Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Banner/Aetna CVS:

(Dropping out of the individual market for 2026.)

I am writing to notify the Department that Banner Health and Aetna Health Plan Inc. (“Banner | Aetna”) will exit the individual health insurance market effective December 31, 2025. This notification is sent pursuant to Department guidance and Arizona statute 20-1380(D)(1). We made this decision after careful consideration and after evaluating the evolution of business at Banner | Aetna. The details of our individual market exit include the following:

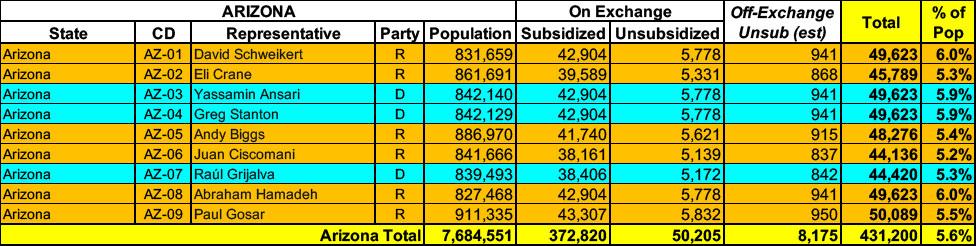

Arizona has around 423,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have perhaps another ~8,000 unsubsidized off-exchange enrollees.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Today, the U.S. Department of Health and Human Services (HHS), through the Centers for Medicare & Medicaid Services (CMS), approved section 1115 demonstration amendments that allow, for the first time ever, Medicaid and Children’s Health Insurance Program (CHIP) coverage of traditional health care practices provided by Indian Health Service (IHS) facilities, Tribal facilities, and urban Indian organizations (UIO). Today’s action is expected to improve access to culturally appropriate health care and improve the quality of care and health outcomes for tribal communities in Arizona, California, New Mexico, and Oregon, and will support IHS, Tribal, and UIO facilities in serving their patients.

The good news is that the federal Rate Review database has now posted the preliminary avg. 2025 rate filings for the individual and small group markets for every state. This makes it very easy to plug in the average requested rate changes in 2025 for every carrier participating in both markets.

The bad news is that most of the underlying filing forms are heavily redacted, meaning I can't use the RR database to acquire the other critical data I need in order to run a proper weighted average: The number of people actually enrolled in the policies for each carrier.

This means that in cases where this data isn't available elsewhere (either the state's insurance department website, the SERFF database or otherwise), I'm limited to running an unweighted average. This can make a huge difference...if one carrier is requesting a 10% increase and the other is keeping prices flat, that's a 5.0% unweighted average rate hike...but if the first carrier has 99,000 enrollees and the second only has 1,000, that means the weighted average is actually 9.9%.

February 16: CMS approved coverage expansions in Arizona through an amendmentof two policies, “Parents as Paid Caregivers” (PPCG) and “KidsCare Expansion." Approval of the Parents as Paid Caregivers amendment will allow the state to continue to reimburse legally responsible parents for providing direct care to their minor children, helping to mitigate the direct care worker shortage and improve access to timely, effective care in the home and community.

Additionally, the KidsCare Expansion amendment will allow the state to increase the Children’s Health Insurance Program (CHIP) eligibility thresholds from 200% of the federal poverty level (FPL) to 225% of the FPL. Expanding KidsCare is expected to improve the rate of child health insurance coverage, increase access to affordable health care coverage, decrease costs by addressing health needs earlier, when care is less expensive, and provide financial relief for families. The demonstration will remain in effect until September 30, 2027.

The good news is that the federal Rate Review database has now posted the preliminary avg. 2024 rate filings for the individual and small group markets for every state. This makes it very easy to plug in the average requested rate changes in 2024 for every carrier participating in both markets.

The bad news is that most of the underlying filing forms are heavily redacted, meaning I can't use the RR database to acquire the other critical data I need in order to run a proper weighted average: The number of people actually enrolled in the policies for each carrier.

This means that in cases where this data isn't available elsewhere (either the state's insurance department website, the SERFF database or otherwise), I'm limited to running an unweighted average. This can make a huge difference...if one carrier is requesting a 10% increase and the other is keeping prices flat, that's a 5.0% unweighted average rate hike...but if the first carrier has 99,000 enrollees and the second only has 1,000, that means the weighted average is actually 9.9%.

During the COVID pandemic emergency, Congress passed legislation which, among other things, required states to provide "continuous coverage" of people who enrolled in Medicaid or the CHIP program.

Normally Medicaid/CHIP enrollees have their eligibility statuses "redetermined" every month (or quarter in some states, I believe) to make sure they were still eligible for the program, but the Families First Coronavirus Response Act (FFCRA) stated that in order to receive increased federal funding of their Medicaid/CHIP programs, states couldn't kick anyone off as long as the public health emergency was in place (unless they died, moved out of state or asked to be disenrolled).

This requirement ended effective April 1st, 2023 via an omnibus bill passed back in December.