugly 7.7% per month...relative to the "high water mark" of paid enrollments they had achieved in July of around 38,000.

However, since then I've realized that given the high amount of churn during the off-season as people enter and leave the marketplace, a far more accurate measure is the number of current enrollees relative to the April tally, since that was the "8.02 Million Total / 7.06 Million Paid" figure that everyone was focusing on anyway. Doing it this way is also far more consistent, since there's a hard 4/19 number to compare against for every state instead of it being all over the map.

In the case of Nevada, I've just received word that the current number of people enrolled in exchange QHPs is exactly 32,460 as of mid-October.

Rounding out today's "Net QHP Attrition Rate" Trifecta is Indiana, which, while not as deep-red as Tennessee, a) also has a Republican administration; b) hasn't expanded Medicaid; and c) refused to set up their own exchange.

This makes it all the more of a positive surprise to see that their ACA exchange QHP attrition rate is even lower than Tennessee--in fact, it's under 1%!!

Excellent news!! I've posted exactly one (1) Tennessee-specific blog entry since I started this site a year ago, having to do with TN's possible caving on Medicaid expansion. Aside from that, I've had bupkus outside of the official monthly HHS reports during the First Open Enrollment period (OE1)...until today.

Today I learned that the number of Tennesseans currently enrolled in QHPs (as in currently in-force policies) via the federal ACA exchange stands at 125,704.

Minnesota's exchange (called MNsure and pronounced to rhyme with "insure") has had it's share of technical problems, but they haven't been nearly as bad as the 4 state-run exchanges undergoing full overhauls (OR & NV are scrapping theirs entirely; MA & MD started over from scratch). They got hit with some bad news recently when the largest insurer on the exchange decided to bail, although that appears to have had more to do with that company's poor business decisions than anything on MNsure's side.

However, they've continued to keep chugging along, quietly adding more enrollees to both private QHP policies (via qualifying life events) as well as Medicaid and MinnesotaCare (neither of which have any deadlines involved). Most relevant to myself, they're also the only exchange which has continued to provide consistent, regular enrollment data updates on a near-daily basis, which is manna from heaven from my POV.

Last year, New Hampshire had but a single participant in the federal ACA exchange: Anthem BCBS. This year, not one, not two, not three, but four other companies have joined in:

Two more insurance companies say they plan to sell policies in New Hampshire’s health exchange in 2015, bringing the total to five carriers. The suddenly crowded field is a sharp contrast to this year, when only Anthem is offering policies through healthcare.gov.

Harvard Pilgrim and Minuteman Health, both based in Massachusetts, announced their intentions to join the exchange earlier this year, and now the New Hampshire Insurance Department says Assurant Health and Maine Community Health Options have also submitted plans for regulatory review.

We don't have a full average-premium percentage breakdown like there are for other states, but this is certainly promising:

Today's New York Times has a pretty in-depth overview of how the ACA is doing. Overall it's very well done, though I do have a few quibbles about the sub-header "After a year fully in place..." because the law hasn't been "fully in place" for a year now, mainly because the employer mandate portion doesn't kick in until January (and most of the SHOP small business exchanges haven't been launched yet either).

Aside from that, though, it asks and tries to answer 7 major questions about where things stand:

Has the percentage of uninsured people been reduced?

Answer: Yes, the number of uninsured has fallen significantly.

Has insurance under the law been affordable?

For many, yes, but not for all.

Did the Affordable Care Act improve health outcomes?

Data remains sparse except for one group, the young.

Will the online exchanges work better this year than last?

Most experts expect they will, but they will be tested by new challenges.

Back in 2003, when the second round of the utterly unnecessary Bush Tax Cuts were doled out (jacking up the federal deficit for decades to come), I received my very own check from the IRS for something like $300 or so. I distinctly remember that it had, typed in the lower left-hand corner, "TAX RELIEF FOR AMERICA'S WORKING MEN & WOMEN".

As it happens, I donated the entire $300 to charity, since I had never asked for it and didn't want it. However, I always remembered the shamelessly partisan promotional nature of how it was done. A physical check with the actual dollar amount and a big, bold slogan referring to "relief" (the implication being, of course, that taxes are by their very nature a negative, awful thing which one needs relief from).

When you think of the flu, the cost of getting sick probably isn’t the first thing that jumps to mind. But coming down with the virus can prove pricey.

A visit to the doctor’s office can run $80 to $100—or more. If you need to head to the ER on a night or weekend for care, the tab can easily total $500.

...The good news is that you probably don’t have to pay a penny for the best defense against the flu. Under Obamacare, a flu shot is free as long as you have health insurance (though plans that were in place before the law passed in 2010, known as grandfathered policies, are exempt). It’s one of the preventive services that insurers must fully cover without charging you a co-pay or co-insurance—even if you haven’t met your annual deductible yet. Under Medicare, you also pay nothing.

Thanks to Margot Sanger-Katz for bringing this KFF study to my attention; Tricia Neuman has done an interesting study to try and predict how many of the appx. 7.3 million current ACA exchange policyholders are likely to make the move from their current policy to a different one (either through the same company or a different one).

She goes pretty deep in the weeds on some of it, but her takeaway is that, based on 3 other government healthcare programs (Federal Employee Health Benefits, Medicare Part D and the Commonwealth Care program in MA), it's likely that only about 7 - 14% of enrollees are likley to switch:

This is a rather awkward post for me, because it cuts to the heart of the main thing I don't like about the Affordable Care Act. As a single-payer advocate, and one who knows all too well the abuses by the health insurance industry in the past, I'm not exactly thrilled about this development. On the other hand, this news also shoots down Yet Another Talking Point® that FOX News/etc. have had about the law: That it would "ruin" the private insurance industry. The ACA has always been a strange hybrid of left-wing/progressive provisions (Medicaid expansion, tax credits to enrollees) and right-wing free market capitalism (the individual mandates and private, for-profit marketplaces). As such...

Even after the disastrous rollout of the healthcare.gov web site a year ago, health insurance companies and providers of medical care are reporting more promising profits as third quarter earnings emerge.

The Halbig/King federal suit cases have been off the radar for awhile now, but they're still swirling around in the ether, and will pop up again sooner or later. While a final ruling (by the SCOTUS either taking up one of the cases or refusing to do so) likely won't happen until next summer or so, the insurance companies and the HHS/CMS Dept. are understandably concerned about the ramifications of the possibile outcome, so they've taken some steps accordingly:

The agreements to participate in the federally-facilitated marketplace (FFM) that CMS sent to issuers last week include a new clause assuring issuers that they may pull out of the contracts, subject to state laws, should federal subsidies cease to flow. CMS did not say if the clause is meant as a safeguard against the potential impact of various high-profile lawsuits -- including Halbig v. Burwell -- that could end up in the Supreme Court next year, but stakeholders assume that is the point.

Gov. Gary Herbert announced Thursday that after months of negotiations, he has reached a final agreement with the Obama administration on his novel alternative to expanding Medicaid.

"They are giving us more flexibility than has been given to any other state in America. We are breaking some new ground," Herbert announced in his monthly press conference on KUED.

Herbert said he soon will send to the Obama administration a letter outlining the agreement they’ve reached on Utah’s alternative, his Healthy Utah plan.

The deal would help low-income Utahns earning up to 138 percent of the federal poverty level who are not covered by Medicaid buy private health insurance plans.

From the sounds of it, it looks like this will be set up along the lines of the Arkansas "private option" program, which basically amounts to using Medicaid funding to cover practically 100% of the cost of private QHPs.

As we head into the final few weeks before the 2nd Open Enrollment period, it looks like MNsure is the only state which is left posting regular off-season enrollment updates. Things are definitely tapering off (only 113 new QHPs over the past 6 days & 3,294 added to Medicaid/MinnesotaCare), but that's still over 3,400 more people with coverage.

latest enrollment numbers

October 22, 2014

Health Coverage Type Cumulative Enrollments

Medical Assistance 227,476

MinnesotaCare 78,321

Qualified Health Plan (QHP) 55,564

TOTAL 361,361

I wouldn't normally give much thought to the Daily Signal, seeing how a) it's an offshoot of the right-wing Heritage Foundation and b) the last time I analyzed one of their pieces it was this idiotic piece by Sharyl Attkisson. However, supporter Adam Goldstein asked me to check out their latest, so I did...and while it's heavily biased against the Affordable Care Act, I find it noteworthy that even these wingnuts are willing to concede that a) their own colleague, Ms. Attkisson, was pathetically wrong and b) the net reduction in the uninsured rate nationally thanks to Obamacare is actually off to a pretty good start:

Our analysis of the data is reported in more detail in our latest paper, but our key findings are that in the first half of 2014:

WASHINGTON -- Democratic Sen. Jeanne Shaheen refused to shy away from Obamacare on Tuesday in the first televised debate of the New Hampshire Senate race.

Shaheen, one of several vulnerable Democrats up for re-election in November, forcefully defended the health care law moments after Scott Brown, her Republican opponent, said he would fight to repeal it. When specifically asked if Obamacare was a proud achievement, Shaheen responded, "Absolutely."

"I think making sure that almost 100,000 people in New Hampshire have access to health care is real progress for people in this state," Shaheen said.

Many Republicans are caught in a quandary when it comes to the Affordable Care Act. They hate the fact that a black Democrat implemented their own law nationally, they hate poor people getting healthcare coverage at little cost to them and they hate middle-class people getting healthcare coverage at a price they can afford. However, they love getting elected/re-elected. So, what's a good Republican candidate to do?

Well, for Mitch McConnell, many GOP Governors and other Republican candidates, the answer seems obvious: Repeal the Affordable Care Act nationally while at the same time changing the laws at the state level to increase eligibility to the same 138% FPL (Federal Poverty Level) threshold included in the ACA.

Gov. John Kasich of Ohio said his comments about a Republican-led Congress being unlikely to repeal the Affordable Care Act — which commentators on the right and left pounced upon Monday — were taken out of context.

...Mr. Kasich, referring to repealing the Affordable Care Act, was quoted as saying “that’s not gonna happen.”

...“I’ve always thought if we got a majority we would repeal Obamacare,’’ he said. “My only point was they’d probably make an accommodation for Medicaid expansion.’’

...It is an open question how expanding Medicaid benefits as generously as the Affordable Care Act allows, to adults earning up to 138 percent of the poverty level, could be paid for without increased taxes and Medicare cost reductions also created by the health care law.

...“I’m in favor of repealing Obamacare,” he repeated. “That’s all I can tell you.’’

Beneficiaries with Healthy Michigan Plan Coverage: 424,852

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of October 20, 2014

*Updated every Monday at 3 p.m.

Obviously this is fantastic news; the state is up to 88% of the 477,000 Michiganders estimated to be eligible for the program.

However, when you add in the 213,000 residents of Michigan who are receiving tax credits via private healthcare policies through the Affordable Care Act...aka "Obamacare"...that's around 638,000 people who would lose their coverage if the Republican Party were to successfully repeal the law, which they've been dead-set on doing for 4 years now.

Last week I announced that I've started writing occasional pieces for HealthInsurance.org. Today they've published my 2nd entry, which is all about Kentucky, Mitch McConnell and the real-world impact on hundreds of thousands of people that repealing the ACA would have.

UPDATE:In my story, I noted that the Federal Government is picking up 100% of the tab for the expanded Medicaid enrollees for the first 3 years, and then thought that it dropped down to 90% for another 6 years, and then to the normal fed/state split after that (70/30 in the case of Kentucky).

Thanks to David M. for bringing to my attention this correction: The expansion program is an even better deal for the states than I thought, because apparently the Federal share only drops to 90% permanently (well, unless a future Congress messes around with that provision of the ACA, of course).

Things may be slowing down, but some people are still enrolling in 2014 QHPs just 1 month before the 2015 enrollment period opens; 162 Minnesotans from 10/8 - 10/16. In addition, Medicaid/MinnesotaCare has jumped by over 7,000 people:

latest enrollment numbers

October 16, 2014

Health Coverage Type Cumulative Enrollments

Medical Assistance 224,891

MinnesotaCare 77,612

Qualified Health Plan (QHP) 55,451

TOTAL 357,954

There's been a lot of fuss made about 2015 ACA exchange premium rates not being available at Healthcare.Gov until after the election. The presumption, of course, is that this is being done for political reasons. While this may be true, it could also simply be that there's a lot of different policy figures to plug into the federal system, and some states haven't even finalized their rates yet.

That being said, residents of some states can check out the 2015 premiums now and compare them against their current premium:

IDAHO: Idaho is the only state moving from HC.gov to their own exchange. Idaho residents can check out their 2015 rates directly via the state exchange site.

This is absolutely awesome...and extremely frustrating at the same time. Dan Goldberg and his chums at CNY have put together another extremely detailed breakdown of ACA enrollments in New York City, with QHPs, Medicaid and CHIP enrollees sorted out by individual zip code (a pretty herculean task given how many zip codes there are in NYC). Even more interesting (from my perspective, anyway) is that they've managed to get the current enrollment figures--updated through September. Since the NY exchange pointedly informed me back in June that they had no plans to release updated enrollment figures during the off-season at all, this is a huge development from my POV.

The only problem, of course, is that this map only gives the tally for NYC itself (about 8.4 million people total) not the rest of the state (about 19.6 million). Since my data is focused on the state-level numbers, this is frustrating; so close, and yet so far. I suppose I could extrapolate the numbers by multiplying each by 2.3x, but that doesn't work because the demographics are so vastly different between the two.

Anyway, for NYC itself, there's gobs of data-nuggety goodness to be found:

Regular readers may recall my thorough debunking of Sharyll Attkisson's ludicrous claim that only 3.4 million people out of the "38 million" who are "eligible for coverage under Obamacare" have actually received healthcare coverage since the law went into effect.

As I noted, these numbers were just a wee bit off. The "3.4 million" is actually more like "11.8 million", and while the "38 million" is actually reasonably close if you're only including those who were a) uninsured last year and b) who qualify for either Medicaid or tax credits via the ACA exchanges (more like 36.4 million), even this is stupid because no one in the Obama administration, HHS, CMS or the CBO ever claimed that all 36.4 million would be insured in the first year of the exchanges.

Research has shown that consumers "do think there is a difference," between for-profit and not-for-profit health plans, says the head of an industry group. But in the final rule on health insurance exchanges, CMS has declined to require that tax-status be disclosed.

Nonprofit health insurance plans continue to dominate customer satisfaction and quality lists, and they want consumers to know about it.

Bruce McPherson, president and CEO of the Alliance for Advancing Nonprofit Health Care, says federal and state health insurance exchanges should do more to make the tax status of health plans readily available to consumers.

And this is kind of important, because at the same time...

Colorado’s 2.0 “Kentucky-style” system that is supposed to simplify the way people get health insurance won’t be ready until days before the Nov. 15 open enrollment starts.

And as Colorado’s health exchange enters its busy season, a third “chief” has announced she’s leaving Connect for Health Colorado. Chief Executive Patty Fontneau departed in August. Chief Financial Officer Cammie Blais left two weeks ago. And Chief Operating Officer Lindy Hinman announced her resignation and plans to leave next month after open enrollment begins.

A provision of the Affordable Care Act precluding health insurers or companies in the “same controlled group of corporations” as a health insurer from holding exchange contracts raises questions about Optum working on Vermont Health Connect.

Concerns regarding Optum were raised at the federal level by Sens. Orrin Hatch, R-Utah, and Chuck Grassley, R-Iowa, the ranking members of the Finance and Judiciary committees respectively.

Basically just an overview of the new Idaho ACA exchange; ID is the only state moving from HC.gov to their own website for the 2nd year, giving them a unique perspective. Most interesting to me is that they're spinning the "autonomy/states-rights" angle, which was the whole reason for pushing states to set up their own exchanges in the first place:

CLARKSTON, WA – Leaders with Washington’s Health Care Exchange are preparing for the second open enrollment period, but at the same time they are still working on resolving billing and computer problems for 1,300 accounts from the first sign-up period.

This is very confusingly worded, because it makes it sound like all 3 companies have been operating on the HC.gov exchange when it turns out that only 2 of them have. Wellmark did not participate in the ACA exchange; the 19,000 customers referred to here have off-exchange policies which are still ACA-compliant:

Commissioner Nick Gerhart said today that he has approved premium increases from Wellmark Blue Cross and Blue Shield, CoOportunity Health and Coventry Health.

As I predicted in early September, Part Two of the "OMG!! GAZILLIONS OF POLICIES CANCELLED!!" freakout has commenced with 3 weeks to go before the election. Case in point: Colorado, where the state Insurance Commissioner sent a letter to "state Senate Republicans" yesterday (I'm going to assume that this was in response to their request, as opposed to the Commissioner voluntarily choosing to only inform the Republicans specifically) stating that a total of 22,000 policies are scheduled for cancellation due to non-compliance with ACA provisions:

Over 22,000 Coloradoans have had their health insurance canceled by Obamacare in the past month — and 200,000 are slated to be shut down in 2015, the state insurance department announced Friday.

The Colorado Division of Insurance wrote to state Senate Republicans Friday, notifying them that five more insurance carriers have ended plans for 18,783 more Coloradoans in just the last month. By far, the most canceled plans will come from Humana Insurance Company and Humana Health Plan.

When I last checked in on New Jersey back in June, their Obamacare Medicaid expansion tally was at around 229,000 people. This number has jumped to 343,000, out of around 466,000 NJ residents eligible for the program, or roughly 74%:

The 343,000-person expansion in Medicaid enrollment this year is nearly three quarters of the 466,000-person expansion-eligible population estimate by the Kaiser Family Foundation. But the 161,775 residents who enrolled through the marketplace are equal to just over one quarter of the estimated 628,000 eligible.

The other noteworthy thing here is that according to my own breakdown of the KFF estimates, New Jersey only has around 562,000 uninsured eligible for tax credits via the ACA, not 628K. However, this is mostly moot since those with insurance can also purchase QHPs via the exchange as well if they wish, so it's not really that big of a deal.

As for the 161,775 QHP figure, that dates back to last spring, so no update there.

In response to that, another Kentucky resident responded with a different perspective. Again, aside from cleaning up some typos and breaking it into more paragraphs for easier readability, I'm presenting it verbatim:

Mr. Gaba, I am also from Kentucky. I appeciate your fact checking of McConnell on the ACA and in most instances I would say that you are correct and he is not.

That said, I work in health care and we have also seen a boon in our bottom line due to decreased uncompensated care and bad debts. We are also in a poor county and almost 80% of the people were Medicaid recipients including some of my family members, so the ACA, at least in the short term has benefited us.

The Health Insurance Marketplace, Medicaid, and Children’s Health Insurance Program (CHIP) are critical in ensuring coverage for many individuals. As of August 15, 2014, 7.3 million Americans were enrolled in Marketplace coverage and had paid their premiums. This number represents a snapshot of a point in time, not the cumulative enrollment data from October 2013 through August 2014.

The other day I noted that Republican Congressman Tom Cotton of Arkansas, currently in a heated battle with U.S. Senator Mark Pryor to take Pryor's seat, is proposing not only stripping healthcare from the 200,000 people in his state who have gained healthcare this year thanks to the Affordable Care Act's Medicaid expanion provision (the "private option" in AR) as well as 40,000 people who are paying for policies via the ACA exchange, but is going even further by pushing for half of the pre-Obamacare Medicaid/CHIP budget to be slashed.

This would effectively result in up to 20% of the state's entire population losing their healthcare coverage...every one of whom is either poor or barely middle-class at best.

I nailed the total QHP enrollment figures during the off-season almost precisely (99% accurate on the total number, 96% accurate on the daily average)

The gross attrition rate has been only 1.6% per month, and the net attrition rate since April is an astonishingly low 1.8% over 6 months, or just 0.3% per month, which is far better than anyone (including myself) had imagined. Basically, people being added are almost entirely cancelling out people dropping coverage.

The list of technical improvements, new features, beefed-up staffing and ramped-up outreach efforts for the 2nd open enrollment period included in the press conference was extremely impressive (see the lower half of this entry from earlier today).

HOWEVER, there was one key data point which was quite surprising and disappointing to me: The initial payment rate.

I still have to sort through a bunch of data, but the main takeaway is this:

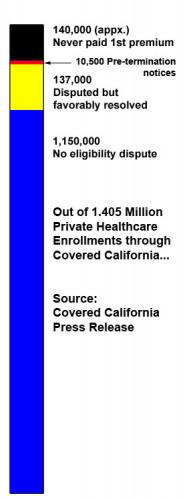

I projected the total California QHP enrollment figure to be around 1.68 million. The actual number is 1,414,668 (as of 4/15...see update at bottom of this page)plus 200,000 off-season enrollments from 6/1 - 9/30 plus an unknown number from the 46 days between 4/16 - 5/31.

I have no idea why they left those 46 days out of the press conference. Very odd.

There were 200,000 people who enrolled from June 1st - September 30th (122 days), or 1,639 people per day.

Assuming the missing 46 days saw a similar rate to the rest of the off-season period, that would be 1,639 x 46 = 75,394 additional enrollees.

Assuming this is correct, that's 1,614,668 + 75,394 = 1,690,062

Regular readers know that given the HHS Dept's going radio silent on the total ACA enrollment figures since the last official report was released back in May (which only ran through April 19th), I've been patching together bits and pieces of enrollment data from a handful of state exchanges, plus the occasional snippet of info from other states which has managed to find daylight from time to time.

Based on this, I've been projecting roughly 9,000 QHP enrollments being added per day during the off-season, translating into around 270,000 per month, of which about 90% eventually pay their first months premium. That translates to around 240K paid enrollees being added per month, which in turn is being roughly cancelled out by people dropping their policies after the first few months as they move on to other types of coverage (Medicare, ESI, Medicaid and so forth). Based on these estimates, there should now be a gross total of around 9.6 million enrollments, of which around 8.3 million have paid their first premium, and around 7.4 million who are currently enrolled as of October.

If there are currently 74,334 enrolled, that means there are 2% more enrolled (and paying) today than there were 6 months ago, which is right in line with my projections as well as the national 7.3 million figure mentioned by HHS Secretary Burwell as of August.

Meanwhile, Medicaid enrollees via the exchange are now up to 208,468. This is only a small increase over a month ago (around 1,400 people), but there's a very good reason for that:

First, I just want to take a minute to note that over the past year, I've discovered that while there's lots of good reporting on the ACA nationally, there are certain states which have one particular person who's the "go to" journalist for all things Obamacare-related.

A nifty summary of technical data points/specs behind the completely overhauled/revamped state ACA exchange website in Massachusetts after the first one failed spectacularly last year includes the following key points:

306,000 — the latest number of Massachusetts residents enrolled in temporary coverage. Will all these people need to get coverage through the state? No one knows, because there’s been no way to process their eligibility this year. But the total number of people trying to use the site during the three months of open enrollment could be around…

450,000 — which is 306,000 + the 100,000 or so people who are still in subsidized Commonwealth Care plans and another 33,000 or so residents who buy insurance through the Connector.

New Hampshire didn't start their ACA Medicaid expansion program until July 1st, and they haven't ramped it up at nearly as impressive a rate as other states like Kentucky, West Virginia or Michigan, but they're doing pretty well with it:

The state has estimated that 50,000 adults are eligible either through the state's managed care program for Medicaid or through a program that subsidizes existing employer coverage. Hassan says 20,035 have signed up since July 1.

According to the last official HHS enrollment report from back in May, as of April 19, 2014, Washington State had enrolled 163,207 people in private policies via their ACA exchange. Of those, 8,310 people never actually had their coverage start due to non-payment (WA requires payment of the first month's premium as part of the enrollment process, so I'm not sure what happened in these cases, but presumably there was some sort of credit card account approval glitch, insufficient funds in debit card accounts and/or the like).

In any event, that means the actual paid tally as of 4/19 was 154,897, or 95%, which is pretty darned good.

Well, a couple of days ago the WA exchange issued a press release regarding the renewal process for 2015, and included 2 key data nuggets. First up:

Just received the following email from a Kentucky resident. With his permission, I'm leaving out his name but am presenting it verbatim otherwise, with no further comment:

Thanks for discrediting good ol' Mitch. What a joke. I am a resident of Kentucky and here's how the ACA impacts my family with other opinions included for good measure.

We have read and heard the partisan battle waged for and against the Affordable Care Act (ACA). Much has been written and said, but I live it. I experience it. But to truly evaluate it requires good old-fashioned common sense. For some reason, this has gone the way of bipartisan politics.

Since I am a consultant paid on a per hour basis, I do not receive nor do I expect to receive health benefits through my employer. We purchased our health plan through the Kentucky Health Exchange – KYNECT: a marketplace to purchase health plans created via the ACA. We chose a silver plan.

For starters, returning customers will have to use the old, 78-screen application. New customers can use a simpler, faster, and more streamlined 16-screen version.

Health and Human Services officials said the site will automatically fill in existing consumers' information, such as their address and income, to help speed them through the process even though they have to use a more cumbersome application. That makes sense, as long as consumers take the time to change pre-populated information that has become outdated.

Boy, this syndrome of Republicans seemingly forgetting that repealing Obamacare would mean that hundreds of thousands of the very people they're hoping will vote for them would have their shiny new healthcare coverage torn away from them seems to be spreading fast. I'm calling it "repealnesia".

Yeah, I did a takedown of Mitch McConnell last night which gained some traction. However, that was more of a rant. Today, let's take a look at just how many times he flat-out lied about the Affordable Care Act (aka "Obamacare", aka "kynect"), shall we?

The yellow highlights are lies by McConnell. The orange highlights are either questionable/confusing statements by either him or the moderator, or otherwise just noteworthy:

(Moderator Bill) Goodman: has Obamacare and kynect been a boon or a bane for Kentuckians? Senator?

Mcconnell: Kentucky kynect is a website1. It was paid for by a $200 million and some-odd grant from the federal government. The website can continue. But in my view, the best interest of the country would be achieved by pulling out Obamacare root & branch and let me tell you why.

I'm pleased to announce that as ACASignups.net enters its' second year in operation, I've also started writing occasional pieces for healthinsurance.org:

Since 1994, healthinsurance.org has been a guide for consumers seeking straightforward explanations about the workings of individual health insurance– also known as medical insurance – and help finding affordable coverage.

The topic of insurance can be confusing, but we’re here with more information than ever: educational articles, expert health policy analysis, frequently asked questions about reform, a health insurance glossary, and guides to the health marketplaces and other insurance resources in each state.

I can't think of another publication outside of this one where what I do here is more appropriate. Looking at the list of other contributors, I'm honored to join their company.

My debut contribution to healthinsurance.org is an update regarding the citizenship/immigration data situation for Covered California enrollees...and the implications it may have for the rest of the country. Please take a look!

In addition to running ACASignups.net, I also happen to be a website developer by trade. I founded my website development company 15 years ago, which makes me an old man in the industry.

Given both of these capacities, I think I'm in a pretty good position to judge what's "just a website" and what isn't.

The kynect "just a website" wouldn't exist without Barack "Yeah, He's Black And He's The President Of The United States, It's Been 5 1/2 Years So Get Over It Already" Obama and the Democratic Party.

Those are two of the findings of a survey released today by the Center for Outcomes Research & Education at Providence Health Services. The goals were to understand who enrolled, assess their connection to care before and after enrollment and to understand their health. At the time of the study, 76,569 Oregonians had signed up through open enrollment.

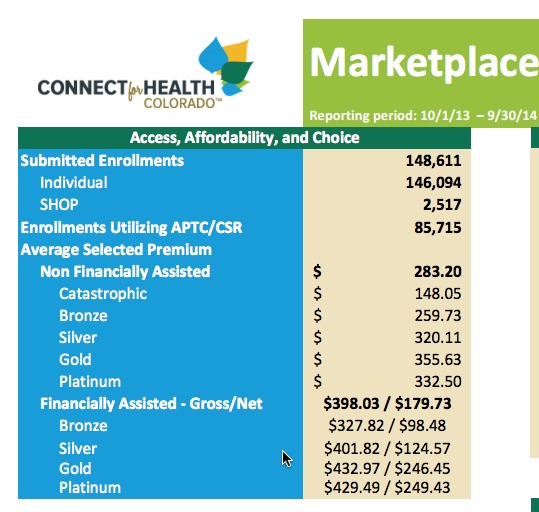

Colorado's official monthly metrics report is out, and shows that while off-season QHP additions have started to drop off as we approach the 2nd Open Enrollment period, they're still within my estimated range of 20-25% of the on-season rate.

Meanwhile, SHOP enrollments have inched above the 2,500 mark to sit at 2,517 covered lives as of the end of September.

Things are definitely tapering off as we come up to the new open enrollment period; Minnesota only added 46 more QHP enrollees in the past week, and just 2,087 more people to either Medicaid or MinnesotaCare. However, this does mean that the MNsure exchange has crossed the 350,000 total milestone:

latest enrollment numbers

October 7, 2014

Health Coverage Type Cumulative Enrollments

Medical Assistance 219,217

MinnesotaCare 76,275

Qualified Health Plan (QHP) 55,289 TOTAL 350,781

On the one hand, I've been expecting the daily QHP enrollment rate to drop off nationally as we approach November 15th; anyone who isn't truly desperate for coverage is likely to hold off at this point even if they do have a qualifying life event, given the numerous changes in companies, policies and rates which are going to be available. On the other hand, my "9,000 per day" estimate has always been a bit closer to the low end of the range (7,900 - 10,500 per day at the moment), so I have some wiggle room in this final month anyway.

Here's the good news: The "Healthy Michigan" program, Michigan's name for ACA Medicaid expansion, is up to over 415,000 enrollees, or 87% of the total eligible for the program. Hooray!!

Now here's the bad news: If the Republican Party has their way, every single one of those people will have their brand-new coverage yanked away from them...along with an additional 240,000 or more people (including myself) who are enrolled in private policies thanks to the Affordable Care Act.

Healthy Michigan Plan Enrollment Statistics

Beneficiaries with Healthy Michigan Plan Coverage: 415,504

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of October 13, 2014

*Updated every Monday at 3 p.m.

Combine the two, and that's over 650,000 Michiganders who will be royally screwed if Republicans get their way, or over 6.5% of the entire population of the state.

What arglebargle will come out of Mitch McConnell's mouth regarding trying to yank healthcare away from over half a million Kentuckians this evening?

The Big Senate Debate of the day promises to be the showdown in Kentucky between Republican Senate Minority Leader Mitch McConnell and Democratic Challenger (and current Secretary of State) Alison Lundergan Grimes.

Health industry officials say ObamaCare-related premiums will double in some parts of the country, countering claims recently made by the administration.

The expected rate hikes will be announced in the coming months amid an intense election year, when control of the Senate is up for grabs. The sticker shock would likely bolster the GOP’s prospects in November and hamper ObamaCare insurance enrollment efforts in 2015.

...The insurance official, who hails from a populous swing state, said his company expects to triple its rates next year on the ObamaCare exchange.

A query from a viewer said he had received health coverage through the Affordable Care Act. To Ernst, he asked, "Have you given any thought to how individuals in my situation won't lose coverage, should repeal occur?"

Ernst called Obamacare a "job killer" in Iowa that is "taking personal health decisions out of our hands and placing them with nameless, faceless bureaucrats in Washington, DC." That is to some degree true, but what about the guy's question? It was a reasonable concern; millions of people are now receiving subsidies to purchase health insurance. If Republicans repeal Obamacare, what happens to them?

Don't Feed the Trolls: A Special Entry for a Special Visitor

...A few days ago, I broke the cardinal rule of blogging and social media: I fed a troll. Specifically, I engaged in a back & forth with a guy who insisted that I don't have any clue what I'm talking about, that I "don't cite my sources" (insane, since every one of my sources is meticulously cited, dated and linked to)...and, in particular, that I'm "lying" about the number of California residents who have "fully" enrolled in exchange-based QHPs in California (and by extension, nationally). If you check the recent Disqus comments you'll see him pop up a few times today.

At first, he was arguing the "But how many have PAID???" line, which I've repeatedly addressed.

Interestingly, he was finally willing to (grudgingly) concede that yes, around 85% of "full enrollments" have indeed been paid to date.

However, he still insisted that the number of "full" enrollments only "counts" if the policy has actually been issued:

Kansas: Shocker: Pat Roberts lying about number of policies cancelled

In Kansas, yes, insurance companies were allowed to bump out non-compliant plans by at least a year...and indeed, Blue Cross Blue Shield of Kansas ended up not cancelling "between 9,500 - 10,000" of their policy holders after all.

So...that basically wipes out half of the "20K cancelled" claim already.

...Supposedly Aetna/Coventry and some smaller providers may have originally been planning on cancelling a bunch of plans as well...except that according to this article, Coventry never got around to doing so in the first place...

...That pretty much leaves BCBS KC and the other 10K. Based on the evidence at hand, my guess is that they likely reversed their cancellation decision as well...and if they did, that means that the actual number of Kansans who lost their healthcare policy in 2013 due to ACA noncompliance may have actually been as little as...ZERO.

Anyone who knows me, or who reads the FAQ (which is to say, hardly anyone), knows that I've never tried to hide my personal political views. I'm a proud progressive, active in the local Democratic Party, and have taken plenty of shots at Republicans here at ACASignups.net. However, I've tried very hard not to let that skew the data I report, and I've also taken plenty of shots at both HHS and/or the various ACA exchanges when they screw up.

Case in point: Just this morning I noted that the Vermont exchange is sending people to their website to pay bills when the site has been offline for weeks, and Oregon's disastrous exchange continues to provide embarrassment with news that they enrolled U.S. Senator Jeff Merkley--himself a proponent of the law--in Medicaid and somehow assigned him 97,000 children.

In any event, when I do go off-topic from time to time, it's generally for something innocuous.

Thanks to Jed Graham for bringing up an interesting point about the 2015 renewal-vs-new-enrollee issue earlier today.

His original point was that it's likely going to cause no end of headaches (especially to me) to try and keep track of the enrollment figures since there's going to be around 7.5 million existing enrollees to contend with (most of whom, I would hope, will renew their policies) plus the newly-added enrollees whose policies start in January or later.

When people shop online for health insurance through the Massachusetts Health Connector next month, they will have a radically different experience than the trouble they encountered last year, state officials promised Thursday.

Last year’s website, redesigned to meet the terms of the Affordable Care Act, never worked properly, leaving people unable to buy subsidized health insurance. This year, officials say, the newly rebuilt website will enable users to cruise smoothly from log-in to plan choice.

Thousands of Vermont Health Connect customers who signed up to pay health care premiums online recently received email notices directing them to pay through a website that is offline.

In any event, you can expect a slew of new "OMG!! X MILLION POLICIES CANCELLED!!" attacks this fall as well...just before the midterms. It's not so much that this is false--some policies will be cancelled--as heavily exaggerated, along with the "impact" of those cancellations (most people will do exactly what my wife and I did...simply replace the old policy which isn't compliant...with a new one which is compliant and offers more comprehensive coverage...in many cases at a much lower rate after tax credits are applied, as long as they enroll via the ACA exchange instead of directly via the company).

Remember that when you start seeing the campaign attack ads with absurdly ominous music playing over black-and-white footage of someone reaching into the mailbox and pulling out...a notice from their insurance company (DUN-dun-dunnnnn...).

On Tuesday, the New York Daily News posted a story about a man in New York who is suing Empire BlueCross BlueShield because the insurance policy he purchased from them is essentially useless. As the header summarizes it:

Jon Fougner says his simple search for a doctor through the insurance company website turned into a ‘Dickensian nightmare.’ Some doctors did not accept new patients, others never returned his calls, and some had wrong contact information listed on the Empire BlueCross BlueShield website, he claims. He accuses Empire of breach of contract, fraud and false advertising.

Now that Mitch McConnell is starting to feel the heat, he's decided to try and double down on the Evils of Obamacare by tying Alison Lundergan Grimes to the law (even though she didn't vote for it, seeing how she isn't, you know, a Senator yet).

So, he's started running a new ad in which a real-life doctor attacks Obamacare (mentioning in the "O" word 6 times in 30 seconds, if you include the on-screen text) while stating that Grimes supports it while McConnell wants to repeal it.

A year after shutting down the government, a group of Senate Republicans are pressuring House Speaker John Boehner (R-OH) to oppose any funding bill in the lame duck session that includes appropriations for a small program contained in the Affordable Care Act, potentially triggering another showdown.

I had to visit HC.gov for the first time in months today to check on something and was impressed by the mostly new interface and overhauled layout. Obviously a lot of the content changes are connected to prepping for the 2nd Open Enrollment Period (lots of "get ready!" and "upcoming deadlines!" and the like), but right off the bat I saw one important improvement: It's finally responsive. That is to say, HC.gov is finally optimized for smartphones & tablets.

the health insurance website will feature a streamlined application for most of those signing up for the first time. Seventy-six screens in the online application have been reduced to 16, officials said.

In an election where people like me are practically begging Democratic candidates in blue states to campaign on the Affordable Care Act, this is a jaw-dropping development.

South Dakota's Senate race normally would be considered a yawner. While the state does have a history of electing the moderate Democrats from time to time, it's pretty red for the most part, and no one was expecting Democrat Rick Weiland to have much of a chance against former Republican Governor Mike Rounds.

However, in an interesting development, independent candidate Larry Pressler has jumped into 2nd place in a recent poll. The thing is, Pressler isn't some no-name small timer; he's already a former U.S. Senator, serving for 3 terms before losing to Democrat Tim Johnson in 1996.

With Johnson retiring, his seat is open, and Pressler wants it back, so he's jumped back into the game. Here's the thing, though: Pressler used to be a Republican. In South Dakota.

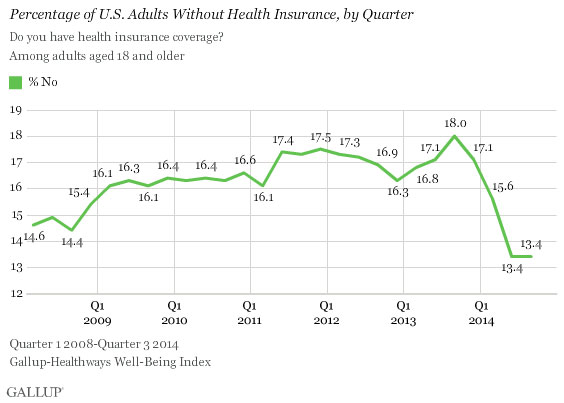

Gallup has just released their latest nationwide, fully-detailed quarterly insurance survey, and the results are...pretty much exactly what everyone in the real world (as opposed to FOX News, etc.) has been reporting for months now.

The uninsured rate for adults (Gallup doesn't survey kids under 18, of course), which hit a high of 18% last fall (just prior to the ACA exchanges launching) is holding steady at 13.4%, the same number it was at in the 2nd quarter of 2014:

The total U.S. population currently sits at roughly 316 million. Of that, around 76.7% are over 18, or about 242 million people.

18% of that is 43.6 million. 13.4% is 32.4 million...a net reduction of around 11.2 million uninsured, or about a 26% drop in the uninsured rate nationally.

There's nothing wrong with this AP article noting that getting an exemption from the $95 (or 1% of your taxable income) fine for not having ACA-compliant healthcare coverage could prove to be pretty complicated. Overall it's a fair assessment of some of the potential headaches involved in the hoops you have to jump through to get a waiver...

WASHINGTON (AP) — Millions of Americans may qualify for waivers from the most unpopular part of President Barack Obama's health care overhaul. But getting that exemption could be an ordeal.

Community groups are concerned about a convoluted process for waivers from the law's tax penalty on people who remain uninsured. Not everyone is complaining, however: Tax preparation companies are flagging it as a business opportunity.

The law's requirement that Americans carry health insurance remains contentious. Waivers were designed to ease the impact.

However, one line in the aticle made me chuckle:

But while some exemptions seem simple, others will require math calculations.

Wal-Mart told The Associated Press that starting Jan. 1, it will no longer offer health insurance to employees who work less than an average of 30 hours a week. The move affects 30,000 employees, or about 5 percent of Wal-Mart's total part-time workforce, but comes after the company already had scaled back the number of part-time workers who were eligible for health insurance coverage since 2011.

By an amazing coincidence, January 1st just happens to be the same day that new ACA-compliant policies purchased during the 2nd open enrollment period kick into effect.

...metal level/plan design, age, and geography, on health insurance plan premiums. At present, certain states are only reporting partial information about next year’s rates, and others are only reporting percentages that rates will change without sharing actual premium data. Unless otherwise noted, only individual health insurance filings containing rate information have been included in this analysis.

The most-recent CMS report, which only runs through June 30th, gave the net gain in Medicaid/CHIP enrollment as around 7.2 million, plus an additional 950,000 people who were added to Medicaid due to ACA provisions prior to October 2013. That's 8.15 million total over pre-ACA numbers.

There's two important points to keep in mind, however: First, again, that only ran through 6/30/14; there's been 3 solid months of additional Medicaid/CHIP enrollments since that time; and second, as of September there was a backlog of over a million people still waiting to be processed and added to the Medicaid/CHIP roles (1/3 of this in California alone).

I have no idea how much of this backlog has since been cleared up, but if CA's improvement rate is anything to go by, my guess is that most of it should be out of the way by the time the 2nd open enrollment period kicks in on November 15th.

Minnesota continues to quietly crank along as we enter the 2nd year of MNsure:

latest enrollment numbers

October 5, 2014

Health Coverage Type Cumulative Enrollments

Medical Assistance 217,535

MinnesotaCare 75,870

Qualified Health Plan (QHP) 55,243

TOTAL 348,648

Note that I'm not really even bothering to keep the Off-Season Projection Chart updated anymore; we're close enough to the 2nd Open Enrollment period that it seems a bit silly to bother (heck, I've already projected the graphs out through 11/15 anyway).

A couple of weeks ago there was a rather absurd-sounding report from a right-wing outlet called "The Pioneer Institute" which claimed that the Massachusetts Health Connector (their ACA exchange site) was going to cost over $1.1 billion over a 2-year period. I didn't really address it at the time, mainly because regardless of the disastrous experience of the MA exchange, that number just didn't seem grounded in reality. Sure enough, it turns out that estimate was about four times too high:

BOSTON - With the next open enrollment period set for Nov. 15, Gov. Deval Patrick on Monday said the state's troubled health care exchange website is fixed, at a cost of an additional $26 million to the state, bringing the federal and state total to $254 million in information technology costs.

...Consumers who log onto the Health Care Connector website will have a "full end-to-end shopping experience" for health plans on Nov. 15, Patrick said.

Louise Norris of HealthInsurance.org is quickly becoming one of my favorite ACA enrollment colleagues (and competitors, after a fashion). The other day she wrote a far better-detailed writeup listing all of the improvements that the various exchanges have made for the 2015 open enrollment period than I did; and now she's also done the grunt work of tracking down the "grandfathered policy" status in all 50 states...although she refers to these plans as being "grandmothered" instead of grandfathered, with the following distinction:

A simple cost comparison using data from the Medical Expenditure Panel Survey illustrates why Medicaid expansions can substantially affect premium prices for private insurance plans. Under national health reform, community rating regulations apply to purchases made on state exchanges by both individual consumers and small employers. In 2011, the health care costs of individuals getting insurance in these ways averaged $4,300 (with lower costs for the healthiest among them). By contrast, health care costs for nonelderly adults on Medicaid averaged $8,300 (even though Medicaid pays low rates to hospitals and physicians). If all Medicaid beneficiaries were shifted to the exchanges, prices for each purchaser would go up by more than $1000.

I haven't read the MEPS referred to, but I think the gist of it is this:

Considering that the vast majority of the policies sold on the ACA exchanges are from private, profit-based corporations already (plus some public-private CO-OPs as well as a handful of "not for profit" Blue companies), it seems a bit stupid to have to reiterate this point, but this could be a huge development:

NEW YORK (AP) -- Wal-Mart is taking one-stop shopping to another area: health insurance.

The world's largest retailer plans to work with DirectHealth.com, an online health insurance comparison site and agency, to allow shoppers to compare coverage options and enroll in Medicare plans or the public exchange plans created under the Affordable Care Act.

Wait, what's that?? Wal-Mart, the poster child for cold, heartless, maximize-profit-at-all-costs capitalism is going to start helping people enroll in that "socialist Obamacare" insurance?? How can that be? Why on earth would they do that?

Earlier today I noted that Idaho, which is the only state moving off of Healthcare.Gov onto their own exchange this year, is already allowing people to comparison shop 2015 policy plans. However, I just noticed something else on their new exchange site:

If you are among the 78,000 Idahoans who purchased a health insurance plan for 2014, we are here to help you renew your policy for 2015 on Idaho’s own health insurance exchange.

This is noteworthy because the official April 19th enrollment number in Idaho was 76,061. Assuming a 10% non-payment rate (which has been proven to be about right repeatedly over the course of the off-season period), that means around 68,400 of those enrollees paid their first month's premium. The gross number, of course, should be around 14,000 higher (assuming an off-season gross addition rate of around 87 per day), and of that grand total, it appears that 78,000 are still currently enrolled (otherwise they wouldn't need to renew their policy, would they?)

Oy gevalt. I made a big stink about this bizarro story when it broke back in June, so it behooves me to post a follow-up now when it appears that at least one Democrat in Virginia (well, besides the "Democrat" who was the subject of the original bribe offer) was basically guilty of the same thing that the state Republicans were:

RICHMOND — Virginia Gov. Terry McAuliffe’s top lieutenant apologized Friday after admitting that he had tried to keep a Democrat from quitting the evenly divided state Senate with the prospect of a lucrative state job for the senator’s daughter.

But it was not entirely clear to Richmond’s increasingly bewildered and antsy political class just what Chief of Staff Paul Reagan had done.

A couple of weeks ago I noted that for the 2015 Open Enrollment period, the (completely overhauled) Maryland exchange will not only be easing into their new website in several stages over several days (first allowing enrollments by phone, then letting brokers/navigators into the website, then health/social service dept. employees, and finally the general public), but they're also going to allow comparison "window shopping" starting 6 days before the official launch date, to give people extra time to figure out what policy they want to sign up for before actually purchasing it.

Then, a week ago I noted that Idaho--the only state moving from HC.gov to their own in-house exchange website for Year Two--is going one step further by opening up comparison shopping on October 1st...as in, 4 days ago. That's right, if you live in Idaho you can go kick the tires and pick out your plan if you wish right now at YourHealthIdaho.org, though you'll still have to wait until 11/15 to actually check out and complete the process.

G'mar Hatimah Tovah. Yes, I know I shouldn't be posting this on Yom Kippur Eve, but this seemingly minor news item means volumes to me personally.

I've spent 5 solid months pain-stakingly piecing together the best projection I could for off-season exchange QHP enrollments, using bits and pieces of data from a dozen or so states...mainly Minnesota, Oregon, Hawaii, Colorado and Washington State. In the absence of official updates from Healthcare.Gov (36 states) or the 2 largest state-run exchanges (California and New York), however, I was never completely sure about how close I was to the actual number, since the data I did have only covered perhaps 8% of the population.

Still, I eventually gave up hope that either NY or CA would bring their numbers up to date, forging ahead with my overall estimate of roughly 9,000 additional QHP enrollments being added daily during the off-season, 90% of those paying for their first month's premium, and roughly an equal number dropping their coverage sometime later...meaning that at any given time during the off-season, roughly 90% of the April 19th "official" number would be likely to still be enrolled and paying up.

I have the press release as well, but this article from the Daily Record does a good job of summarizing the numbers:

More than 81,000 Marylanders had enrolled in private health insurance on the state’s health exchange as of Sept. 20, officials said Friday.

That’s an increase of 2,425 individuals since August.

At the end of September, 376,850 people had gained Medicaid coverage during 2014. That’s an increase of 21,569 over the past month.

However, over the past year, some people have been dropped from the Medicaid rolls. People can become ineligible for the public insurance program if their income increases or if they experience other changes, like in age or household status.

So, the net increase in Medicaid enrollment compared to December 2013 is 262,979 people, according to officials with the Maryland Health Benefit Exchange.

It may seem a bit pointless to keep posting 2015 premium rate changes now that we're only 6 weeks away from the Open Enrollment period anyway (everyone will find out soon enough at this point), but the BS is still flying fast & furious, and the topic seems especially relevant in Minnesota's case since the largest insurer on the 2014 exchange, PreferredOne, has pulled out for Year Two:

Minnesota officials say the average rate for policies sold on the state health insurance exchange next year will go up 4.5 percent.

But, they say Minnesotans will still have access to the lowest average rates in the nation.

The five companies participating in the exchange range from dropping their averages by 10 percent to hiking them more than 17 percent.

They declined to say which companies are raising rates and which are lowering them.

BluePlus joins Blue Cross Blue Shield, HealthPartners, Medica and UCare this year.

Unfortunately, not only is there no way of doing a weighted average here since the current enrollees for the various plans aren't listed, I can't even post which companies are increasing or decreasing their rates. Ah, well.

A few weeks ago, I posted "Get ready for the "OMG!! GAZILLIONS OF POLICIES CANCELLED!!" Freakout" in which I pointed out that while yes, some policies which aren't in compliance with ACA requirements will indeed be discontinued this year, the odds are that the actual number will end up being far fewer than the GOP attacks will claim.

Well, right on schedule, here comes the freakout, and as I expected, the actual number of policies cancelled looks like it'll be missing a few zeroes from the attack headlines:

Thousands of Americans will see their health plans cancelled before the November elections in a development that could boost critics of ObamaCare.

The Morning Consult, a Washington-based policy publication, reported that nearly 50,000 people will lose their current health coverage in the coming weeks.

This story is beyond disgusting. The Michigan Republican Party has mailed out a hit piece on John Fisher the Democratic candidate for Michigan’s 61st House district. The mailer asks the recipient to call a phone number to complain about Fisher’s support of the Affordable Care Act. The number they give rings at the bedside of Fisher’s mother, 91-year-old Isabel Marie Kramb, who is in hospice care with congestive heart failure.

It finally happened. A new poll shows a majority that want Obamacare repealed. Sort of. And the Weekly Standard rejoices, with the headline "60 percent of voters want Obamacare to be repealed." Maybe they shouldn't rush to uncork that champagne. Because the pollsters here are McLaughlin & Associates. These guys. There's a track record here, reflected most recently in the internal polling they did for for Eric Cantor, showing him leading by 34 points just before he lost by 11. That's a 45 point error.

But so what if they got Cantor, Gabriel Gomez, Bob Dold, Mitt Romney, Richard Mourdock, George Allen and countless others wrong. They've got to get it right sometime, surely. Well, yeah, when you ask a question like this to get 60 percent approval:

Yes, I know I just updated Minnesota 2 days ago, and no, the latest numbers aren't terribly significant increases, but given that MN is the only state which has been consistently updating their data almost daily, with a nice simple breakout between QHPs, Medicaid and MinnesotaCare (a sort of quasi-Medicaid/QHP hybrid allowed for by the ACA), I figured I owed it to them to provide an update which matches their numbers up precisely with Day 365...exactly 1 year to the day since the exchanges launched last October:

enrollment update

latest enrollment numbers

September 30, 2014

Health Coverage Type Cumulative Enrollments

Medical Assistance 214,071

MinnesotaCare 75,013

Qualified Health Plan (QHP) 55,148

TOTAL 344,232

The Affordable Care Act includes several reinsurance programs that were supposed to help insurers mitigate the risk of mispricing their policies as they ventured into the strange new world of selling insurance on the government exchanges. The administration is leaning hard on these programs to keep insurers in the game, allowing payments out to be higher than payments in, and otherwise substantially reducing the potential losses that insurers can experience when selling exchange policies.

...The GAO responded that the payments are indeed legal, but for them to be legal again in 2015, the appropriations language for 2015 would have to be similar to this year’s language.

But even as Obamacare found its sea legs nationally and boasted solid first enrollment numbers in recent weeks [reminder: article is from April], it still came as a surprise to local political watchers when a Kentucky Democratic congressional candidate picked up the ACA baton and used it to bash the GOP incumbent that she is challenging. Elisabeth Jensen, the presumptive favorite to take on Lexington Congressman Andy Barr this November, emerged last week as the first federal candidate in the region—and one of only a few in the entire country—to broadcast a campaign ad championing health care reform, and attacking her opponent for voting more than a dozen times to repeal it.

The headline is a bit tongue-in-cheek, of course; in spite of Republican "Euro-Socialist" stereotypes, not every country in Europe is "socialist" (and even then, "socialism" has many different flavors/ranges just as "capitalism" does). Still, the irony of this development is rather amusing on the 1-year anniversary of the ACA "Obamacare" health insurance exchanges:

Swiss voters resoundingly rejected a proposal to move the country to asingle-payer system on Sunday. Instead, the country will keep its private health insurance system, which looks a whole lot like Obamacare.

Two-thirds of Swiss voters opposed creating a state-run health plan in the national referendum.

...For a country with a relatively small population (8 million), Switzerland comes up a shocking amount in debates over American health care. That's probably because the Swiss health care system looks pretty similar to the one Obamacare sets up.

OK, this isn't particularly dramatic given that I've already projected the cumulative total QHP figure to hit around 9.9 million by November 15th, but it's still nice to mark the occasion of another milestone being hit. By my best estimates, assuming 9,000 people enrolling in private Qualified Health Plans via the various ACA exchanges every day during the off-season, the grand total should have hit the 9.5 million mark right around midnight last night.

Of those 9.5 million, I estimate that around 8.2 million of them have paid their first month premium already, with another 300K or so who will do so sometime this month. I further estimate that the current number enrolled (after subtracting those who have dropped their coverage after the first month) should be around 7.4 million at the moment:

At the end of August, Illinois' Medicaid expansion program was up to around 452,000 people (including 93,000 transferred over from the existing CountyCare program). As of the end of September, that total was up another 16,000:

The video also coincides with the release Tuesday of new data by Quinn’s administration that showed 468,000 people enrolled in the expanded Medicaid program since last year, more than double original forecasts.

Of course, the larger point of the article in question is that if Democratic Illinois Gov. Quinn's Republican opponent had been calling the shots, he would have told all 468,000 of his fellow Illinoisians (?) to go pound sand:

SPRINGFIELD — Newly surfaced video of Republican Bruce Rauner obtained by the Chicago Sun-Times shows him telling conservative activists in Lake County last year that, as governor, he would have blocked Gov. Pat Quinn’s 2013 expansion of Medicaid.

Deaconblues provides another article with a similarly curious private enrollment update. I just reported that Ohio's 2014 open enrollment tally was apparently several thousand people higher than originally thought. Now it seems that the same is true in Alaska:

When the ACA open enrollment period ended for 2014, approximately 16,000 Alaskans had purchased individual health insurance plans, with nearly 9,000 receiving federal subsidies through the Federally Facilitated Marketplace.

The official HHS report gave Alaska's number as 12,890 as of 4/19...this is 24% higher than that. The first thing which crossed my mind is that the 16K figure might refer to the current gross enrollment figure, which should indeed be about 18% higher than it was in mid-April nationally. However, the fact that the article itself is an extremely anti-ACA screed by the Alaska Commerce Commissioner makes me pretty confident that she wouldn't try to make the actual enrollment numbers any better than they actually were.

OK, this is a pretty minor update, but according to the last HHS report, as of 4/19, Ohio's official QHP tally stood at 154,668. However, according to this article, it was a few thousand higher than that:

About 157,000 Ohioans signed up for health plans through the federal exchange during the first open enrollment period, which ran from Oct. 1, 2013 into March, 2014. In January, Ohio expanded Medicaid under Obamacare to cover more low-income adults. More than 360,000 people have already enrolled around the state through that new eligibility. And most of the doom and gloom predictions about the Affordable Care Act haven’t come true. Premiums aren’t through the roof, and the website, pretty much works as the federal government prepares for a new round of open enrollment starting Nov.15.

Again, pretty minor stuff, but as we enter the 2nd year of the ACA exchanges being open (slightly different from the 2nd open enrollment period, of course, which doesn't start for another 6 weeks), I figure it's a good idea to get some little details up to date.

Republican U.S. Senator Pat Roberts is scrambling for his political life after the Kansas Democratic Party pulled off a clever maneuver by deliberately dropping out of the race in order to shore up support for independent challenger Greg Orman (who may or may not caucus with the Dems, but would still be a huge step up from Roberts).

Anyway, Roberts has gone on the attack against Orman with a rather lame attack ad trying to paint Orman as an Obama/Pelosi/Ultra-Leftie Liberal, bla bla bla.

Aside from general Obamacare bashing, the ad makes one interesting claim: That "20,000 Kansans lost their healthcare because of" the ACA. The headline accompanying the narration reads "Obamacare cancels almost 20,000 Kansas health care plans" and cites "Kansas Watchdog" from 10/31/13 as the source:

When I last checked in on New Mexico's Medicaid expansion program, they were at around 55% of the total eligible. As of late August (judging by the Sept. 1st byline on the article), that number was up to 71%:

New Mexico projected that Medicaid expansion would sign up 219,000 new enrollees over a six-year period. In the first year alone (2014), they have already signed up 155,000, 71% of the best-case six-year estimate.