Last year, there was roughly a 13% net attrition rate from the end of the 2015 open enrollment period and the end of March, from 11.7 million down to about 10.2 million over a 5-week period (2/22/15 - 3/31/15).

This year, as of the end of the 2016 Open Enrollment Period on January 31st, just shy of 12.7 million people (12,681,874 to be precise) had selected Qualified Health Plans (QHPs) via either the federal exchange (HealthCare.Gov) or one of the dozen or so state-based exchanges (Covered California, kynect, MNsure and so forth). A flat 13% drop should have resulted in the number still effectuated as of the end of the first quarter (3/31/16) having dropped to just barely over 11.0 million (11,033,230 to be precise).

While I was generally supportive of the idea overall, I also concluded that:

For me, however, ColoradoCare addresses many of the criticisms I've had of Bernie's plan. I'm not necessarily "endorsing" it (I still have a lot more to learn about the details and the criticisms before I can do so), but the bottom line is that it's more realistic and far better thought out than Bernie's national plan is. This is the best opportunity for achieving single payer that you're likely to see anytime soon.

The Kaiser Family Foundation released their monthly tracking poll today. In addition to the usual questions about the ACA (spoiler: Republicans generally don't like it, Democrats generally do, and there's absolutely no consensus about what the public wants to do about it anyway), they also mixed things up a bit by asking timely questions about the Zika virus and increasing insurance policy premiums.

Here's the one which I find the most depressing...but also the least surprising:

Overall, nearly nine in ten (88 percent) Americans say they are concerned about increases in the amount people pay for their health insurance premiums. This is followed closely by the percent who are concerned about increases in the costs of deductibles (85 percent), increases in what the nation as whole spends on health care (83 percent), and increases in prescription drug costs (82 percent). Fewer but still large majorities of insured Americans are concerned about increases in spending on government health insurance programs (74 percent) and increases in the amount employers pay for their employees’ premiums (71 percent).

A special session for Medicaid expansion will have to wait, Gov. Dennis Daugaard announced Wednesday.

After a weeks-long effort to lobby enough lawmakers to get the proposal approved in the Statehouse, Daugaard announced in a statement that he wouldn't call lawmakers back to Pierre.

Citing the upcoming presidential election that could result in substantial changes to the federal health insurance program for needy people, Daugaard said a special session was off the table.

“We have a good plan that would increase health care access at no additional state cost and guarantee that the federal government won’t shift its responsibility to pay for Native American health care to the state,” Daugaard said in a statement. “Still, I have heard from legislators that they would like more time to study this plan and in particular want to wait to consider the issue until after the presidential election. For that reason, I will not be calling a special session to take up this issue.”

The Supreme Court, in an opinion written by Chief Justice Roberts, upheld by a vote of 5 to 4 the individual mandate to buy health insurance as a constitutional exercise of Congress's taxing power. A majority of the justices, including Chief Justice Roberts, agreed that the individual mandate was not a proper use of Congress's Commerce Clause or Necessary and Proper Clause powers, though they did not join in a single opinion. A majority of the justices also agreed that another challenged provision of the Act, a significant expansion of Medicaid, was not a valid exercise of Congress's spending power as it would coerce states to either accept the expansion or risk losing existing Medicaid funding.

UPDATE: This story has, thankfully, gone quite viral since I originally posted it yesterday morning. One important clarification: I estimated the monthly cost for treatment at around $5,200. According to Ms. Nichols in this local story about the situation in the Clarion-Ledger, the cost for her daughter’s treatment/medication is around $2,000; the balance appears to be for her husband, who also has diabetes. This actually makes the family more sympathetic, because she’s only asking for state assistance for her daughter’s portion of the bill.

In addition, according to the updated local story, the message appears to have gotten through to Rep. Guice (at least to the point that he's issued an apology, anyway):

Guice, who told The Clarion-Ledger Tuesday morning "I don't do interviews" and declined to comment, issued an apology Tuesday night.

1. Virtually all of those enrolled as of yesterday, a total of 189,000 by day's end, were transfers from existing limited-benefit public plans. These include 132,000 enrollees in Take Charge Plus, a program focused mainly on family planning, along with a few free office visits; and 56,000 from the Greater New Orleans Health Connection (GNOHC), a no-cost primary care program for low income people in the greater New Orleans area. GNOHC does not provide drug or hospital coverage.

...which is perfectly fine as well; it still lifts a huge financial burden off of the state while streamlining and consolidating enrollees into the larger Medicaid program itself.

Anyway, according to their latest report, when you add up the "effectuated enrollments WITH and WITHOUT APTC/CSR" (medical only), it totals 143,430 people as of June 9th, 2016...a slight drop from the 146,000 figure as of the end of April. As I noted last month, however:

I'm still waiting on the 2017 requested rate changes for Minnesota's individual market, but there's one carrier which won't be asking for any changes: Blue Cross Blue Shield of Minnesota:

Minnesota's largest health insurer, Blue Cross and Blue Shield of Minnesota has decided to stop selling health plans to individuals and families in Minnesota starting next year. The insurer explained extraordinary financial losses drove the decision.

"Based on current medical claim trends, Blue Cross is projecting a total loss of more than $500 million in the individual [health plan] segment over three years," BCBSM said in a statement.

The Blues reported a loss of $265 million on insurance operations from individual market plans in 2015. The insurer said claims for medical care far exceeded premium revenue for those plans.

But a funny thing happened on the way to the governor's office: Bevin's anti-Obamacare rhetoric started to tone down as Election Day approached. And in the months since he's been chief executive of Kentucky,instead of ripping up Obamacare out of his state, Bevin is making alterations to how the law works there and leaving its core elements and benefits in place.

My home state of Michigan has finally published the "Part II - Consumer Justification Narrative" carrier filings for 14 of the 15 carriers offering individual market plans next year. The combined total number of current enrollees comes in at around 390,000 including both on and off-exchange numbers. Last year, Michigan had 560,000 people on the ACA-compliant individual market, so it's important to note that there's likely at least 170,000 people missing from this analysis. However, many of these are likely found here:

UnitedHealthcare is pulling out of the MI market (unknown number of enrollees)

Celtic, Consumer's Mutual, HealthPlus and Time Insurance are all long gone

While I have the data for "Priority Health Plan", their counterpart, "Priority Health Insurance Co." has an unknown number of additional enrollees...and an unknown rate hike request (I don't know if it just hasn't been added to the database yet or what).

It should be noted, however, that last year, "Priority Health Insurance Co." had only about 1/10th as many enrollees as "Priority Health". If that ratio holds up this year, that should only be around 9,000 people, which is unlikely to skew the statewide average up or down by much.

With that in mind, here's how the requested hikes shake out in the Wolverine state for the bulk of indy market enrollees next year:

That's the subheadline of Jonathan Cohn & Jeffrey Young's story this morning about the kind-of, sort-of "replacement plan" for the ACA which Paul Ryan and the House Republicans have finally come up with, more than 6 years after the ACA was signed into law:

The plan, which isn’t legislation and is more like a mission statement, lacks the level of detail that would enable a full analysis, but one thing is clear: If put in place, it would almost surely mean fewer people with health insurance, fewer people getting financial assistance for their premiums or out-of-pocket costs, and fewer consumer protections than the ACA provides.

It’s difficult to be certain, because the proposal, which House Speaker Paul Ryan(R-Wis.) will talk up at the American Enterprise Institute in Washington on Wednesday, lacks crucial information, like estimates of its costs and effects on how many people will have health coverage.

The Idaho insurance department website has made this really easy for me. Most states either don't provide the requested rate hikes at all (forcing me to track them down via a slew of SERFF filing forms) or, if they do provide the rate requests, they don't provide the actual enrollment numbers for each carrier, making it very difficult to run a weighted average.

In the case of Idaho, they don't give the enrollment numbers, but they've already ran the average and posted the weighted number for me! Better yet, they've done this for both the Individual and Small Group markets:

One of the biggest challenges the HHS Dept. has encountered when it comes to enrolling people in ACA exchange policies has been encouraging (or "goading" depending on your POV) millennials into signing up. This is important for several reasons:

Hmmm...this is kind of interesting. As I noted a few weeks ago, here's what the QHP enrollment pattern has looked like in Minnesota since the end of the 2016 Open Enrollment Period:

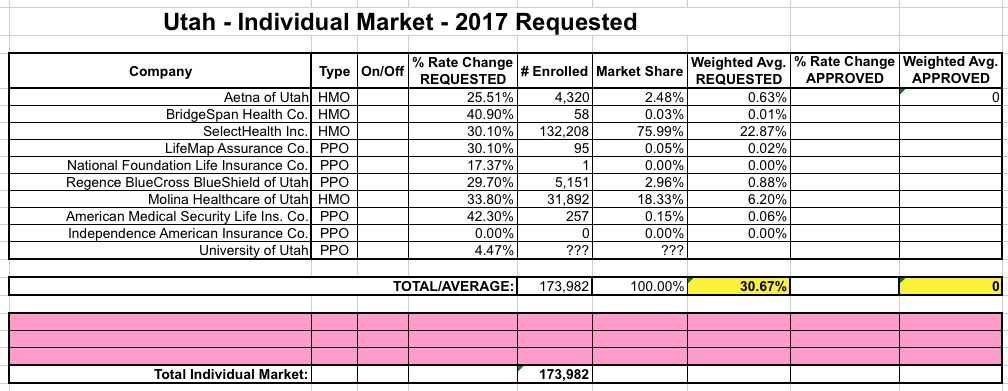

UPDATE 6/22/16: I've been informed that there was a coding glitch with Utah's website which prevented several carrier rate filings from being listed. I've gone back and plugged in the additional carriers, which account for about 32,000 more Utah residents...but which only moves the weighted average slightly, since Molina's request is fairly close to the 30% average I already had estimated.

This leaves around 93K unaccounted for. Some of them are presumably enrolled via University of Utah plans; U of U's enrollment numbers are redacted, and while the Utah site claims a 0% rate hike, the RR.HC.gov database lists it as 4.47%.

Also, as far as I can tell, "American Medical Security Life Insurance Co." is a branding for UnitedHealthcare, which should clear up that confusion.

The Widespread Slowdown in Health Spending Growth Implications for Future Spending Projections and the Cost of the Affordable Care Act

The United States is on track to spend $2.6 trillion less on health care between 2014 and 2019, compared to initial projections made right after the 2010 passage of the Affordable Care Act (ACA).

The Issue

The report uses health expenditure data produced by the Centers for Medicare and Medicaid Services and consistently adjusts in each year for the absence of the sustainable growth rate system for physician payment rates in Medicare.

UPDATE: It turns out that Humana is not dropping out of Michigan entirely; they're only dropping their PPO plans, not their HMOs.

I noted last month that like UnitedHealthcare, Humana is pulling out of the individual market in multiple states next year. Unlike United, however, both the number of states and the number of enrollees impacted by Humana's withdrawl is fairly nominal; at the time I counted 5 states and around 25,000 total enrollees. Since then, Humana has confirmed that they're also dropping out of Colorado (9,914 enrollees), for a total of roughly 35,400 people nationally.

Today, I've confirmed that Michigan can be added to the list, impacting 1,717 people enrolled in off-exchange PPO plans. This brings the total to around 37,000 nationally:

Here's some relatively good news! Ohio's 2017 requested rate filings have finally been published, and considering that some other states are looking at weighted average requested increases of 30%, 40% or even as high as 56%, Ohio's 13.1% average is actually refreshingly low by 2017 standards.

It's actually even better than that, because as you can see below, I haven't been able to track down the actual current membership number for "Buckeye Community Health" (aka Ambetter)...and Buckeye is asking to lower their rates slightly, by around 1% on average. To get an idea of how this could impact the statewide average:

Assuming 0 enrollees: No impact at all; 13.1% average.

Assuming 10,000 enrollees: Would reduce avg. to 12.4%

Assuming 50,000 enrollees: Would reduce avg. to 10.1%

Assuming 100,000 enrollees: Would reduce avg. to 8.1%

Again, without knowing how many people Buckeye/Ambetter actually has currently enrolled, it's impossible to say what the weighted statewide average is...but I can say that it's no more than 13.1%.

Oregon was the second state to publicly announce the rate changes their carriers are requesting for the 2017 individual and small group markets. The overall weighted average request on the individual market side came in at a requested 27.5% increase, while the small group market requests had an average increase of just 1% overall (I didn't weight the small group enrollment numbers at the time, but have done so below).

Yeah, yeah, I know; a test server for Healthcare.Gov was successfully hacked into recently; no sensitive data was stolen, but Security was Breached, etc etc etc.

No, I'm not shrugging the incident off. I'm the one who called Hawaii's state exchange website out for taking over a week to resolve their own Heartbleed SSL vulnerability last spring. Yes, security is very important, especially with personal financial, medical and citizenship data. Hopefully the HHS techies are eliminating vulnerabilities, beefing up security and so forth.

I'm swamped with my day job at the moment, so I don't have a whole lot to add to the discussion at the moment...

The Affordable Care Act's exchanges have not been a bust for every health insurer. Florida's Blue Cross and Blue Shield affiliate made a profit of almost a half-billion dollars on the ACA's new individual plans last year.

The substantial ACA exchange losses exhibited by large health insurers—such as Health Care Service Corp., Highmark, Humana and UnitedHealth Group—have emboldened the law's critics and worried investors about whether the new marketplaces will ever achieve sustainability.

Yet many other companies, including Medicaid insurers Centene Corp. andMolina Healthcare and now Florida Blue, have had no difficulties making money on the new ACA plans, which often have narrow networks of hospitals and doctors as well as high deductibles.

I already knew that Massachusetts was among the 30-odd states that UnitedHealthcare was dropping out of. However, it turns out that United is currently covering fewer than 500 of MA's exchange enrollees (considering that MA's entire individual market was only 72,000 people 2 years ago, and exchange enrollment alone is currently 224,000, I'd imagine that there aren't too many off-exchange United enrollees on top of those 500).

In addition, Guardian and MetLife are dropping off of MA's dental policy exchange, although according to their monthly report, neither one has any market share via the exchange this year anyway (Altus and Delta seem to make up 100% of the total). (correction: I was looking at the individual dental exchange; Guardian/MetLife are on the small group exchange this year)

The MA exchange reports an impressive 94% enrollment retention rate year over year:

The Massachusetts Health Connector has posted their latest monthly enrollment report, and the news is good. As I note every month:

Unlike most states, the Massachusetts Health Connector has not only seen no net attrition since the end of Open Enrollment, but has actually seen a net increase in enrollment...mainly due to their unique "ConnectorCare" policies, which are fully Qualified Health Plans (QHPs) but have additional financial assistance for those who qualify and which are available year-round instead of being limited to the open enrollment period.

House Republicans’ ObamaCare replacement plan will not include specific dollar figures on some of its core provisions, and will instead be more of a broad outline, according to lobbyists and aides.

The plan, set to be released next week, will include a tax credit to help people afford insurance and a cap on the current exclusion of employer-based health insurance plans from taxation.

However, it will not include specific dollar amounts on how large the tax credit would be, nor will it note which employer health insurance plans would be subject to taxation, lobbyists and aides said.

Speaker Paul Ryan’s (R-Wis.) office declined to comment on the plan ahead of its release next week, and noted it is still being finalized.

Republicans have said previously they will not be introducing their ObamaCare replacement plan in the form of a bill, but will instead release a white paper that is less detailed than legislation would be.

CMS Announces $22 Million in Affordable Care Act Funding for State Insurance Departments

Awards will help states enforce Affordable Care Act consumer protections

Health insurance companies that want to raise rates more than 10 percent next year will get an extra dose of scrutiny from Alabama regulators this year – for the first time since the marketplace launched in 2013.

Under Obamacare, states were supposed to implement systems for reviewing, and in some cases rejecting, rate increases that exceed 10 percent. Alabama was one of six states that didn't create an effective rate review program, despite receiving a $1 million grant to bolster oversight at the Department of Insurance, according to the Centers for Medicare & Medicaid Services.

After crunching the numbers for the requested rate changes (OK, rate hikes) across 31 states & DC, it looks like it's gonna be awhile longer for the remaining 19 states to post their rate filings publicly. For instance, while Michigan's SERFF database has had a whole mess of rate filing stuff posted for weeks now, none of them appear to include the two pieces of crucial data that I need for this project: The actual requested average percentage rate changes and the actual number of current lives covered by those policies...and likely won't for at least another week:

2017 Rate Filings - Individual Products - ALERT

The 2017 Individual Product filings are not yet complete. Partial filing information was submitted by issuers on May 9, 2016.

Thanks to Richard Mayhew of Balloon Juice for bringing this to my attention: This morning, Sabrina Corlette and JoAnn Volk of the Center on Health Insurance Reforms posted an amusing but also highly educational real-world example of the sort of non-ACA compliant healthcare plans that outfits like "Freedom Life" (aka "National Foundation" aka "Enterprise Life" aka "USHealth") specialize in...which also happen to be the exact types of plans that HHS is trying to keep a lid on with their recently-announced policy change.

Gun rights activists are constantly criticizing gun safety activists for not understanding the distinction between an "automatic" weapon, a "semi-automatic" weapon, a "machine gun", an "assault rifle" and so forth. I admit that I know very little about guns other than that their primary purpose...their only purpose, really...is to either kill or wound people or animals or, alternatively, to threaten to kill or wound.

Gun rights activists also constantly point out that you can kill/injure people with other items, such as knives, baseball bats, box cutters and so forth. This is true. However, unlike guns, those items actually have a useful primary purpose besides to kill or injure. If you remove baseball bats from someone's hands, they can't play baseball. If you remove knives from their hands, they can't slice bread.

If you remove a gun from their hands, the only thing they can't do is...shoot stuff.

By my count, Tennessee has a total of 6 companies offering individual policies this year (Aetna, TRH, BCBS of TN, Cigna, "Freedom Life" (hah!) and Humana. UnitedHealthcare is dropping out next year, leaving at least 37,000 people to switch to a different policy (this is based on this article in the Tennessean, which claims that United currently has 15.76% of the On-exchange individual market in Tennessee). TN had 269,000 people select exchange-based QHPs during the 2016 open enrollment period. Assuming around 13% net attrition since then, that leaves around 234,000 current enrollees on the exchange. If United holds 15.76% of those, that's around 37,000 poeple.

Hmmmm...I'm still waiting for the Michigan Dept. of Insurance to publicly post the 2017 requested rate hikes (they aren't due until June 20th, apparently), but in the meantime, Blue Cross Blue Shield of Michigan (the largest insurer in the state) decided to issue a press release patting themselves on the back for keeping their small business average rate hike down to 2.9%:

DETROIT, June 8, 2016 /PRNewswire-USNewswire/ -- In contrast to national trends, Blue Cross Blue Shield of Michigan today announced a comparatively small statewide average rate increase of 2.9 percent for small group employers in 2017, pending state regulatory approval. This follows rate reductions that Blue Cross delivered to small employer group customers that renewed during the second half of 2015.

Interesting. When I last checked in on the Maryland exchange, their effectuated QHP enrollment was down about 14% since the end of open enrollment (from 162,177 QHP selections to 139,379 effectuated enrllees as of the end of April).

However, they just posted the following market share breakdown, which shows that they currently have 148,403 Marylanders enrolled in exchange policies, a net drop of just 8.5%. Apparently they've added more people during the off season via SEPs than they've lost due to attrition since April.

Back in April, I attempted to figure out just how many people are still enrolled in Grandathered and/or Transitional (or "Grandmothered") policies on the individual market. My conclusion, based on some very rough estimates, was that the figure is likely somewhere between 800K - 1.4 million Grandfathered enrollees and somewhere between 1.1 - 1.5 million Transitional enrollees.

Today, I decided to try tackling the Transitional side of this problem by taking the direct approach: I visited RateReview.Healthcare.Gov.

Most of my time spent here over the past few weeks has been spent on the "Search ACA-Compliant Products" side, trying to lock down the requested 2017 rate hikes for every carrier offering individual policies in every state. However, there's a second big button available as well: "Search Transitional Products":

I receive most of the HHS/CMS press releases, but this one seems to have slipped by me (furiously checking spam filter...). Fortunately, Bob Herman of Modern Healthcare spilled the beans via Twitter this morning (emphasis mine):

Today, the Department of Labor, Department of Treasury, and Department of Health and Human Services (HHS) issued a proposed rule to revise the definition of short-term, limited duration coverage. Under the new rules, short-term policies may be offered only for less than three months, and coverage cannot be renewed at the end of the three month period. The proposed rule also improves transparency for consumers by requiring issuers to provide notice to consumers that the coverage is not minimum essential coverage, does not satisfy the health coverage requirement of the ACA, and will not prevent the consumer from owing a tax penalty. The proposed changes will help strengthen the risk pool by ensuring that short term limited duration plans are used only as intended, to fill truly temporary gaps in coverage.

First, let's hear it for the Oxford Comma, everyone!!

Ever since my infamous clash with Avik Roy over the "how many exchange enrollees are newly insured?" brouhaha over two years ago, one issue which has always been kind of fuzzy has been the question of exactly how many OFF-exchange individual healthcare policy enrollees there are. Since most carriers don't like to break out their enrollment numbers in too much detail for competitive/trade secret reasons, and many states don't require them to do so, this makes tracking the off-exchange numbers pretty difficult.

Just yesterday I posted the Washington Healthplanfinder's latest monthly report, which showed either 177,613, 170,267 or 167,827 people currently enrolled in exchange QHPs statewide, depending on whether you go by the number who have "selected plans", the number that the carriers have reported as being paid up or the number who the exchange has recorded as having paid.

The first number has been pretty confusing to me over the past few months, because the actual number of people who selected QHPs during the 2016 open enrollment period was reported as just over 200,000 by both the exchange itself as well as in the official national ASPE report, so I wasn't quite sure whether to report the net effectuated enrollment drop since then as being almost none at all or around 15%. I finally went with the 15% figure because dividing into the 177K number just didn't make sense by any other measure.

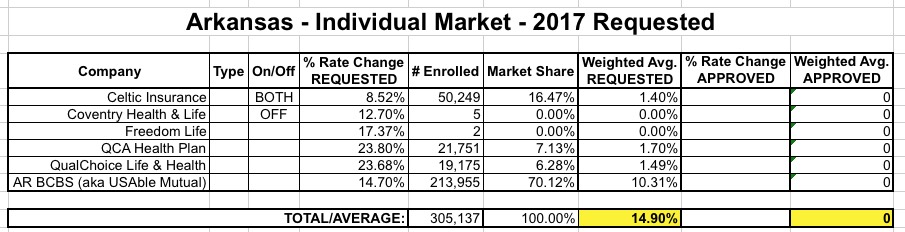

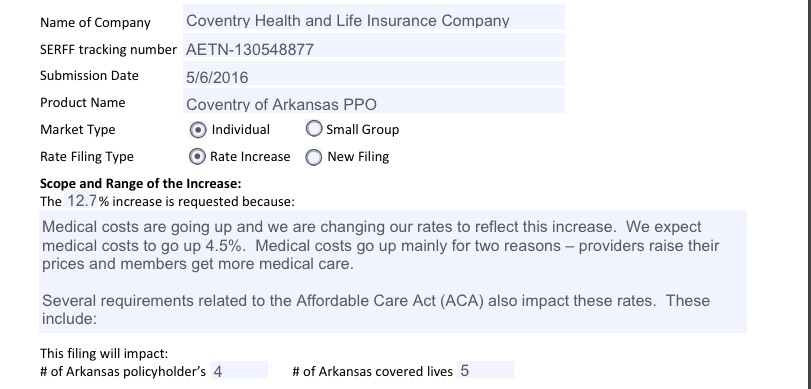

So just last Friday I posted the weighted average requested rate hikes for the Arkansas individual market; it came in at 14.9% overall, which is actually one of the lower statewide averages this year. As a reminder, here's what how the breakout looks:

OK, so 3 major carriers asking to jack up rates 15-24%, plus one at 8.5% and two others with just 7 enrollees between them (one of which is, once again, Freedom Life Insurance). So what?

As regular readers know, I'm currently in the thick of my state-by-state analysis of the requested, weighted average rate changes for 2017 by insurance carriers for the entire ACA-compliant individual market. As of this writing, the overall average looks like it's just a hair over 20% across 28 states + DC.

Does the first sentence above include a lot of clarifiers? Yes, yes it does...and with good reason. I try to be very specific when I discuss this stuff, because it's very easy to get confused about what a given number is actually referring to.

For instance, a few days ago, Avalere Health released their own analysis which concludes that the average requested/proposed premium rates are around 12%. If I left it at that, you might think that either my average is 8 percentage points too high...or that Avalere's is 8 points too low.

Thanks to commenter "Junaed S" who directed me towards this simple, cut 'n dry PDF from the Connecticut Dept. of Insurance detailing the requested rate hikes for the CT individual and small group markets for 2017:

In addition, Anthem has decided not to offer its PPO (Preferred Provider Organization) individual plans in 2017. In all, the Colorado Division of Insurance said Monday around 92,000 people with individual plans from Anthem, UnitedHealth, Humana, and Rocky Mountain Health Plans will have to find other coverage during open enrollment in the fall.

Last month I noted that the Washington Healthplanfinder was reportingcurrently effectuated QHP enrollment at 170,527 as of the end of March, a 15.0% drop from the official number of QHP selections during the 2016 Open Enrollment Period. I also noted that due to some confusion about how the numbers are reported by the exchange, it could also be argued that WA has seen just a 6.6% net drop, depending on how you look at it.

However, since 200,691 is the official number included in the ASPE report, I'm finally letting that one go...and actually, that's OK, because a 15% drop by 3/31 is fairly close to what I would expect anyway (a bit higher than the 13% national drop from last year, but not out of line).

Anyway, the WA exchange just released their May report (with data through the end of April), and it's actually pretty good--there's only been a very slight net drop since March, for an overall drop of just 15.2% from the 200K figure:

A simmering dispute over the risk corridor program has broken into the presidential campaign, with Senator Rubio crowing that an arcane budget move has “kill[ed] Obamacare” and “saved the American taxpayer $2.5 billion.” On account of that move, health plans are set to receive only pennies on the dollar from the risk corridor program, which was supposed to cushion them from big losses.

...The administration has vaguely said that it will “use other sources of funding for the risk corridors payments, subject to the availability of appropriations.” But the budget bill limits the administration’s power to dip into other funds, and a Republican-controlled Congress isn’t likely to appropriate money for a program that’s been decried as an insurer bailout.

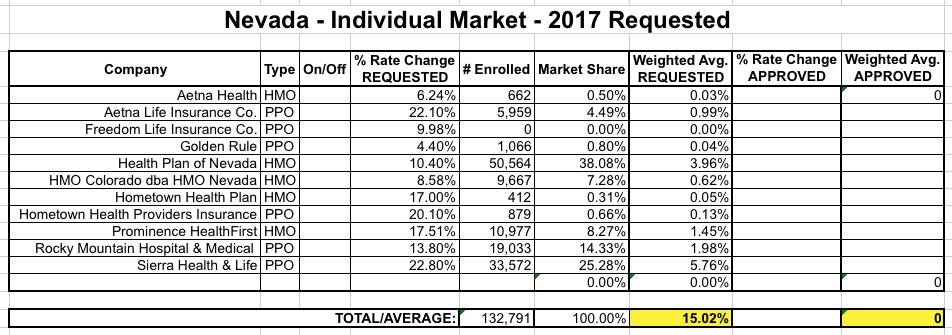

Can I first say that I absolutely love the way Nevada's rate filing database is set up, especially their (apparently proprietary and mandatory) filing format system?

Unlike the standard SERFF database, which is comprehensive but also can be confusing as hell, Nevada's system is simple, clean, easy to navigate and, most of all, every single carrier filing listed displays the number of current enrollees clearly.This is a huge pet peeve of mine, which is understandable given what I'm trying to do here!

OK, that said, here's what things look like in the Silver State:

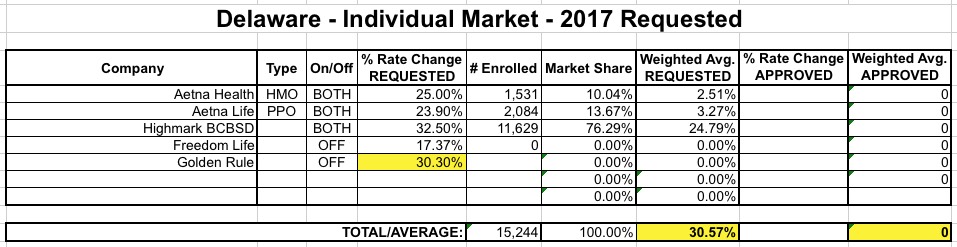

Delaware is a small state, and only has a total of 4 carriers offering individual polcies (2 on exchange, 2 off). One of those, however, is once again "Freedom Life" which, once again, is asking for precisely a 17.37% rate hike on their almost-certain-to-be-nonexistent enrollees. So...never mind them. That leaves Aetna (split into HMOs and PPOs) and Highmark BCBS offering policies on the exchange, and Golden Rule off the exchange.

Unfortunately, I can't find Golden Rule's actual current enrollment number, but as you can see below, it really doesn't matter:

As you can see, no matter how many enrollees Golden Rule has, their 30.3% average hike request is very close to the 30.6% average of the other carriers. The very most it could do is nudge the weighted average down by a tenth of a point or two, so let's call it 30.5%.

On Wednesday I noted that a whopping 175,000 Louisianans had somehow managed to enroll in the state's just-launched Medicaid expansion program within less than 12 hours of the floodgates being opened up. This was even more amazing when you consider that number represents 47% of the total people estimated to be eligible for the program state-wide (375K).

Now, obviously there's no way that 16,000 people per hour were individually visiting HealthCare.Gov or their local state health agency; on it's busiest day (December 15, 2015), HealthCare.Gov was averaging 25K/hour...but that was across 38 states, many of which are much larger than Louisiana. Instead, I assumed that LA had done something similar to Oregon/West Virginia's "fast-track" programs, where they use existing food stamp/welfare databases to automatically enroll people, not "officially" pulling the trigger until after the stroke of midnight.

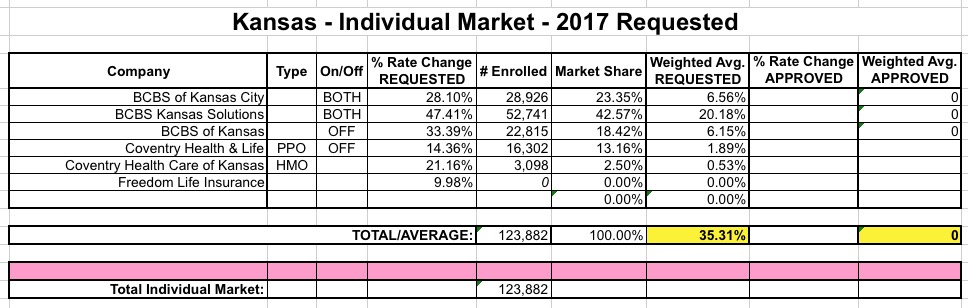

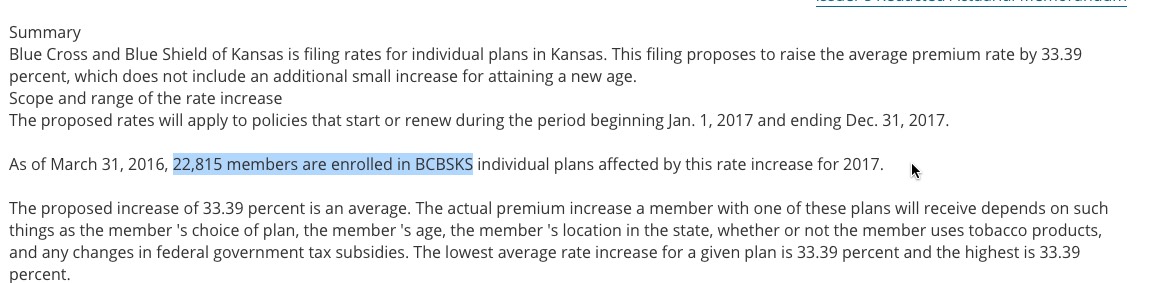

The good news about Kansas is that 5 of the 6 carriers which have submitted 2017 individual market rate filings included their current enrollment totals in a clear, easy to see format...and the 6th one is (once again) "Freedom Life" which, judging by the dozen other states they've popped up in, almost certainly has only 1 or 2 enrollees (or none at all) anyway.

The bad news is...well, the requested rate hikes are pretty ugly: About 35.3% on weighted average.

Also, is it really necessary for Blue Cross Blue Shield to operate under three nearly-identical names? Really?

Arkansas was a little weird...while the rate filings for 5 carriers are listed over at RateReview.HealthCare.Gov, the carrier with the largest individual market share in the state, BCBS (aka "USAble Mutual") is nowhere to be seen (there's a sm. group listing for them, but not individual). However, when I went directly to the AR SERFF database, there they were--and it's listed specifically as "2017 Individual QHP Rates", so there's no question here about whether they plan on offering ACA-compliant policies in 2017.

Anyway, between the HC.gov site and the SERFF site I was able to cobble together pretty much all of Arkansas' indy market. The numbers seem about right; AR's indy market was around 303K in 2014; while it's likely up to 375K or so today, the "missing" 70K can easily be attributed to UnitedHealthcare dropping out and/or grandfathered/transitional enrollees.

At 14.9% on average, this is actually good news for 2017, relatively speaking.

Oklahoma's entire individual market (including grandfathered/transitional plans) was around 172,000 people in 2014. Assuming it's grown roughly 25% (in line with the national increase), it should be up to perhaps 215,000 people by today, of which perhaps 195K are ACA-compliant.

This is significant because there appear to be only 3 carriers offering individual policies in Oklahoma next year...one of which is the infamous "Freedom Life Insurance Co." which I wrote about last night. Since Freedom Life has (as usual) only a single enrollee in the state, it's really a nonfactor for calculating the weighted rate hike average.

That leaves Blue Cross Blue Shield of Oklahoma, which has a whopping 170,000 enrollees...and CommunityCare (which is in turn broken into HMO and PPO divisions)...unfortunately, their rate filing doesn't include their enrollment number; all it says is that it's "too small to be credible" to be used as the basis of their rate hike request. In addition, UnitedHealthcare is dropping out of the OK indy market; I don't know how many enrollees they actually have.

About 800,000 people nationally lost their insurance coverage, on very short notice, and were forced to scramble to find alternate coverage

The new coverage they ended up with was generally more expensive, and in many cases has worse networks

The federal government has to pay out more in premium subsidies to cover the increased costs as benchmark plans were increased

Over a dozen insurance carriers went out of business, meaning hundreds of people lost their jobs

Less competition in those markets, therefore higher premiums, therefore even more cost to the federal government in subsidies to make up the difference

Since all of the carriers which went out of business were little guys, this also means the big kahunas suck up even more market share

The original $2.5 billion which Rubio was supposedly trying to "save" taxpayers ends up being paid out anyway; and

Assuming the government decides to just concede the point (which, by all rights, they should), it's conceivable that Marco Rubio's "genius" stunt from December 2014could also very well end up costing taxpayers $2.5 billion MORE than it would have to just let the government make the payments they were supposed to in the first place.

...all of this just so that Marco Rubio could earn a couple of political brownie points to help him win the GOP nomination for President...which he ended up failing at miserably.

Throughout the summers of 2015 and 2016, the news media was chock-full of apocalyptic headlines screaming about MASSIVE DOUBLE DIGIT OBAMACARE RATE HIKES!!!, suggesting that rate hikes of 20%, 30% even 50% would be not just widespread but the norm nationally.

The reality, as I repeatedly tried to get through people's heads, is that while some carriers in some states were trying to push through massive hikes on some plans, the overall picture was far less dramatic. Many were seeking increases of under 10%, while some (not many, I admit) were even reducing rates. When you averaged out the rate changes by state and then weighted them by the number of people actually enrolled in those policies, it came in at around 7-8% in 2015 and around 12-13% in 2016.

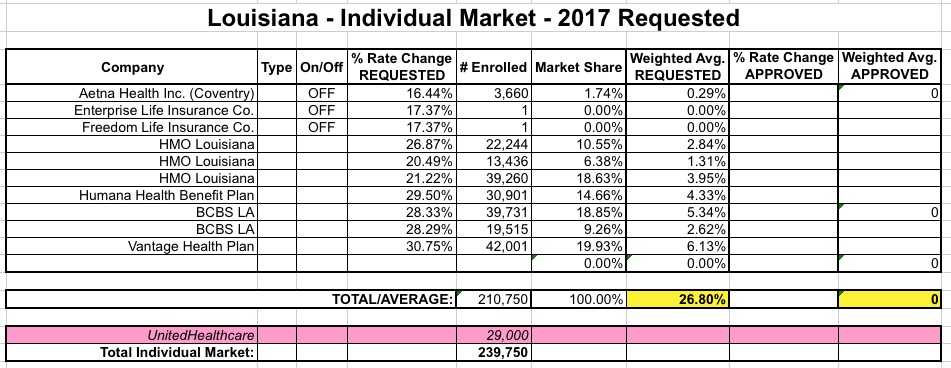

This year, about 214,000 people selected QHPs via HealthCare.Gov in Louisiana, though this has likely dropped to around 182K by now. The state's total individual market (on+off exchange, as well as grandfathered/transitional policies) was around 225,000 in 2014, and has likely increased roughly 25% since then to perhaps 280,000 total, of which around 10% is likely comprised of grandfathered/transitional enrollees. That should leave roughly 250,000 ACA-compliant enrollees statewide.

With this in mind, here's how things stack up in Louisiana for the ACA-compliant individual risk pool rate hike requests:

A few weeks ago I noted that thanks to the election of Democratic Governor John Bel Edwards (with an assist by David Vitter's diaper fetish), up to 375,000 lower-income Louisiana residents became eligible for the ACA's Medicaid expansion provision starting a month earlier than expected (June 1st instead of July 1st).

Enrollment officially started early this morning (not sure if it was right at midnight or if they had to wait until the state offices opened or whatever), and as of around 11:40am...

Gov. Edwards announces that there are already 175,000 Louisianans enrolled in the expanded Medicaid program. #lagov#lalege

— Gov John Bel Edwards (@LouisianaGov) June 1, 2016

Hmmm...last year Nebraska had 5 carriers offering individual policies, 2 of which were actually divisions of the same company (UnitedHealthcare). Since United is pulling out of Nebraska, this leaves only three companies...one of which is the mysterious "Freedom Life Insurance Co." which keeps popping up in numerous states as not having a single actual enrollee, and almost always asking for the exact same rate hike: 17.37%. What's up with that?

Anyway, Coventry (actually Aetna) appears to also be gone next year as well...or perhaps they simply haven't submitted their rate filings yet? I suspect the latter because Nebraska's total individual market was over 110,000 people as of 2014, and is likely up to over 130K this year (nearly 88,000 enrolled via the ACA exchange alone this year)...yet adding up the numbers from the official filings only totals around 30,000 people.

Back in mid-April, I posted the UnitedHealthcare State Dropout Odometer, which tracked exactly which of the 34 states which UnitedHealthcare is currently offering individual market policies in this year they'd drop out of for 2017. Instead of simply stating "we're sticking around in these states and dropping out of the rest", United decided to dole the pain out gradually, with states announcing their departure one by one over several weeks. For quite awhile, I knew that they were sticking around Nevada, New York and Virginia, with another half-dozen states in limbo status.

Today, according to the Chicago Tribune and the Minnesota Star Tribune, it looks like those three are it: They'll still be available in those 3 states, but are pulling out of the other 31 (including California, where they only have around 1,200 current enrollees via the exchange anyway). OK, that sucks, but we kind of knew about this already; it's old news for the most part.

North Carolina's individual market, which only had 5 carriers participating to begin with this year, suffered a double blow recently when both UnitedHealthcare (155,000 enrollees) and Humana (3,272 enrollees) announced that they were dropping out of the market entirely next year (Celtic is also leaving the state, but they have literally just 1 person enrolled state-wide anyway). Fortunately, nature abhors a vacuum, so Cigna Health & Life Insurance decided to join the exchange for 2017. Cigna is already selling off-exchange individual policies, but only has fewer than 1,300 people enrolled in them at the moment. There's also a carrier called "National Foundation Life Insurance" which is raising rates 17.4%...but doesn't have a single person enrolled at the moment anyway, so I'm not sure what to make of that.

It's time to take a breather from my ongoing 2017 Rate Hike Request project to check in on a couple of off-season enrollment numbers. First up is Minnesota. Here's how the QHP tally (cumulative, not currently effectuated) has gone since open enrollment ended in the Land of 10,000 Lakes (note: Michigan actually has 11,000, so there!):

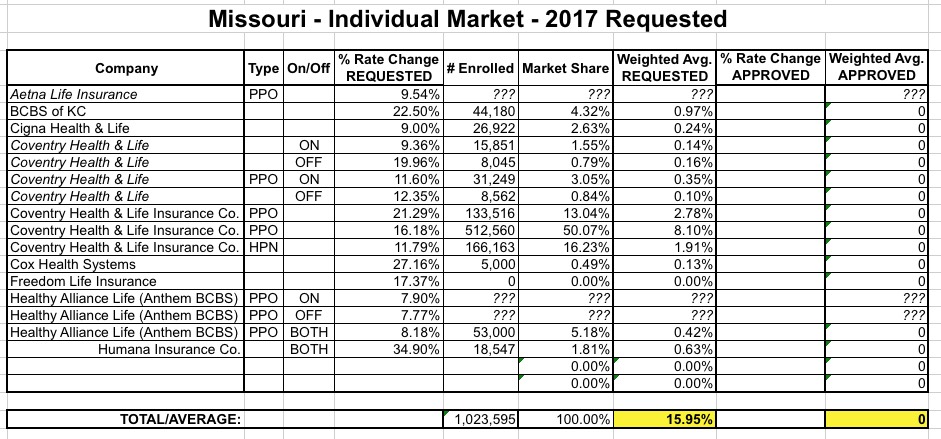

OK, there's something very odd going on with Missouri's 2017 rate filings for the individual market. According to the Kaiser Family Foundation, Missouri's entire individual market was around 344,000 people in 2014. While it's likely increased by around 25% since then, that would still only bring it up to around 430,000 people including both grandfathered and transitional enrollees, which sounds about right to me (290,000 enrolled via the ACA exchange, which would leave around 140,000 off-exchange).

And yet, when I plug in the official rate filings for Missouri's individual market for 2017, here's what it looks like: