So far, after a 2-month initial delay, the Musk/Trump Regime has been posting updated Medicare enrollment data roughly once per month. We'll see if that continues.

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of February 2025:

Over the past month or so, as Congressional Republicans have pulled out all the stops in their attempt to ram through their budget bill which would gut Medicaid and ACA exchange enrollment (along with SNAP and numerous other desperately-needed social aid programs), you may have noticed that they keep using an oddly specific talking point:

Mike Johnson: Medicaid Is Not for 29-Year-Old Males Sitting on Their Couches Playing Video Games

Mike Johnson on Medicaid: "What we've talked about is returning work requirements ... you return the dignity of work to young men who need to be out working instead of playing video games all day. We have a lot of fraud, waste, and abuse in Medicaid."

Welp. House Republicans did indeed follow through with passing their horrific (and disgustingly-titled) "One Big Beautiful Bill" Act which will effectively repeal the bulk of the ACA without officially repealing it, and that's just for starters.

The final vote was 215 - 214, with every Republican except a handful voting for it (and the two who voted against it openly admitted to the NY Times that they would have voted for it if their votes had been needed), and every Democrat voting against it. There were 2 Republican "no" votes...but both of those were only because they wanted the final bill to be even more draconian.

There's so many awful things included in the bill, many of which are of course healthcare-related, and it would take hundreds of blog entries to discuss them all...but I want to focus on one in particular.

I joined Jennifer Taub on her podcast to discuss the House GOP budget bill (aka the #MAGAMassacreBill) and the Trump Regime's all-out assault on the U.S. healthcare system.

For over a decade, State-Based Marketplaces have provided private health coverage to tens of millions of Americans, ensuring their health, well-being, and economic security. The Americans who depend on the Marketplaces include working parents, small business owners, farmers, gig workers, early retirees, and lower and middle-class individuals of all ages, political views, and backgrounds who drive our local economies and make both our rural and urban communities thrive.

The legislation under consideration in the House will severely impact the ability of these millions of Americans to continue to access this coverage and the health and financial security they depend on today. This will make for a sicker, less financially secure American public and strain hospitals and health care providers by increasing uncompensated care.

Advocating for Massachusetts residents and maintaining access to affordable coverage for everyone, the Massachusetts Health Connector on Friday submitted a comment letter to a proposed federal rule from the Centers for Medicare and Medicaid Services.

The letter focuses on proposals in the federal rule that would impact eligibility and enrollment functions for the Health Connector as well as policies in the larger insurance market. Massachusetts leads the nation in coverage rate, with more than 98 percent of residents covered according to the U.S. Census, and provisions in the rule would make it more difficult for residents to get and maintain coverage, while making coverage more expensive.

Congress Urged to Renew Expiring Enhanced Premium Tax Credits and Prevent Unnecessary Increases in Health Care Costs for New Jersey Residents

Over 450,000 Get Covered New Jersey enrollees would be impacted by loss of expanded financial help

New Jerseyans could lose more than half a billion dollars in federal support and face higher health insurance costs

TRENTON — Warning about significant health insurance premium increases for over 450,000 New Jerseyans, New Jersey Department of Banking and Insurance Commissioner Justin Zimmerman sent a letter to New Jersey’s Congressional delegation strongly urging them to extend the expiring federal enhanced premium tax credits that have enabled hundreds of thousands of New Jersey residents to enroll in quality, affordable health insurance through Get Covered New Jersey, the State’s Official Health Insurance Marketplace.

Rep. Boyle: The one thing I would point out, though, is this bill is actually significantly worse [than the GOP's ACA repeal attempt in 2017], because this piece of legislation will throw 13.5 million, almost 14 million Americans off their healthcare.

First, you're cutting people off Medicaid. But second, this does include very deep cuts to Obamacare as well. And finally, I have breaking news for you tonight, that literally just came out in the last few minutes as I've been sitting here: The nonpartisan Congressional Budget Office, the official authority on these figures, has now confirmed that this bill, in addition to Medicaid cuts, in addition to Obamacare cuts, includes $500 BILLION WORTH OF CUTS TO MEDICARE that is now in this bill as well.

With potential Federal cuts to Medicaid on the horizon, renewing enhanced premium tax credits to ensure affordable insurance through the marketplace takes on greater significance

AUGUSTA— The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) today announced its support for renewing the enhanced premium tax credits for consumers of the health insurance marketplace.

The enhanced premium tax credits, which were first implemented in 2021 through the American Rescue Act and extended in the Inflation Reduction Act are set to expire at the end of this year unless Congress acts. Allowing these federal tax credits to expire will result in higher health insurance premiums for Maine consumers, potentially putting health coverage out of reach for thousands of Mainers. Overall, the enhanced tax credits are saving Mainers a conservative estimate of nearly $90 million in health care premium savings this year.

Covered California expresses deep concern regarding the proposed health provisions in the reconciliation bill moving through the House of Representatives.

If enacted, the legislation would have devastating consequences to the health, well-being and financial security of hundreds of thousands of Californians who would lose access to affordable health insurance. It would also lead to greater strain on the health care system and increased costs for individuals and businesses throughout the state.

Estimated Nearly $13.5 Billion Loss Annually For New Yorkers and Our Healthcare Economy

Nearly 1.5 Million New Yorkers Could Lose Essential Plan or Medicaid Coverage And Become Uninsured

Governor Hochul Demands Republican Members of Congress Oppose These Cuts and Protect Their Constituents

Governor Kathy Hochul today updated New Yorkers on the harmful effects of several healthcare provisions already passed from the House Ways & Means and Energy & Commerce committees for the Republican budget reconciliation bill. These provisions collectively amount to an annual loss of nearly $13.5 billion for New Yorkers and our healthcare sector, jeopardizing healthcare access for millions of New Yorkers while imperiling the state’s hospitals and other healthcare providers.

So, the Congressional Budget Office has published updated estimates of the budgetary impact of the House Republican budget plan (officially called the "One Big Beautiful BIll Act" (seriously); more appropriately called the #MedicaidMassacre bill by certain individuals (ahem) were to pass & be implemented.

In addition to all the dollar amounts tossed around, however, the spreadsheet also includes some important footnotes, including the following (h/t Larry Levitt of KFF for the heads up):

Under the Title IV - Energy & Commerce tab is this:

With the House Republican budget bill having made it past its second significant hurdle last night (the House Budget Committee vote), it's time tot ake a cold, hard look at just what the impact of the bill will be in pure partisan terms.

The logic Congressional Republicans (or at least Donald Trump, who pretty much has complete control over the Congressional Republican hivemind) seem to be going with is that targeting the Medicaid expansion population is good politics for them because:

UPDATED 5/22/25: Welp. House Republicans did indeed follow through with passing their horrific (and disgustingly-titled) "One Big Beautiful Bill" Act which will effectively repeal the bulk of the ACA without officially repealing it, and that's just for starters.

The final vote was 215 - 214, with every Republican except a handful voting for it (and the two who voted against it openly admitted to the NY Times that they would have voted for it if their votes had been needed), and every Democrat voting against it. There were 2 Republican "no" votes...but both of those were only because they wanted the final bill to be even more draconian.

I joined Susan J. Demas of Lincoln Square to discuss the House GOP budget bill (aka the #MAGAMassacreBill) and the Trump Regime's all-out assault on the U.S. healthcare system.

Last week I wrote about the latest state of play regarding House Republicans so-called "big beautiful bill" to gut Medicaid in order to give fat tax cuts to billionaires. Yesterday the first official version of the legislative text was released, and it's pretty much as ugly as you might expect.

...The plan caters more to the moderate wing of the Republican party by omitting two of the biggest and most politically controversial proposals discussed: a per-capita cap on people who get coverage from Medicaid expansion, and a direct lowering of the federal matching rate.

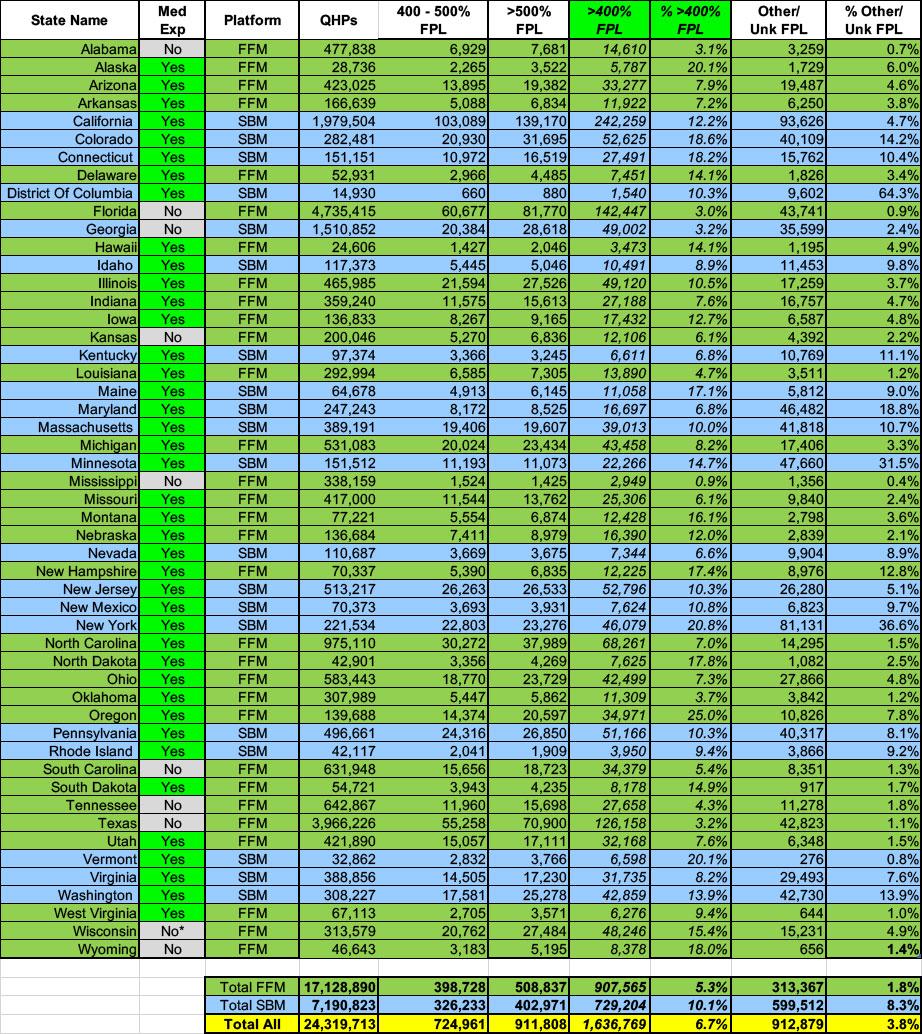

Finally, there's over 1.6 million exchange enrollees who earn more than 400% FPL.

While enrollees in every other income bracket will be hit hard by IRA subsidies expiring, and many of them would be seriously damaged by Silver Loading being phased out, in terms of hard dollars, it's the middle-class enrollees being kicked back off the "Subsidy Cliff" again who will see the most jaw-dropping premium hikes.

Not only would they lose eligibility to any federal financial assistance, they'd also be hit with 6 full years of medical inflation (remember, the original ARPA/IRA subsidies have been in place (retroactively in some cases) since January 2021).

It's not gonna be pretty.

Finally, there's over 900,000 enrollees whose household income is simply unknown.

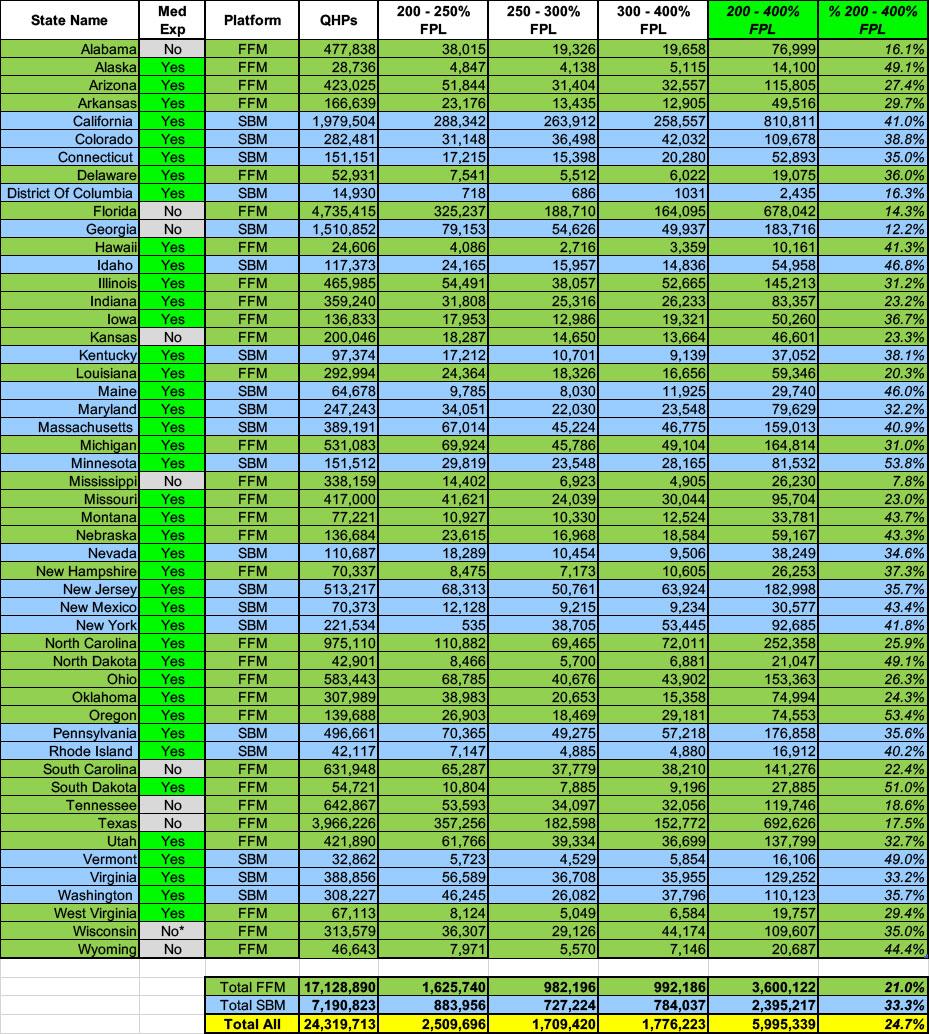

Next, let's look at the 200-400% FPL brackets. These make up almost exactly 1/4th (24.7%) of total ACA exchange enrollment this year.

These ~6 million enrollees are the ones who will be hit with a double whammy if both the IRA subsidies and Silver Loading end next year: Not only will they be hit with skyrocketing monthly premiums due to dramatically less-generous APTC subsidies, but they'll be far less likely to be able to use what subsidies they do receive to enroll in lower-deductible Gold plans (which cover ~80% of average claims) vs. Silver plans (which only cover 70-73% of average claims, depending on whether they include CSR help or not).

Turning to the 100 - 200% FPL range (and ignoring Medicaid expansion), 63% of all exchange enrollees fall into this income range (up from 61% last year).

That's over 15.2 million people total, and with extremely rare exceptions, just about every one of them should be enrolled in a Silver CSR plan, aka "Secret Platinum", since the extremely generous Cost Sharing Reduction (CSR) assistance in the 100 - 200% FPL range turns Silver plans (which normally have a ~70% Actuarial Value) into either an 87% or 94% AV plan...effectively Platinum (90% AV)).

In layman's terms, High CSR Silver plans have either free or extremely low premiums along with extremely low deductibles & co-pays.

This is, of course, extremely important since household income is one of the most critical factors in calculating how much financial assistance enrollees receive (or if they're eligible for Advance Premium Tax Credits (ATPC) at all).

Since there's so many income bracket columns and there's a lot to delve into for many of them, I've broken the full spreadsheet out into three sections/posts. The first focuses on exchange enrollees who earn less than 138% of the Federal Poverty Level (FPL). This is a critical threshold because it's the cut-off point for ACA Medicaid expansion enrollment in the 40 states (+DC) which have expanded it.

Nationally, over 31% of all exchange enrollees earn less than 138% FPL, which may sound surprising given that 41 states have expanded Medicaid...until you realize which states haven't done so yet: Over 4.5 MILLION enrollees in Florida and Texas alone earn less than 138% FPL (2.4 million & 2.1 million respectively).

If you've ever wondered why healthcare wonks (myself included) almost never even bring up the ACA's Catastrophic Level plans and why the only time I ever discuss Platinum Plans is in the context of high-CSR enrollees being eligible for "Secret Platinum" plans (labeled as Silver), this table should explain why.

Catastrophic ACA plans aren't available at all 10 states, and only 0.24% of enrollees choose Catastrophic plans in the other 40 states (+DC)...just 54,000 nationally (which is also down several thousand y/y). Of the states that even offer them, Catastrophic plans don't reach higher than 2.4% of the ACA exchange market, and that's only in DC and Minnesota...just 4,000 people in both.

At the opposite end, Platinum plans are only available in 19 states (+DC)...and again, just 0.5% of all exchange enrollees choose Platinum plans (even in those 20 states it's only 1.0%). This ranges from virtually none in TN, WV & IN to 15.7% in Hawaii.

Next up: Age brackets, gender, racial/ethnic groups and urban/rural communities. I'm also throwing in the stand-alone Dental Plan table here for the heck of it since I don't know where else to include it.

I don't have a ton to say about any of these, really. 10.6% of ACA exchange enrollees are children; 38.2% are under 35. It's also always interesting to me to see that 1.7% of ACA exchange enrollees are 65 or older.

Alabama has the lowest percent of enrollees under 18 (3.6%), while Utah has the highest (27.8%) which I guess makes sense since Utah has the youngest median-aged population in the country. Similarly, Utah has the highest percent of enrollees under 35 (58.6%) vs. Hawaii's 26.2% (lowest).

Next up: Premiums, Advance Premium Tax Credits (APTC) and Cost Sharing Reduction (CSR) assistance.

Nationally, the average unsubsidized premiums for 2025 exchange-based Open Enrollment Period enrollees is $619/month, up $14 or just 2.3% from $605 last year.

This is a noteworthy because 2025 ACA exchange premiums "should" have increase by more like 6-7% on average. This discrepancy is mostly because that 6-7% assumed that 100% of those enrolled in each plan in 2024 renewed the exact same policy (without any attrition or additional enrollment), which of course is never the case...even if total QHP selections were identical year over year, not all of the enrollees would be the same people, millions of them would switch to different policies and so on.

New Hampshire has the lowest average ACA premiums for the second year in a row at $469/month, while West Virginia once again has by far the highest at a whopping $1,170/month...up $51 from last year. Again, these are the unsubsidized average prices.

Now it's time to move on to the actual demographic breakout of 2025 Open Enrollment Period (OEP) Qualified Health Plan (QHP) enrollment.

First up: Breaking out new enrollees vs. existing enrollees who either actively re-enroll in an exchange plan for another year or who passively allow themselves to be automatically renewed into their current plan (or to be "mapped" to a similar plan if the current one is no longer available).

Nationally, 17% of all exchange QHP enrollees were new this year. The other 83% are current enrollees who signed up for another year, either actively (39%) or passively (45%).

New York had the lowest percent of new enrollees (11%), while Minnesota had the highest at 28%.

As I've noted before, there's still a massive divide between federal and state-based exchanges when it comes to active renewals: Over 45% of federal exchange states actively renewed (which is good!)...but only 22% of state-based exchange enrollees did. Active renewals range from just 8% in Rhode Island & DC to 58% in Utah.

The most recent press release from the Centers for Medicare & Medicaid Services (CMS) which included actual enrollment data about the 2025 ACA Open Enrollment Period (OEP) came out back on January 17, 2025 as one of the final communications from the outgoing Biden/Harris Administration.

This press release didn't include any accompanying Public Use Files (PUFs) since it only included semi-final enrollment data for the 2025 period.

Final top-line numbers were available for the 31 states hosted via the Federally Facilitated Marketplace (FFM), HealthCare.Gov...but the enrollment data was still preliminary for the 20 State-Based Marketplaces (SBEs), several of which hadn't even wrapped up Open Enrollment yet (including CA, DC, MA, NJ, NY, RI & VA). A few states final enrollment deadlines wouldn't hit until January 31st, over a week into the new Musk/Trump Regime.

Over at Evensun Health, Wesley Sanders has written about two newbulletins from the Centers for Medicare & Medicaid Services (CMS) which, if followed to their conclusion, would cause massive changes to how ACA individual market policies are priced and marketed...along with dramatic changes to net premiums, deductibles, co-pays & other out of pocket expenses for exchange enrollees.

Warning: This one is not only absurdly wonky, it requires me to fire up the Wayback Machine and dig deep into the ACA's 15-year history. I actually wrote about this prospect back in January, but I haven't read or seen anything else about it since then...until today.

There's two new stories out about where things stand with Congressional Republicans obsessive desire to gut Medicaid & kick millions of people off their healthcare coverage in order to give massive tax cuts to billionaires. The first, from Jessie Hellmann, Sandhya Raman and Olivia M. Bridges at Roll Call, has some pretty positive-sounding news:

...Johnson, R-La., said leadership had ruled out two Medicaid policies that could go a long way toward meeting the Energy and Commerce Committee’s $880 billion, 10-year savings target but faced strong pushback from blue-state GOP centrists.

First, Johnson said the emerging package wouldn’t touch the Federal Medical Assistance Percentage, or FMAP, rate — the portion of state Medicaid costs borne by the federal government — for the Medicaid expansion population, which is currently 90 percent.

Johnson also poured cold water over a provision that would implement per capita caps on Medicaid benefits for enrollees in expansion states, though he wasn’t quite as definitive on that front.

Gov. Whitmer Releases Top Lines of Alarming Report on Federal Medicaid Cuts, Finding Cuts Would Terminate Health Care for 700,000 Michiganders

MDHHS report also shows federal cuts to Medicaid will increase costs for hospitals and small businesses, and significantly strain state budget

LANSING, Mich. -- Today, Governor Gretchen Whitmer released toplines of an alarming report from the Michigan Department of Health and Human Services (MDHHS) on the impact of federal proposals to cut Medicaid. According to the new report, these proposed cuts would result in a loss of health care coverage for hundreds of thousands of Michiganders, reduce access to providers for all residents, increase financial burdens on hospitals and small businesses, and significantly strain the state’s budget.

Two years ago, with all the controversy over the frighteningly quick expansion of machine learning technology (popularly known as Artificial Intelligence (AI), even though it's not really that) over the few years into every facet of our lives, I decided to run a quick experiment using ChatGPT. My request was pretty simple:

"Write a blog post in the style of Charles Gaba."

I didn't include anything about healthcare or the Affordable Care Act...just my name.

You can see what it came back with at the link. I concluded at the time:

Aside from the fact that I'm not a pirate and don't generally use "themes" for my blog posts anyway...the larger issue here is that the text generated by ChatGPT doesn't include any specific information.

Every year around this time I start my annual individual & small group market rate filing analysis project. This involves spending months painstakingly tracking every insurance carrier rate filing for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to change.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier: How many effectuated enrollees they have in ACA-compliant policies this year; the average projected rate change for those policies; and, ideally, a breakout of the rationale behind the changes.

Usually the reasons given are fairly vague things like "increased morbidity" (ie, a sicker risk pool) or the like. Sometimes, however, there's a very specific reason given for some or all of the premium changes. Major examples of this include:

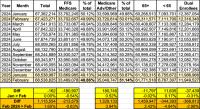

In December 2024, 78.8 million individuals were enrolled in Medicaid and CHIP.

71.5 million individuals were enrolled in Medicaid, and 7.3 million individuals were enrolled in CHIP.

41.4 million adults were enrolled in Medicaid, and there were 37.4 million Medicaid child and CHIP enrollees.

Medicaid and CHIP Applications Received

In December 2024, Medicaid, CHIP, Human Services agencies, and State-based Marketplaces received 3.0 million applications, or 11 percent more applications, as compared to November 2024.

The number of applications received has increased by 30 percent since December 2023 and increased by 84 percent since December 2022.

Total Medicaid/CHIP enrollment in December 2024 dropped slightly from November, by 171,000 people or 0.2%.

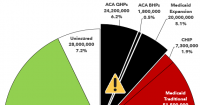

With all the understandable focus on Congressional Republicans efforts to effectively end Medicaid coverage for nearly 21 million Americans enrolled via ACA expansion, there's been much less attention paid to the other looming threat to healthcare coverage: The expiration of the upgraded financial subsidies for ~24.2 million ACA exchange enrollees, which are currently scheduled to end this New Year's Eve.

As I've explained numerous times before, the ACA's original premium subsidy formula was always far too stingy to make individual market policies affordable for many people...and worse yet, the subsidies cut off entirely for households making more than 4 times the Federal Poverty Level (FPL).

CVS Plans To Exit Obamacare In 2026, Affecting 1 Million Aetna Members

CVS Health plans to exit the individual health insurance business also known as Obamacare next year, leaving about 1 million Aetna members in 17 states looking for new coverage in 2026.

...CVS’ move to exit the individual insurance market comes as the Donald Trump White House and Republicans in Congress ponder cuts to health insurance benefits to pay for tax cuts for wealthy Americans. Trump has never been a fan of Obamacare, which he tried and failed several times to repeal in his first term, and his administration has already made moves to cut spending on such health benefits, already slashing what the federal government spends on navigators that help people sign up for Obamacare coverage.

Meanwhile, it remains unclear whether subsidies Americans use to buy individual coverage will remain once Congress has passed its budget.