Oklahoma is another state where I have no access to the actual enrollment data--all I have to go by are the average requested rate changes for each carrier on the individual and small group markets. As a result, the averages for each market are unweighted.

For individual market plans, that unweighted average is a slight decrease of 0.7%, though the carriers range from as low as a 12% drop to as high as a 10% increase.

It's worth noting that BlueLincs HMO, which was only added to the OK individual market last year, is already being removed from it. In fact, as shown below, it looks like BlueLincs was a special line of policies offered at the point of a regulatory gun; apparently Blue Cross was required to create it as an option for group coverage members who move off of employer coverage. However, that regulation was apparently changed shortly thereafter, and no one ever actually enrolled in a BlueLinc plan anyway, so that's that.

For the small group market, average requested rate hikes range from as little as 4.0% to as much as a 15.2. The unweighted average is 8.3%

First, I want to apologize to all of my regular visitors for the 2-week gap in posting; a combination of personal committments and unjustified distractions resulted in my not posting any updates for a longer-than-acceptable period of time. I hope to try and make up for that over the next week or so.

The Colorado Division of Insurance (DOI) has completed its initial review of the health insurance plans that the companies have filed for 2025. The information below highlights the key information about the number of companies, plans and the premium changes the companies are requesting.

On July 25, 2024, the DOI will hold a virtual stakeholder meeting from 9:30-11:30 a.m. MDT, to share preliminary information regarding health insurance for 2025. This meeting will focus on highlights and trends the DOI has identified in its initial review of the information Colorado health insurers have submitted for 2025. People interested in attending this July 25 stakeholder meeting should register (via Zoom) using the following link - Register for July 25 Stakeholder Meeting(opens in new window).

TRUTH OR CONSEQUENCES – Gov. Michelle Lujan Grisham today signed into law legislation that builds on the administration’s work to make healthcare more affordable and accessible for every New Mexican.

“Delivering quality healthcare to New Mexico’s population requires a tailored approach that takes into account rural communities, New Mexicans benefiting from Medicaid, and the tens of thousands of public employees in our state,” said Gov. Lujan Grisham. “These are bills that are going to positively impact a vast swath of New Mexicans.”

The governor signed these important healthcare bills during a ceremony at Sierra Vista Hospital in Truth or Consequences.

As an aside, I was a bit confused about the name of the city so I looked it up. Huh.

Emergency rooms not required to perform life-saving abortions, federal appeals court rules

The Biden administration reminded hospitals of their obligation to perform life-saving abortions under the Emergency Medical Treatment and Labor Act after the overturn of Roe v. Wade. Texas sued, arguing it was an overstep that mandated abortions.

Federal regulations do not require emergency rooms to perform life-saving abortions if it would run afoul of state law, a federal appeals court ruled Tuesday.

After the overturn of Roe v. Wade in June 2022, the U.S. Department of Health and Human Services sent hospitals guidance, reminding them of their obligation to offer stabilizing care, including medically necessary abortions, under the Emergency Medical Treatment and Labor Act (EMTALA).

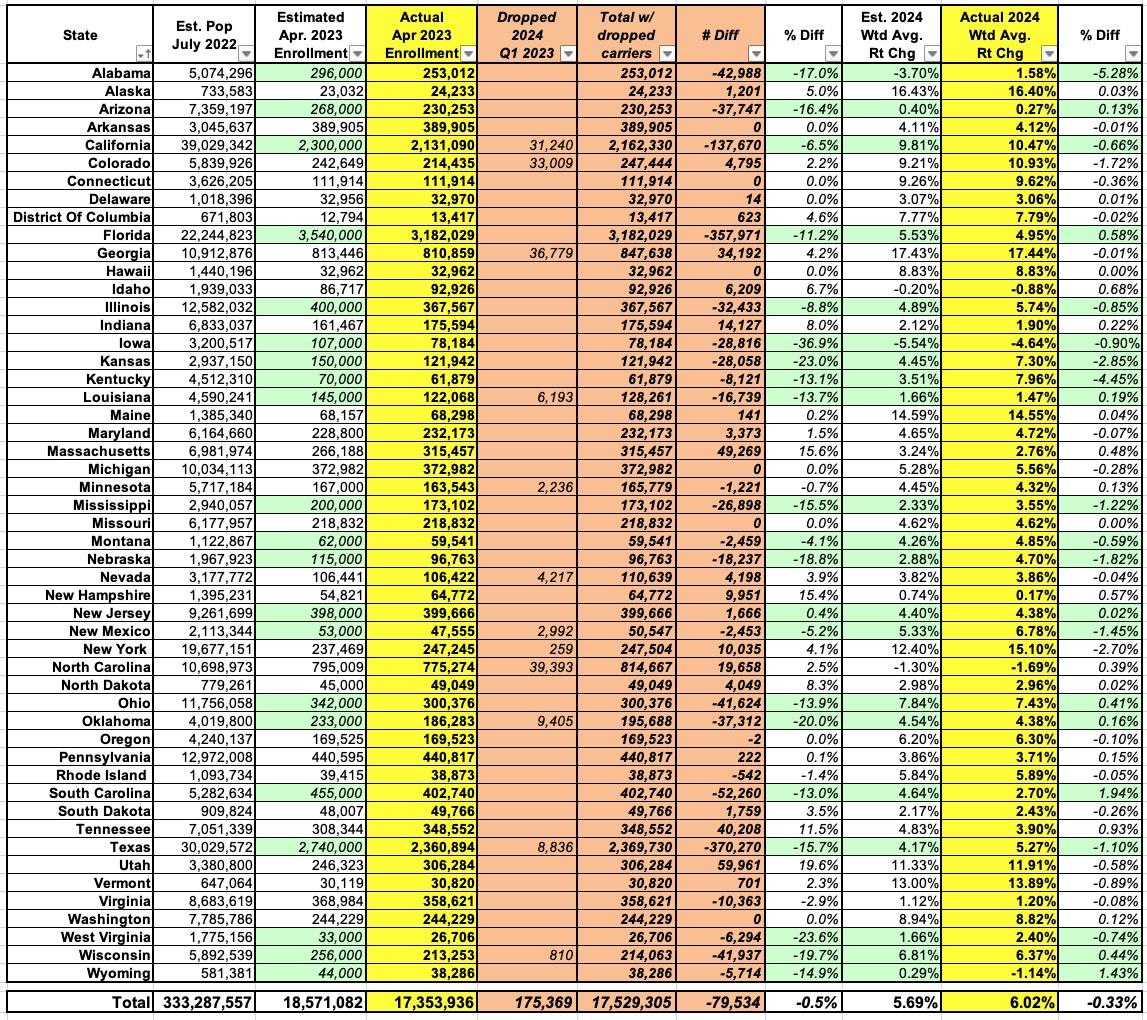

As regular readers know, every year I pore over hundreds of annual health insurance policy rate filings from carriers participating in the individual and small group markets, attempting to run weighted average rate changes on a state-by-state level. I then compile all 50 states (+DC) into a national weighted average rate change table.

I generally do this twice for every state: First, over the spring and summer, I crunch the numbers for the carriers preliminary rate change requests. These are submitted to the state regulatory authorities (or in a few cases, federal regulators), who run their own actuarial analysis and then either approve the requests as is, lower the requested rates or (in a few cases) even raise rates more than requested, since part of the regulators job is to ensure that the insurance carriers have enough cash flow to actually pay their claims over the upcoming year.

Fourteen health insurers have been approved to sell in Washington's 2024 individual health insurance market. Insurers requested an average increase of 9.11% but 8.94% was approved. How much premium someone pays will depend on the plan they select, the number of people covered, their age, whether or not they smoke and where they live.

West Virginia is yet another state where I'm unable to acquire unredacted actuarial memos and/or filing summaries in order to run weighted average rate changes, so I have to settle for unweighted averages. On the other hand, on the individual market, at least, WV only has three carriers and their requested rate changes for 2024 are in a very narrow range anyway (from flat to a 2.1% increase), so it doesn't matter much.

The good news is that West Virginia's individual market rates are only increasing by around 1% next year, one of the lowest avg. rate increases in the country.

The bad news is that West Virginia already has by far the highest unsubsidized individual market rates in the nation, at nearly $1,200 per month (second highest this year is Wyoming at $965/month).

In any event, small group market carriers are requesting an unweighted average increase of 9.6% overall.

UPDATE 11/08/23: State regulators increased the rate h ikes from 1.1% to 3.0% for CareSource, but otherwise left the other carriers on both markets as is.

As always, the Texas individual and small group markets are pretty messy. For starters, they have up to 20 individual market carriers depending on the year, along with over a dozen small group market carriers some years.

On top of that, as is also the case in some other states, some of the names of the insurance carriers can be confusing as hell. There's the "Insurance company of Scott & White" which seems to have changed its name to "Baylor Scott & White Insurance Co.," which isn't to be confused with "Scott & White Health Plans" and so on.

In addition, this year there seem to be a lot of carriers bailing on the Texas market altogether: Ambetter, Ascension and FirstCare appear to be pulling out of the states individual market, while Aetna (up to four different divisions?) along with Humana are leaving the small group market.

The bad news for Wyoming residents who earn too much to qualify for any federal ACA subsidies is that the state has the second highest unsubsidized premiums in the country after West Virginia. The good news is that, thanks to the Inflation Reduction Act, there are far more residents who do qualify for federal subsidies, which chop those premiums down to no more than 8.5% of their income.

The other good news for them is that for 2024, average premiums across the two insurance carriers which participate on the ACA exchange pretty much cancel each other out, with Blue Cross Blue Shield of Wyoming dropping their average premiums by 7% even as the Montana Health Co-Op seeks to raise theirs by 7.6%. Unfortunately, once again, I've been unable to get ahold of enrollment data for each carrier so this is an unweighted average only; if, say, 90% of enrollees are in Montana Co-Op plans, the weighted average would obviously be more like a 6% increase or whatever.

Pretty straightforward in the Mount Rushmore state. Three carriers on the individual market; around 48,000 enrollees total; requested rate changes ranging from a slight drop to a 5.9% increase. The weighted average across all three is +2.5%. No one new seems to be entering the market and none of the current ones are pulling out.

For the small group market, there are six carriers (again, no one new, no one dropping). The requested rate increases for these range from 2.5% to 10.3%, with a weighted average increase of 5.2% statewide.

Update 11/08/23:No changes to any of the preliminary filings on either market.

{kind=link}