New Mexico: TRICK OR TREAT! NM faces one more bit of CSR stupidity just ahead of Open Enrollment

Tue, 10/31/2017 - 6:56pm

UPDATE: It looks like this issue may be limited to a single carrier in New Mexico; I've changed the headline and graphic accordingly...but it might be an issue in other states as well; if so I may have to change it back again...

Fantastic (if migraine-inducing) scoop by Susannah Luthi of Inside Health Policy (paywall):

Insurers That Filed Wrong Rates Told By CMS They Can't Sell Plans Through Mid-November

An issuer whose final CMS-approved rates don’t account for the loss of cost-sharing reduction payments is being told by the agency that they won’t be able to sell plans until healthcare.gov data is refreshed– even though this would mean the carriers are even more crunched for time to sell their plans during the shortened open enrollment period.

Insurers are being told rates will be “suppressed and not able to be viewed or purchased” until that refresh is completed, officials said according to an email obtained by Inside Health Policy. Originally CCIIO told plans they would have to wait until the end of November for the refresh, but according to one source officials will move that date up to the middle of the month instead. But an agency official said these plans have no recourse. “CMS provided a limited data correction period this year to give issuers an opportunity to submit updates to final rate filings. Plans will not have additional recourse to change rate filings,” the official told IHP.

I really shouldn't quote any more of the story (especially since IHP is a paywall site), but depending on how this plays out, it could be ugly, especially if the problem is widespread. If I understand the article right, this is gonna confuse the hell out of people even more than they already are.

On the other hand...it could mean even more generous tax credits for some people...again, depending on the specifics.

For one thing, it sounds like for the first two weeks of Open Enrollment (November 1st through November 15th), the plans in question won't show up at all...and then they'll suddenly pop up on HC.gov starting on November 16th. I can't tell from the article whether this latest mess will apply to every state or only the 39 handled by the federal exchange, although Luthi says she thinks it's HC.gov only, for whatever that's worth.

So what is this gonna mean? Well...I'm not sure.

For one thing, it means that from 11/01 - 11/15, a bunch of people will shop around without seeing some options which will pop up on HC.gov after the 15th.

For another, it could play havoc with the benchmark plan pricing, which in turn could potentially make a mess out of the Advance Premium Tax Credit (APTC) subsidy formula.

For instance, let's say that the following Silver plans are available in a given market:

- Carrier A: $300

- Carrier B: $325

- Carrier C: $350

- Carrier D: $375

In this lineup, Carrier B is the 2nd lowest-cost Silver plan, so it's the benchmark plan, and everyone's subsidies in that rating area will be based on it.

However, what if Carrier B is one of the companies which had to scramble to refile at the last minute? What if the CSR-loaded premium for Carrier B's Silver plan is, say, $360?

In that case, Carrier C now has the 2nd lowest-cost Silver at $350...which means that everyone's subsidies is higher (preumably to the tune of $25/month or $300/year). Plus, anyone who was less than $300 over the 400% FPL APTC income threshold will suddenly be eligible after all...and that could mean up to several thousand dollars in savings!

OK, great...but is the benchmark plan during the first two weeks going to be based on the $325 rate or the $350 rate? The $325 plan isn't technically listed/available, so it technically isn't the "2nd lowest-cost Silver plan available"...but then what happens after 11/15? Does the benchmark plan stay at $350, or does it nudge up a bit more to $360? If so, that presumably means subsidized enrollees end up with another $10/month in APTC, or an extra $120 for the year, right?

For that matter, what if Carrier B only adds a small CSR load...instead of repricing their plan at $360, they price it at $340? Now it's still the 2nd lowest-priced Silver plan, and it's available after 11/15, meaning the APTC formula drops slightly (from $350 to $340), costing everyone $10/month.

Either way, what does that mean for someone who selects their exchange policy during the first two weeks? Will they receive the pre-11/15 APTC or the post-11/15 APTC amount?

To play it safe (hah!), it sounds like the best bet for most folks might be to wait until after 11/15 to enroll...but if you do that, that just means an even shorter time window and more traffic volume on the HC.gov server (which should be able to handle it) and the support lines (which may not?).

What a mess.

Oh, yeah, one more thing: According to Luthi, the insurance carriers themselves weren't even notified about this ahead of time; they didn't find out about it until they HC.gov launched window shopping a week ago. Apparently they, like everyone else, loaded HC.gov in their browser, started poking around only to discover that some of their own policies were missing.

Bravo, Trump Administration. Bravo.

ADDENDUM: Wesley Sanders adds a bit of context to this morass:

The confirmed one is Christus – their banner on the website confirms. At least some of their plans were the SLCSP https://t.co/PJ3Wo5GCYj

— Wesley Sanders (@wcsanders) October 31, 2017

Sure enough, if you visit CHRISTUS's website, right at the top:

ATTENTION CHRISTUS HEALTH USFHP AND CHRISTUS HEALTH PLAN MEMBERS:

Due to a technical error with CMS, CHRISTUS Health Plan’s Health Insurance Exchange plans in New Mexico may not currently appear on healthcare.gov. We are actively working with CMS to resolve the issue. If you have any questions, please feel free to contact the CHRISTUS Health Plan Customer Service Department at 844-282-3025.

I believe there are 4 carriers operating on the exchange in New Mexico: CHRISTUS, HCSC, Molina and New Mexico Health Connections.

So what happens if CHRISTUS originally had the benchmark plan? I have no idea.

Fortunately, every rating area in New Mexico has at least 3-4 carriers serving it...but what if there's a state/area where the "suppressed" carrier in question is the only one available there?

The mind boggles.

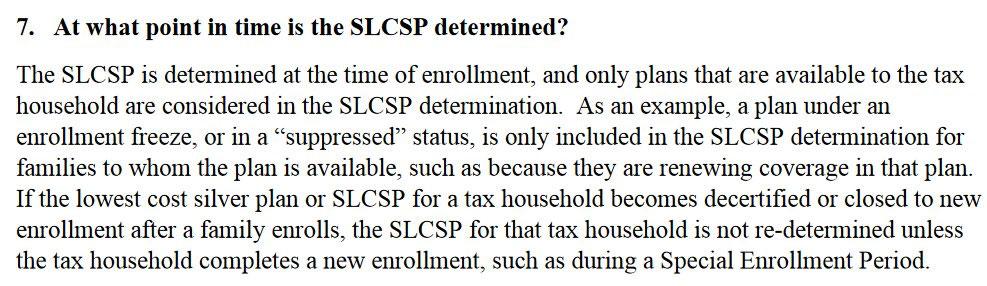

UPDATE: OK, healthcare economist Emily Gee of the Center for American Progress has at least one of the answers:

Here's the answer from an old FAQ. Suppressed plans considered as SLCS only for enrollees who are renewing. https://t.co/PZurzYdFWI pic.twitter.com/2Hh1SQFJt7

— Emily Gee (@EmilyG_DC) November 1, 2017

Advertisement