IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

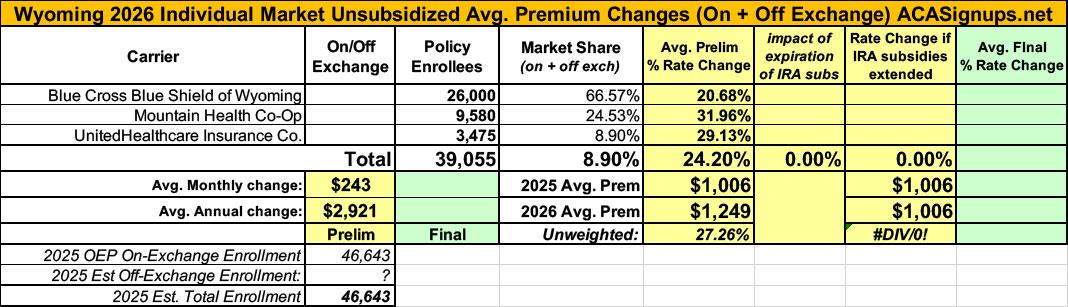

Wyoming has ~46,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most). Combined, that's around 8% of their total population.

(Note, however, that the official actuarial rate filings for the 3 carriers offering coverage in the Wyoming individual market only report a combined total of around 39,000 enrollees as of spring 2025, or 6.6% of the total population).

Blue Cross Blue Shield of Wyoming (BCBSWY) has offered comprehensive and fully insured coverage to members in the Individual ACA market since 2014. BCBSWY is filing a rate increase for 2026 products. All plans will be offered statewide; plans with be offered either on or off the Federally Facilitated Marketplace in Wyoming.

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

It was just a couple of weeks ago that the official (if preliminary) 2026 ACA individual market rate filings for Wyoming insurance carriers went live on the federal rate review website.

I published a writeup about these just 3 days ago; unlike some states, Wyoming was pretty easy to break out as they only have three carriers on the indy market, all of which also made their current enrollment data easy to find.

The landscape isn't pretty: BCBS is seeking average rate increases of 20.7%; UHC wants 29.1%, and Mountain Health Co-Op, which has around 9,600 enrollees, was asking for a whopping 32% average premium hike.

Keep in mind that Wyoming already has among the most expensive individual market policies in the country, with premiums averaging over $1,000/month.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

The bad news for Wyoming residents who earn too much to qualify for any federal ACA subsidies is that the state has the second highest unsubsidized premiums in the country after West Virginia. The good news is that, thanks to the Inflation Reduction Act, there are far more residents who do qualify for federal subsidies, which chop those premiums down to no more than 8.5% of their income....at least until the end of 2025, at which point the upgraded IRA subsidies are currently scheduled to expire.

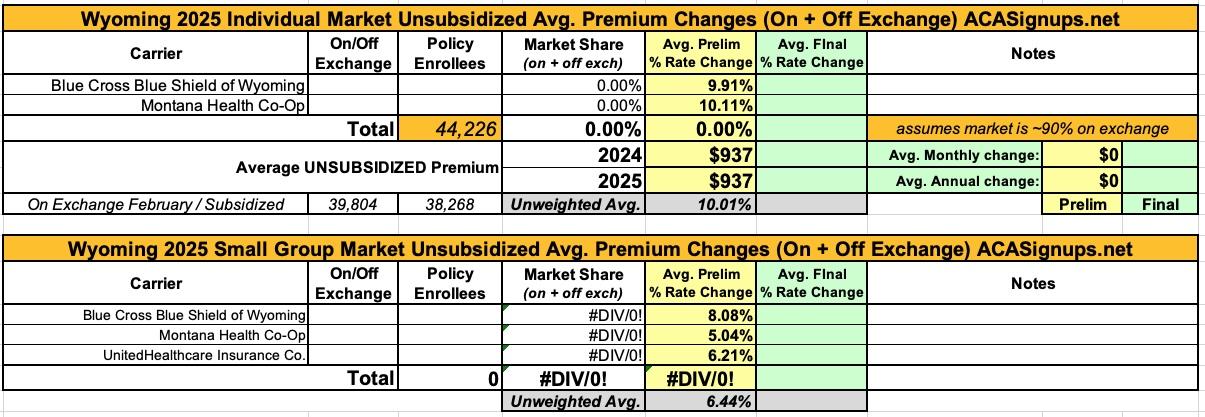

Unfortunately, once again, I've been unable to get ahold of enrollment data for any of Wyoming's carriers on either the individual or small group markets, so I can only run unweighted averages for both markets.

With that said, the unweighted average rate hikes being asked for are 10% on the indy market and 6.4% for small group plans.

Wyomingites may be skeptical of Obamacare, but many use it for health insurance

(sigh)

Wyoming leaders have repeatedly rejected Medicaid expansion, but a new study shows many residents here rely on another component of the Affordable Care Act: the health insurance marketplace.

Among 10 states with the highest share of farmers, Wyoming uses the federal health insurance marketplace the most, according to a new analysis by the Robert Wood Johnson Foundation. That marketplace is a virtual space for comparing plans and finding insurance that’s often more affordable than elsewhere thanks to federal subsidies.

The bad news for Wyoming residents who earn too much to qualify for any federal ACA subsidies is that the state has the second highest unsubsidized premiums in the country after West Virginia. The good news is that, thanks to the Inflation Reduction Act, there are far more residents who do qualify for federal subsidies, which chop those premiums down to no more than 8.5% of their income.

The other good news for them is that for 2024, average premiums across the two insurance carriers which participate on the ACA exchange pretty much cancel each other out, with Blue Cross Blue Shield of Wyoming dropping their average premiums by 7% even as the Montana Health Co-Op seeks to raise theirs by 7.6%. Unfortunately, once again, I've been unable to get ahold of enrollment data for each carrier so this is an unweighted average only; if, say, 90% of enrollees are in Montana Co-Op plans, the weighted average would obviously be more like a 6% increase or whatever.