About 200,000 Virginians will be eligible to tap into new state funding meant to offset costs for insurance through the state’s Affordable Care Act exchange, starting in November.

This means that participants could save about 70% on their monthly premium, after state lawmakers and Gov. Abigail Spanberger approved $150 million dollars for it in the state budget late last month.

The move comes after federal funding shifts triggered by Congress’ failure to renew expiring ACA subsidies. Thousands of Virginians have dropped their coverage so far this year as premiums have shot up.

Virginia’s Health Benefit Exchange estimates that about 100,000 Virginians have lost their health coverage this year as a result of higher premiums, according to a new press release.

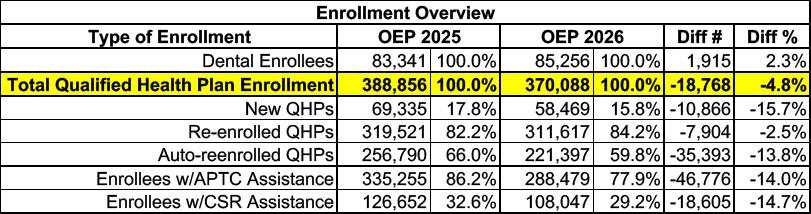

Here's the overview of Virginia ACA exchange enrollment over the course of OEP 2026 vs. 2025. Stand-alone dental plan enrollment is up 2.3%, which is nice, but overall major medical plan (Qualified Health Plan, or QHP) enrollment dropped by nearly 19,000 people, or 4.8% year over year.

There's also 14% fewer enrollees receiving federal tax credits than last year (nearly 47,000 people), while another 15% lost Cost Sharing Reduction assistance (CSR).

IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

With the 2026 ACA Open Enrollment Period officially starting on November 1st, and with millions of ACA enrollees being bombarded with scary letters from their insurance carriers and headlines warning of massive premium hikes, residents of six states* (as of this writing) can already enter their own household information to find out how much their net health insurance premiums are going to increase starting January 1st, 2026:

Twelve years ago, the Wall St. Journal ran a story about the impact of the American Taxpayer Relief Act of 2012, a sweeping tax bill signed into law by President Obama which locked in the Bush tax cuts for lower & middle-class households while allowing them to expire on schedule for wealthier Americans:

A compromise measure, the Act gives permanence to the lower rate of much of the Bush tax cuts, while retaining the higher tax rate at upper income levels that became effective on January 1 due to the expiration of the Bush tax cuts. It also establishes caps on tax deductions and credits for those at upper income levels. It does not tackle federal spending levels to a great extent, rather leaving that for further negotiations and legislation. The American Taxpayer Relief Act passed by a wide majority in the Senate, with both Democrats and Republicans supporting it, while most of the House Republicans opposed it.

...This letter is formal notice that Aetna Health Inc. (“AHI”) intends to exit from the Individual health insurance market in Virginia effective January 1, 2026. Subject to the Department’s review, we will mail the 180-day notices of discontinuance to covered individuals.

As of May 2025, our records show that AHI has 9,810 subscribers and 13,721 total members in Virginia.

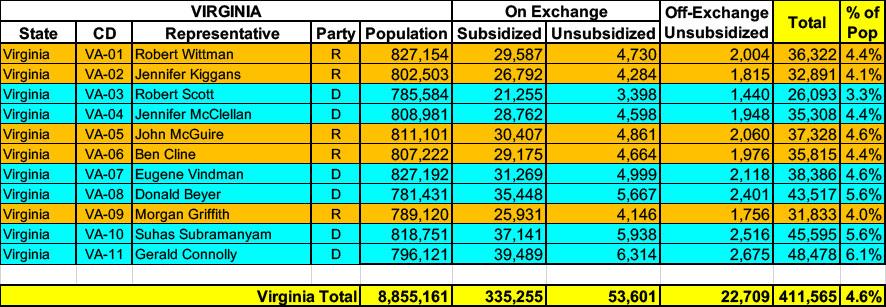

Virginia has ~388,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. They also have over 22,000 off-exchange enrollees. Combined, that's 411,000 people with ACA market coverage, or 4.6% of the total population.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.