IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

I've written multiple times in the past about "Silver Loading," the ACA health insurance policy pricing strategy in which insurance carriers load the extra cost of their Cost Sharing Reduction financial burden (the portion of deductibles, co-pays & coinsurance which they're required to cover themselves for low-income enrollees who select Silver plans) onto the gross premium of those same Silver plans.

It gets a bit wonky, but the bottom line is that Silver Loading results in the gross price of Silver ACA plans increasing significantly even if the price of Bronze, Gold & Platinum plans only go up modestly. This may sound bad, but stay with me.

From the carriers perspective, how the CSR load is allocated doesn't matter much as long as they aren't left stuck with the bill...but pricing the plans in this fashion has major implications for the enrollees themselves.

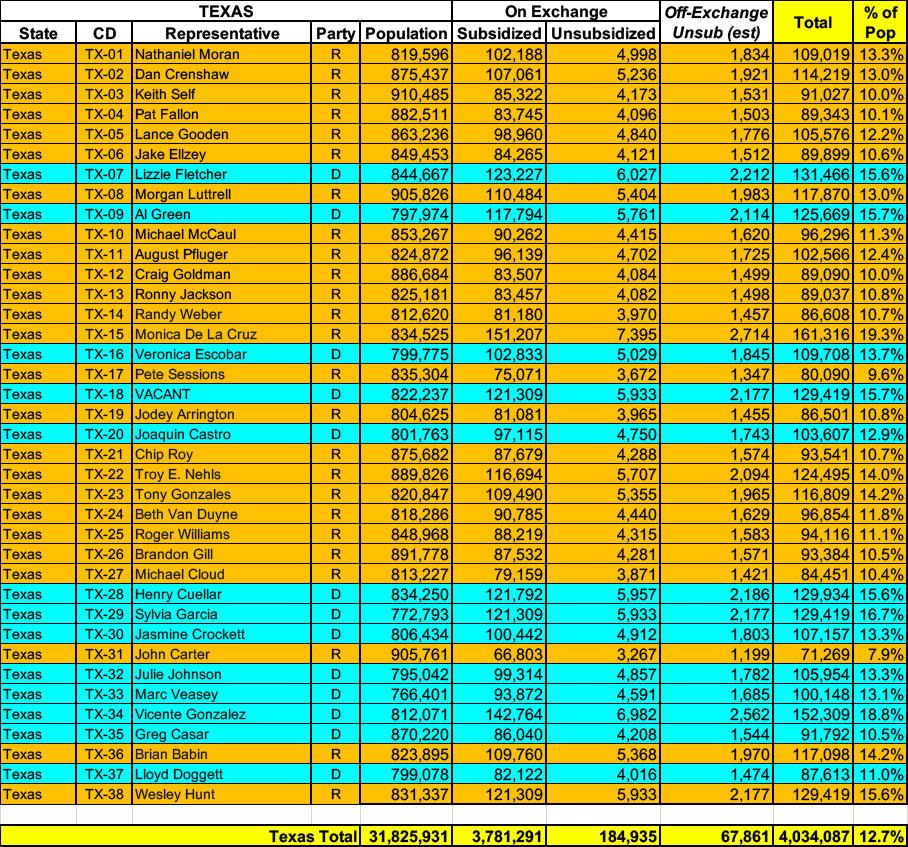

Texas has ~3.9 MILLION residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have perhaps ~67,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.0 MILLION Texans, although although assuming the national average 6.6% net enrollment attrition rate applies, current enrollment would be back down to more like ~3.8 million statewide.

(Access to Care Health Plan is a division of Sendero; unfortunately, they've heavily redacted their actuarial memo and I can't find a justification summary)

Aetna Health:

Aetna is dropping out of the individual market nationally in 2026. In texas, they've provided a market withdrawl letter which includes the exact number of current enrollees in each region of the state:

"Aetna is totally withdrawing from the individual (off and on-exchange) market, effective December 31, 2025. Individuals currently covered under an Aetna plan will need to make a different plan selection for 2026. In accordance with Texas and federal law, consumers will be given 180 days’ notice of the termination of their policy."

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

The Supreme Court seemed likely to uphold a key preventive-care provision of the Affordable Care Act in a case heard Monday.

Conservative justices Brett Kavanaugh and Amy Coney Barrett, along with the court’s three liberals, appeared skeptical of arguments that Obamacare’s process for deciding which services must be fully covered by private insurance is unconstitutional.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

The Supreme Court seemed likely to uphold a key preventive-care provision of the Affordable Care Act in a case heard Monday.

Conservative justices Brett Kavanaugh and Amy Coney Barrett, along with the court’s three liberals, appeared skeptical of arguments that Obamacare’s process for deciding which services must be fully covered by private insurance is unconstitutional.