I've spent the past couple of weeks up to my ears in 2025 annual healthcare policy rate filing analysis, so I haven't gotten around to addressing JD Vance's recent appearance on NBC in which he finally explained exactly what Donald Trump's "concept of a plan" for healthcare is:

When Donald Trump stammered at the recent presidential debate that he had “concepts of a plan” for Americans’ health care, he came across like a child who had forgotten his homework. But thanks to his campaign and his running mate JD Vance, we know now the Republican ticket really does have some “concepts.” Those concepts are bringing health care into the election — and presenting a tremendous opportunity to Vice President Kamala Harris.

Last Sunday, Vance raised the eyebrows of anyone familiar with health care policy when he told NBC’s Kristen Welker about Trump’s “deregulatory agenda.”

The summary table below provides an overview of proposed average rate changes for plan year 2025 in the individual health insurance market as reported by the insurers.

It is important to note that while these are initial rates as proposed and filed, rates are subject to review by the Departments of Commerce and Health. Final approved rates may vary from these proposed rates for many reasons.

Proposed rates do not reflect the impact of federal premium tax credits that are available to eligible Minnesotans who purchase their coverage through MNsure.

Additionally, the change in actual premium a consumer will pay in 2025 can vary from the proposed average change due to factors such as the specific plan selected, geographic rating area and age.

Small Group Market Proposed Average Rate Changes for Plan Year 2025

Congress Urged to Act Now to Prevent Increase in Health Coverage Costs For Pennsylvanians

The enhanced premium tax credits from the American Rescue Plan and the Inflation Reduction Act have placed high-quality health coverage within reach for hundreds of thousands of Pennsylvanians. Unless Congress extends these savings, many Pennsylvanians will lose the coverage that protects their health and financial security.

Pennsylvania – September 11, 2024 – Yesterday, Devon Trolley, Executive Director of Pennie – PA’s official health insurance marketplace – and Chairman of the Pennie Board, Michael Humphreys, issued a letter to Pennsylvania’s representatives in Congress strongly urging them to act now to extend the enhanced premium tax credits that dramatically reduce the cost of health coverage through Pennie for hundreds of thousands of Pennsylvanians.

Findings show that while New Jersey benefits from high-quality care, health care costs have risen rapidly over nearly a decade

TRENTON – The Murphy Administration today released a trio of reports assessing the quality and affordability of health care in New Jersey. These reports serve as a critical first step to understanding and addressing the health care affordability challenge impacting individuals and families both in the state and across the nation. Together, the reports show that a lack of affordable health care continues to burden New Jerseyans, and they will be instrumental in supporting the development of innovative and collaborative approaches to address high costs.

Nevada Health Link Broker/Agents Awardees Announced for Plan Year 2025, Enhancing Free Available Assistance

Award funds support marketing and outreach initiatives to amplify and expand open enrollment efforts through NevadaHealthLink.com

CARSON CITY, Nev. – Nevada Health Link has announced eight licensed brokers/agents who were selected for the Plan Year 2025 Broker Award Program. The Broker Award Program is an annual program where Nevada Health Link awards funding to a select group of brokers who propose innovative approaches to amplify marketing, outreach, and operational expenses related to storefront locations during the upcoming Open Enrollment Period that will run from November 1, 2024, through January 15, 2025. Applicants submit a robust proposal and are evaluated by Nevada Health Link staff as part of the selection process.

Health Connector member survey finds 88 percent have used new coverage, one in five have used preventative services previously deferred

August 28, 2024 – A new report published today by the Health Connector shows that the ConnectorCare pilot expansion enabled access to lower-cost health insurance to over 51,000 Massachusetts residents and many new participants benefit from the program’s financial protections.

The pilot expansion, part of the Fiscal Year 2024 state budget, is available to residents for Calendar Years 2024 and 2025. The expansion lifted income eligibility limits to the program from 300 percent to 500 percent of the federal poverty level – from $43,740 to $72,900 for an individual, and from $90,000 to $150,000 for a family of four.

SACRAMENTO, Calif. — Covered California announced that the statewide weighted average rate change for dental plans offered through the marketplace in 2025 will be 1.55 percent.

Covered California also announced that consumers will have more choice among dental plans with the addition of a new dental carrier, Humana, that will offer full statewide coverage in 2025.

Affordable Care Act Marketplace Coverage for the Self-Employed and Small Business Owners

Before the Affordable Care Act (ACA) was enacted in 2010, self-employed workers and small business owners had limited options to purchase affordable, high-quality health coverage. While most Americans obtained health coverage through their jobs, self-employed workers and small business owners often needed to purchase health coverage on their own, in which case quality coverage was expensive and sometimes denied.

The Affordable Care Act established Marketplaces in all states beginning in 2014. Self-employed workers and small business owners, as well as anybody else who does not have other access to affordable health coverage, can purchase it on their own and can qualify for tax credits if their premiums would otherwise be unaffordable as a share of their income.

In May 2024, 80,855,947 individuals were enrolled in Medicaid and CHIP, a decrease of 840,795 individuals (1.0%) from April 2024.

73,793,274 individuals were enrolled in Medicaid in May 2024, a decrease of 846,948 individuals (1.1%) from April 2024.

7,062,673 individuals were enrolled in CHIP in May 2024, an increase of 6,153 individuals (0.1%) from April 2024.

As of May 2024, enrollment in Medicaid and CHIP has decreased by 13,012,059 individuals (13.9%) since March 2023, the final month of the Medicaid continuous enrollment condition under the Families First Coronavirus Response Act (FFCRA) and amended by the Consolidated Appropriations Act, 2023.

Medicaid enrollment has decreased by 12,937,285 individuals (14.9%).

CHIP enrollment has decreased by 74,774 individuals (1.0%).

Between February 2020 and March 2023, enrollment in Medicaid and CHIP increased by 23,023,434 individuals (32.5%) to 93,868,006.

Medicaid enrollment increased by 22,681,263 individuals (35.4%).

CHIP enrollment increased by 342,171 individuals (5.0%)

Normally, states will review (or "redetermine") whether people enrolled in Medicaid or the CHIP program are still eligible to be covered by it on a monthly (or in some cases, quarterly, I believe) basis.

However, the federal Families First Coronavirus Response Act (FFCRA), passed by Congress at the start of the COVID-19 pandemic in March 2020, included a provision requiring state Medicaid programs to keep people enrolled through the end of the Public Health Emergency (PHE). In return, states received higher federal funding to the tune of billions of dollars.

As a result, there are tens of millions of Medicaid/CHIP enrollees who didn't have their eligibility status redetermined for as long as three years.

Every month for years now, the Centers for Medicare & Medicare Services (CMS) has published a monthly press release with a breakout of total Medicare, Medicaid & CHIP enrollment; the most recent one was posted in late February, and ran through November 2022.

Every year, I spend months painstakingly tracking every insurance carrier rate filing nationally for the upcoming year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need. The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier:

After last year's near-chaos on Virginia's individual market, things seem to be much calmer & less interesting this year. The premium increases for 2025 being requested by individual market carriers have a weighted average of 4.0%, while small group market carriers are asking for 6.8% increases on average.

The most noteworthy news for 2025 is that Aetna Life Insurance (their EPO division) is exiting the Virginia market, although Aetna Health (HMOs) is sticking around.

UPDATE: I thought Piedmont was also pulling out in 2025, but it turns out they left Virginia's individual market last fall at the very last minute.

In addition, it looks like Aetna is pulling completely out of the small group market, as is Innovation Health and, again, Piedmont Community.

Every year, I spend months painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need. The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier:

Via the New York Dept. of Financial Services, the preliminary, weighted average rate increases being requested for individual market health insurance policies for 2025 sound bad: 16.6% overall according to DIFS. I get a slightly lower weighted average of 16.2%, but it still ain't pretty.

Two of the highest increases are for carriers which are only offering policies off-exchange next year and which have fewer than 100 enrollees each anyway (Aetna and UnitedHealthcare Insurance Co. of NY); I assume they're both winding down their operations in the state.

As for the rest, they range from requested average increases of "only" 8.8% for the other UHC division to a stunning 51% rate hike by Emblem (HIP). The justification summaries are below the table.

It's important to remember that these are not final rate increases--New York in particular has a tendency to slash the requested rate hikes down significantly before approving them.

The Oregon Division of Financial Regulation (DFR) has finalized the rate decisions for 2025 health insurance for the individual and small group markets. The division reviews and approves rates for these markets through a detailed and transparent public process before they can be charged to policyholders.

This transparent process includes actuarial analysis provided to the public, public hearings, and a public comment period. Annually, insurance companies submit rate filings for the upcoming plan year. These filings are rigorously reviewed by division actuaries during a monthslong public review process. That process is now final and Oregonians will see an average rate increase of 8.3 percent in the individual market and a 12.2 percent increase in the small group markets.

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has 9 different carriers participating in the individual market in 2025. This is down from ten this year--ConnectiCare appears to be dropping out of the Massachusetts market.

One thing which sets Massachusetts (along with Vermont) apart from every other state is that their Individual and Small Group risk pools are merged for premium setting purposes.

Normally you would think this would make my job easier, since I only have to run one set of analysis instead of two...but until recently, it was surprisingly difficult to get ahold of exact enrollment data for each carrier on the merged Massachusetts market (and even more difficult to break out how many are enrolled in each market since they're merged...not that that's relevant to the actual rate changes).

OLYMPIA, Wash. — Thirteen health insurers filed an average requested rate increase of 11.3% for Washington's individual health insurance market. The proposed plans and their rates are currently under review and final decisions will be made this fall.

"I recognize that any proposed increase in price is deeply upsetting to those struggling to pay for coverage today,” said Insurance Commissioner Mike Kreidler. “People should know that these rates are not final and my office will be carefully reviewing each request to validate the assumptions being made by our state’s insurers. We will do everything under our authority ensure that any rate changes are justified."

Health Carriers Propose Affordable Care Act Premium Rates for 2025 New carrier files to enter individual market statewide

BALTIMORE – The Maryland Insurance Administration has received the 2025 proposed premium rates for Affordable Care Act products offered by health and dental carriers in the individual, non-Medigap and small group markets, which impact approximately 496,000 Marylanders. This includes rate submissions from Wellpoint Maryland Inc., an HMO that will begin offering Affordable Care Act products in Maryland for the first time.

Each year insurers that sell Individual and Small Group plans in Maine's pooled risk market must submit their proposed forms and rates to the Bureau of Insurance, using the System for Electronic Rate and Form Filing (SERFF). Details of the filings submitted to the state since June 10, 2010 can be viewed in the system.

To see details of a filing, click on the Search Public Filings button below and paste or type in the relevant SERFF Tracking Number listed in the table (no need to complete the rest of the form).

There's a couple of noteworthy items going on here:

I'm pleasantly surprised to report that after several years of Kentucky's rate filings being heavily redacted, this year at least (and hopefully going forward), I was able to acquire the actual enrollment data for all of them...not just the individual market, but the small group market as well!

There are four carriers offering policies on the KY individual market (Anthem, CareSource, Molina and WellCare), with an weighted average rate change request of 8.5%, while the small group carriers are requesting steeper average increases of 17.8% for what seems to be shrinking market.

UPDATE 9/19/24: OK, it looks like the approved rate filings have been uploaded to the SERFF database. Average unsubsidized individual market premiums will be going up 7.9%, while small group rates will see a 16.6% average increase.

(Washington)– The District of Columbia Department of Insurance, Securities and Banking (DISB) has received 193 proposed health insurance plan rates for annual review in advance of open enrollment for plan year 2025. The proposed rates were submitted for DC Health Link, the District of Columbia’s health insurance marketplace, from CareFirst BlueCross BlueShield, Kaiser and United Healthcare.

The proposed rates are for individuals, families and small businesses for the 2025 plan year. Overall, the number of plans submitted for 2025 is down by 22 from those submitted for 2024. The number of small group plans decreased from 188 to 166 while the number of individual plans remained at 27.

Arkansas is a problematic state for many reasons, but I have to give their insurance dept. website high praise for posting their annual rate filings in a clear, simple & comprehensive fashion (which is to say, not only do they post the avg. premium changes for each carrier, they also post the number of covered lives for each, which is often difficult for me to dig up). Better yet, they also include direct links to the filing summaries and include the SERFF tracking number for each in case I need to look up more detailed info.

Anyway, there's nothing terribly noteworthy in the 2025 filings. Insurance carriers are seeking an average 4.2% rate hike on the individual market and 9.6% for small group plans.

HMO Partners (Health Advantage) appears to be dropping out of the small group market, but otherwise it looks pretty calm.

The big news on the individual market is that Aetna is seeking massive rate hikes of over 34% next year, though the weighted average across the board being requested is "only" a still ugly 13.3% increase.

On the small group market, average increases are the lower but still-not-great 8.8%. More significantly here is that Aetna and Optimum Choice are pulling out of the Delaware small group market entirely, reducing the number of carriers from six to just two, since Aetna had three divisions operating there.

The overall proposed average rate increase for 2025 Indiana individual marketplace plans is -1.6%.

The IDOI will finalize the review of the 2025 ACA compliant filings both on and off the federal Marketplace by August 16, 2024. The Centers for Medicare and Medicaid Services (CMS) will issue the ultimate approval for the Marketplace plans sold in Indiana. CMS will issue its approval on or before September 18, 2024.

CONNECTICUT INSURANCE DEPARTMENT RELEASES HEALTH INSURANCE RATE REQUEST FILINGS FOR 2025

The Connecticut Insurance Department (CID) has received eight rate filings from seven health insurers for plans that will be available on the individual and small group market, both on and off the state-sponsored exchange, Access Health CT. As part of our regulatory responsibilities, we will conduct a thorough examination of these filings to ensure that the requested rates comply with Connecticut’s insurance laws and regulations.

Hawaii only has two health insurance carriers serving the individual market, Hawaii Medical Service Assocation and Kaiser Foundation Health Plan. Both of them have submitted their proposed premium rate filings for 2025: HMSA is requesting a 7.6% hike, while Kaiser is only asking for a 4.0% bump. The weighted average is 6.4%.

On the small group market, the 5 carriers participating are requesting unweighted average increases of 7.1% statewide.

UPDATE 9/19/24: Hawaii regulators have uploaded the approved 2025 rate filings for the individual market only (I assume the small group filings will be uploaded soon). HMSA's rates will be going up slightly more than originally requested, but overall not much changed.

It's worth noting that Hawaii has a larger portion of its individual market enrolled in off-exchange policies than most states...around 37%, which means only 53% of the total indy market is subsidized at the moment.

Florida state law gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret." In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

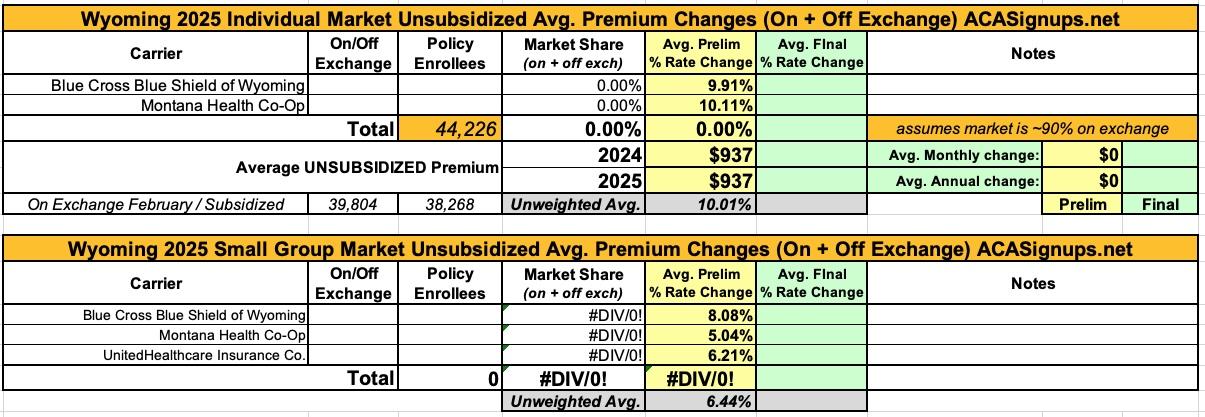

The bad news for Wyoming residents who earn too much to qualify for any federal ACA subsidies is that the state has the second highest unsubsidized premiums in the country after West Virginia. The good news is that, thanks to the Inflation Reduction Act, there are far more residents who do qualify for federal subsidies, which chop those premiums down to no more than 8.5% of their income....at least until the end of 2025, at which point the upgraded IRA subsidies are currently scheduled to expire.

Unfortunately, once again, I've been unable to get ahold of enrollment data for any of Wyoming's carriers on either the individual or small group markets, so I can only run unweighted averages for both markets.

With that said, the unweighted average rate hikes being asked for are 10% on the indy market and 6.4% for small group plans.

Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual (14) and small group (16) markets. Their small group market is losing 2 carriers next year (All Savers and Common Ground Health Co-op), but it's still pretty robust.

The bad news is that it's once again extremely difficult to acquire Wisconsin's actual rate filings prior to the actual Open Enrollment Period launching, meaning I can only run unweighted average requested rate increases/decreases for the most part, although I've made a crude attempt at a partially-weighted average for the individual market.

With that in mind, individual market carriers are requesting unweighted increases of around 9.1%, while small group carriers are seeking hikes of around 7.4% overall.

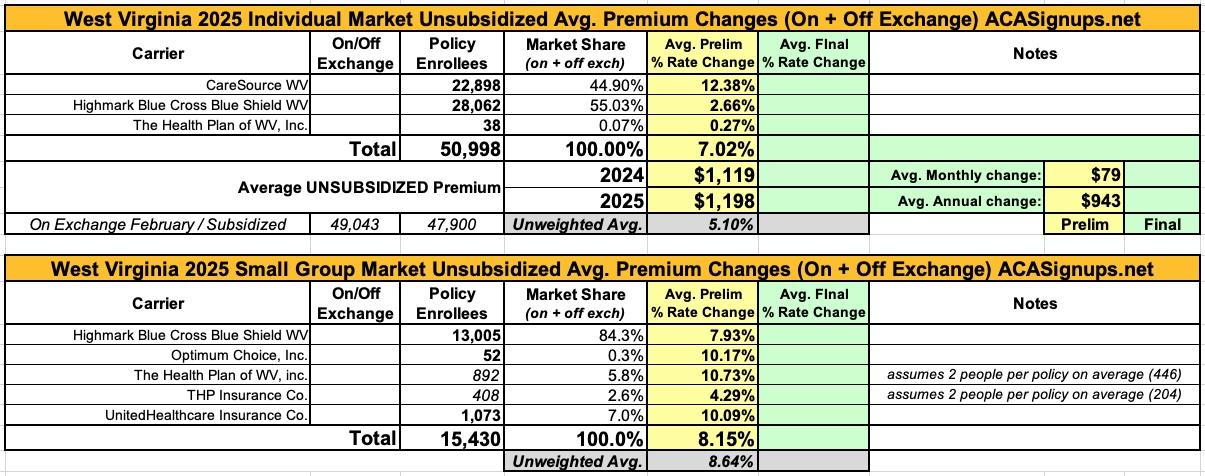

Well whaddya know? After years of their actuarial memos being redacted and/or filing summaries missing critical info, this year I'm suddenly able to access all the data I need!

West Virginia carriers are asking for average rate hikes of 7% on the individual market and 8.2% for small group plans.

The 7% hike is pretty close to the average nationally on a percentage basis...but since West Virginia also already has by far the highest average unsubsidized premiums in the nation, that's ugly news, especially if the enhanced ACA subsidies provided by the Inflation Reduction Act are allowed to expire starting in 2026...

Utah's preliminary 2025 individual and small group market rate filings are listed below. They launched a handy new website specifically dedicated to insurance filings, which is nice to see.

Unless there's a change in the final/approved rates, unsubsidized individual market plan premiums are increasing by around 10.4% in 2025, while small group plans will go up 8.9% on average.

It's worth noting that Cigna Health & LIfe is pulling out of Utah's individual market next year, while Angle Insurance Co. is dropping out of the small group market.

It's also worth noting that virtually all of Utah's individual market enrollment appears to be on exchange this year...over 95% of it! It's slightly lower than that since I don't know how many enrollees Cigna has at the moment, but they only reported around 3,000 effectuated enrollees as of a year earlier, so unless they had massive growth this year (which could have happened, I suppose), it would only knock the on exchange percentage down a point or two.

Cigna notwithstanding, this means that in Utah:

95.3% of all indy market enrollees are on exchange

As always, the Texas individual and small group markets are pretty messy. For starters, they have up to 20 individual market carriers depending on the year, along with over a dozen small group market carriers some years (this year they're at 17 and 8 respectively).

On top of that, as is also the case in some other states, some of the names of the insurance carriers can be confusing as hell. There's the "Insurance company of Scott & White" which seems to have changed its name to "Baylor Scott & White Insurance Co.," which isn't to be confused with "Scott & White Health Plans" and so on.

I was only able to acquire hard enrollment data for five of the carriers on the individual market this year, and one of those doesn't really count since they're brand new and don't have any (Wellpoint Insurance Co.). For another 11 of them the rate filings include the number of policyholders but not the actual number of covered lives; for those I'm using an average 1.4x multiplier, based on the actual multiplier found in the carriers I have both numbers available for.

Tennessee's preliminary 2025 individual & small group market health insurance rate filings are now available. Unfortunately, I can't find any unredacted filing forms for any of them (and in fact most of the rate filings aren't showing up in the SERFF database at all).

For the most part there's not much to see at first glance: Requested rate changes range from a 1.3% drop to a 3.9% increase on the individual market and from a 9.7% to 11.2% increase for small group plans. The unweighted averages are +1.4% and +10.6% respectively.

However, it also looks like several carriers are dropping out of each market in Tennessee: Alliant and US Health & Life (Ascension) don't show up on the federal Rate Review database for the individual market, while Aetna and CIGNA are missing for small group listings.

Assuming the exchange-based market makes up roughly 85% of total individual market enrollment in Tennessee, the total indy market should be around 628,000 people.

Pretty straightforward in the Mount Rushmore state. Three carriers on the individual market; around 56.4K enrollees total. The weighted average rate change across all three is +2.3% if approved as is.

Note that I've added a new feature to my rate change spreadsheet this year: I've started including the on exchange effectuated enrollmentas well as the subsidized on exchange enrollment as of February for every state. This will allow me to calculate the percent of the total individual market which is receiving ACA subsidies...at least in states where I'm able to figure out what total off-exchange enrollment is (typically only around half of them).

In South Dakota, for instance:

95.7% of on exchange enrollees are subsidized (49,250 / 51,416)

87.2% of the total market is subsidized (49,250 / 56,457)

On exchange enrollment makes up around 91% of the total individual market

For the small group market, there are five carriers this year; Medica Insurance Co. appears to be pulling out of the state. The weighted requested average rate change is a 2.8% increase.

I got so far behind on my annual rate filing project that some of the states have started issuing their APPROVED changes before I got around to analyzing the REQUESTED rate changes. Ah, well...

LINSEY DAVIS: This is now your third time running for president. you [Trump] have long vowed to repeal and replace the Affordable Care Act, also known as Obamacare. You have failed to accomplish that. You now say you're going to keep Obamacare. Quote, unless we can do something much better. Last month you said, quote, we're working on it. So tonight, nine years after you first started running, do you have a plan and can you tell us what it is?

Oklahoma is another state where I have no access to the actual enrollment data--all I have to go by are the average requested rate changes for each carrier on the individual and small group markets. As a result, the averages for each market are unweighted.

For individual market plans, that unweighted average is a slight decrease of 0.7%, though the carriers range from as low as a 12% drop to as high as a 10% increase.

It's worth noting that BlueLincs HMO, which was only added to the OK individual market last year, is already being removed from it. In fact, as shown below, it looks like BlueLincs was a special line of policies offered at the point of a regulatory gun; apparently Blue Cross was required to create it as an option for group coverage members who move off of employer coverage. However, that regulation was apparently changed shortly thereafter, and no one ever actually enrolled in a BlueLinc plan anyway, so that's that.

For the small group market, average requested rate hikes range from as little as 4.0% to as much as a 15.2. The unweighted average is 8.3%

1 in 7 U.S. residents covered through Affordable Care Act health insurance marketplaces over the last decade, with all-time high enrollment under Biden-Harris Administration

WASHINGTON – Today, the U.S. Department of the Treasury released new data showing that nearly 50 million Americans, or 1 in 7 U.S. residents, have been covered through the Affordable Care Act marketplaces since January 2014. Under the Biden-Harris Administration, which has lowered the cost of marketplace coverage by expanding the premium tax credit, the number of Americans covered through the marketplaces has significantly increased, reaching an all-time high of 20.8 million following open enrollment for 2024—18.2 million Americans have enrolled for the first time since January 2021.

As a result, I've been able to put together a weighted average requested rate increase for the individual market, which comes in at +3.9%.

For the small group market, I have to go with an unweighted average of +12.0%. It's also worth noting that it looks like one of Aetna's divisions is pulling out of the OH small group market, as are two fof the 4 (!) UnitedHealthcare divisions and possibly AultCare, although I'm not sure about that one.

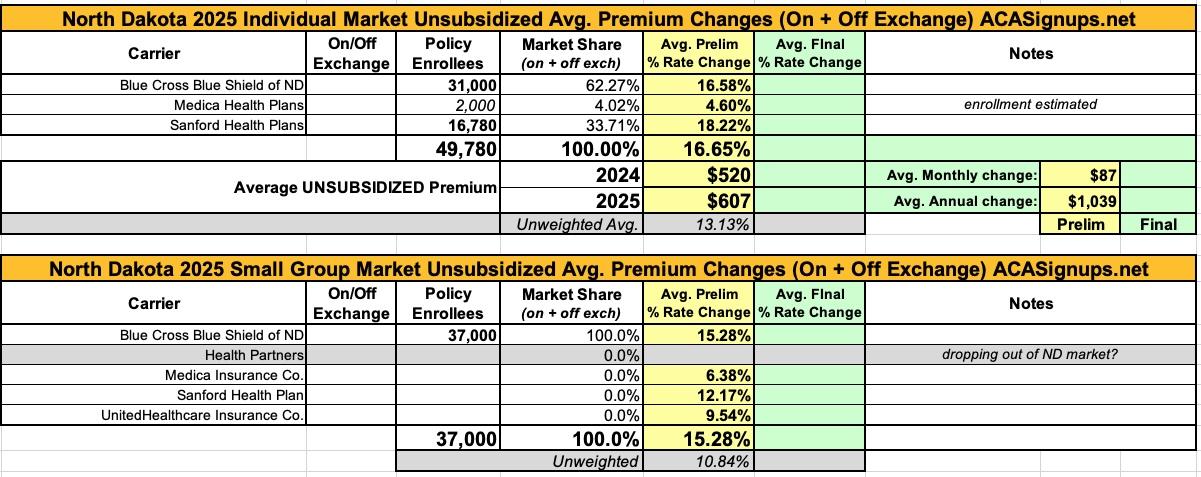

North Dakota only has 3 carriers participating in their individual health insurance market and four in their small group market, since it appears that Health Partners will be pulling out of the latter next year.

For the indy market, the weighted average premium increase being requested is a painful 16.7%, although this may be off slightly due to Medica's enrollment number being a rough estimate (last year's total ND market was only 45,000 people; I'm assuming Medica only has around 2,000 enrollees this year).

For the small group market, I only have the unweighted average rate hikes, which come in at 10.8%.

New Jersey individual & small group market carriers are asking for unweighted average rate increases of 7.3% and 4.5% respectively for 2025. However, the unweighted averages don't tell the whole story--the carriers are asking for rate hikes ranging from as low as 3.8% to as high as 16.2% on the individual market, and from as low as an 18.8% reduction to a 12.3% increase for small group plans.

As is the case with far too many states these days, most of the rate filing memorandums are heavily redacted in New Jersey, making it nearly impossible to get ahold of the actual enrollment numbers, which means I have no way of running a weighted average on either market.

I should note that the 433,000 estimate for New Jersey's total individual market is based on the assumption that 90% of it is via the ACA exchange, with only 10% being enrolled off-exchange.

Nebraska doesn't even bother listing indy/small group plan rate filings on their own insurance department website...the link goes directly to the federal Rate Review database. The problem with this is that very few filings here are unredacted, which means it's difficult to acquire the policy enrollees for many carriers needed to run a weighted average.

Nebraska has 4 carriers on the individual market for 2025: BCBS, Medica, NE Total Care and Oscar Health. The unweighted average rate increase being requested is around 4.0%.

For the 4 Small Group market carriers, I do have enrollment data for two of them, but without knowing the other two this isn't terribly useful. The unweighted average rate change being requested there is a 9.3% increase.

The good news is that this year at least, the SERFF database has both the average rate changes as well as the 2024 effectuated enrollment for all carriers on both the individual and small group markets. There's one curiousity, however: For the small group market, UnitedHealthcare shows up in the SERFF database but doesn't appear on the federal Rate Review website.

This doesn't really move the needle much either way, however, since UHC only reports having 250 enrollees anyway.

In any event, individual market carriers are requesting average 8.3% rate increases, while small group carriers are asking for similar 8.6% hikes.

Not a whole lot stands out to me other than SSM Health Insurance apparently dropping out of the states indy market and a new carrier, Bankers Reserve Life Insurance, newly joining it.

At the same time, the Missouri small group market appears to be losing two carriers (or three depending on your POV): Aetna Health, Aetna Life and Cigna Health & Life are all missing from the 2025 filing summaries as well as the federal Rate Review database.

In any event, the MO individual market is looking at average premium reductions of 1.7% if approved as is, while small group plans are likely to increase by about 7.9% overall.

As always, these are subject to state regulatory review and approval.

Unfortunately, Mississippi is another state which provides zero useful rate filing data for my purposes (preliminary or final) prior to the Open Enrollment Period launching. The only data I have is from the federal Rate Review website, and even the filing forms there are heavily redacted, so all I can put together are unweighted averages for the 2025 calendar year.

It's worth noting that Vantage Health Plan appears to be dropping out of the individual market, while All Savers appears to be dropping out of the states small group market (at least, neither one shows up on the Rate Review site or in a SERFF search, anyway).

With that in mind, unsubsidized individual market enrollees are looking for unweighted average increases of around 1.8%, while small group carriers are hoping to increase rates by around 9.8% (again, unweighted).

They break out the filings not between Individual and small group markets or on- vs. off-exchange policies, but between rate increases over and under 10%. Normally that would be fine, but they also have multiple listings within each market for several carrier.

Not that any of that matters this year, as they don't appear to have posted any of the ACA-compliant individual market filings there anyway. I had to rely entirely on the federal Rate Review site, and the filings there still don't include enrollment data for most carriers, so the averages below are all unweighted only:

Individual Market: Around 3.0% lower (in fact, 4 of the 5 carriers on the market next year are dropping average premiums at least slightly)

Small Group Market: 9.6% higher

It's worth noting, however that Louisiana Healthcare Connections appears to be dropping out of the individual market entirely.

Kansas is another state where the annual rate filings are redacted for many of the carriers; as a result, I can only run a semi-weighted average, and even that is dependent on my estimate of the total individual market size being accurate (my general rule of thumb as long as the enhanced subsidies of the IRA are in place is that about 90% of most states individual market enrollment is on-exchange unless I have data proving otherwise).

With that in mind, the carriers on the Kansas individual market are asking for rate hikes ranging from 2.1% - 24.4%, with an estimated semi-weighted average of 8.9%.

For the small group market, I can't even run a semi-weighted average since I have no idea what the KS small group market size is overall, but the unweighted average rate hikes being requested is 14.9%.

It's also worth noting that unless I'm missing something, US Health & Life Insurance seems to be pulling out of the Kansas individual market, while both Aetna and Cigna seem to be missing from the small group market.