Wisconsin has around ~293,000 residents enrolled in ACA exchange plans, 98% of whom are currently subsidized. I estimate they also have another ~19,000 unsubsidized off-exchange enrollees.

The average proposed rate increase of 12.6%, effective January 1, 2026 is expected to impact 13,677 members, based on membership as of March 31, 2025. The rate increase varies by plan, ranging between 4.4% and 20.5%. Rate changes vary by plan due to the impact of changes in benefits and rating adjustments to account for the non-funding of Cost Sharing Reduction (CSR) payments.

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

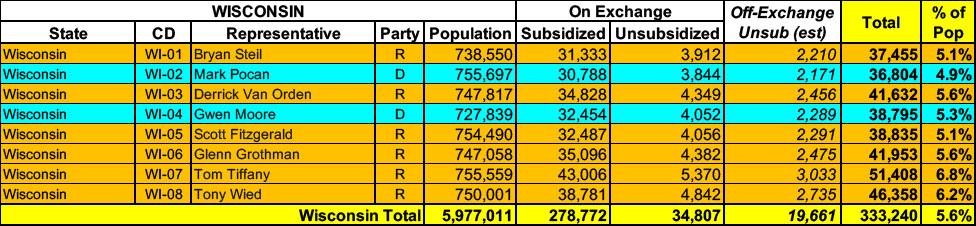

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual (14) and small group (16) markets. Their small group market is losing 2 carriers next year (All Savers and Common Ground Health Co-op), but it's still pretty robust.

The bad news is that it's once again extremely difficult to acquire Wisconsin's actual rate filings prior to the actual Open Enrollment Period launching, meaning I can only run unweighted average requested rate increases/decreases for the most part, although I've made a crude attempt at a partially-weighted average for the individual market.

With that in mind, individual market carriers are requesting unweighted increases of around 9.1%, while small group carriers are seeking hikes of around 7.4% overall.

It's been a long, long time since I've written about the "Sub26ers"...that is, the population of Americans age 18 - 25 who are enrolled in the same healthcare policy as their parents thanks to the ACA's provision mandating that insurance carriers allow them to do so. While I may be missing a more recent article, the last time I recall writing anything in depth about this was nearly a decade ago:

Long-time readers will remember that throughout the 2014 Open Enrollment period, there was much fuss and bother made by both the Obama administration, the HHS Dept., myself and some ACA detractors over the "sub26er" population: Young adults aged from 19-25 years old who are covered by their parents policies thanks to provisions in the Affordable Care Act requiring all new policies issued since 2010 to allow this.

At the time I was a bit obsessed with trying to suss out just how many Americans fell into this particular category. It was a tricky number to pin down for a number of reasons, but in the end it seemed to hover somewhere in the 2 - 3 million range, depending on your source.

Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual (14) and small group (18) markets. They're losing two carriers in 2024 (WPS Health Plan in both markets and Humana in the small group market only), but it's still pretty robust.

The bad news is that it's once again extremely difficult to acquire Wisconsin's actual rate filings prior to the actual Open Enrollment Period launching, meaning I can only run unweighted average requested rate increases/decreases.

With that in mind, individual market carriers are requesting unweighted increases of around 6.8% (ranging from 1% - 15.7%), while small group carriers are seeking hikes of around 7% overall, ranging from a 25.9% reduction (wow!) to a 16.3% increase.

UPDATE 11/08/23: No changes to any of the individual market rate requests; a couple of slight changes to the small group carriers.

I'm pretty sure Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual (15) and small group (20) markets.

The bad news is that it was extremely difficult to acquire Wisconsin's 2023 rate filings prior to the actual Open Enrollment Period launching this morning.

Overall, individual market premiums for unsubsidized enrollees are going up around 7.7%, while small group market rates are increasing by an unweighted average of 8.9%.

It's worth noting that two carriers (Health Tradition and Network) appear to be dropping out of the small group market, while one of the individual market players, Children's Community Health Plan, is changing their name to...Chorus Community Health Plan for whatever reason.

I'm pretty sure Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual and small group markets. A total of 37 are present at the moment, although 5 of the small group carriers don't appear on the federal Rate Review database as of yet.

Unfortunately, this is yet another state where the enrollment data has basically been buried, so I can only run unweighted average rate changes.

With that in mind, the individual market rates look to be nearly flat (dropping by 0.8% on average), while small group plans are going up 4.4%.