Iowa Code §505.19 requires the Commissioner to hold a public hearing on a proposed individual health insurance rate increase which exceeds the average annual health spending growth rate as published by the Centers for Medicare and Medicaid Services of the United State Department of Health and Human Services. For 2026 the growth rate is 5.6%.

The Iowa Insurance Commissioner will hold a public hearing regarding the relevant rate increases on August 19, 2025.

The purpose will be to hear public comments on the proposed increase in the base premium rate. Consumers wishing to make a public comment at the hearing are encouraged to attend the hearing via the live webcast.

All comments received will be considered public records and will be posted here. The Consumer Advocate will present the public comments received at the hearing.

Iowa has around 136,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~9,600 unsubsidized off-exchange enrollees.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

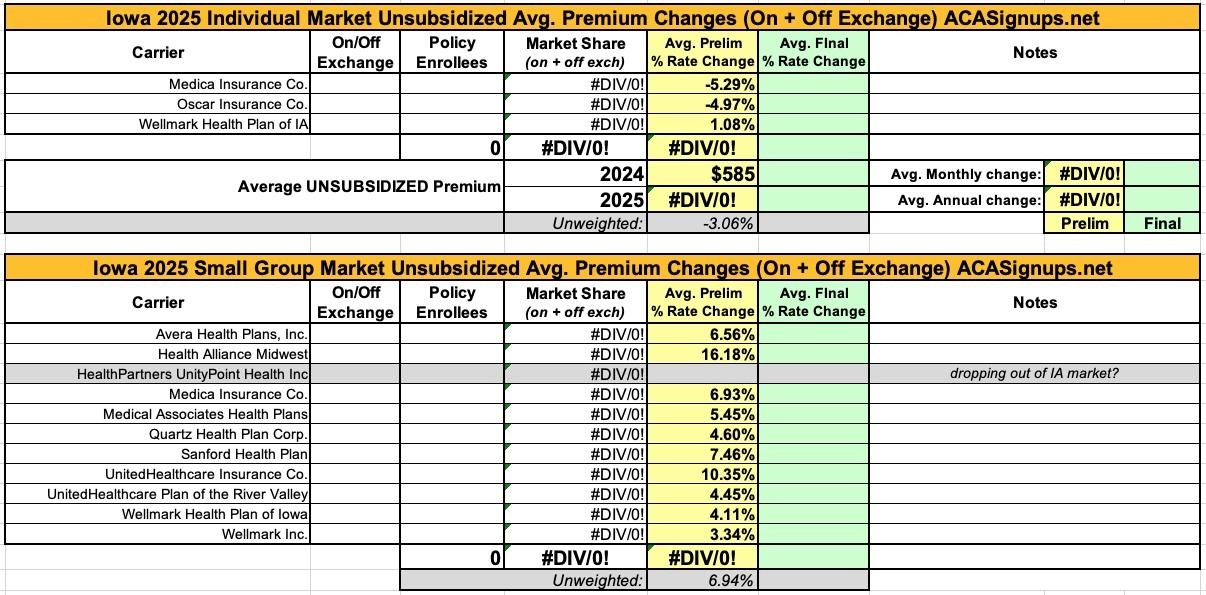

Here's the preliminary 2025 ACA individual and small group market rate filings. Unfortunately, the effectuated enrollment isn't available this year for the carriers in either market, so I can only offer unweighted averages...which include a 3.1% reduction on the indy market and a 6.9% increase for small group enrollees.

the only other noteworthy item is that it looks like HealthPartners UnityPoint is dropping out of Iowa's small group market next year...but with 9 other carriers participating there's still plenty of options for that population.

Back in November, I noted that Georgia, one of the ten states STILL refusing to expand Medicaid coverage to hundreds of thousands of low-income residents a decade after they could have done so under the ACA, may finally be coming around...albeit via a rather silly & inefficient method. via the Atlanta Journal-Constitution:

Could Georgia adopt an Arkansas-style Medicaid plan?

Senior Republicans see an opening for a health care overhaul

Key Republicans say they’re open to legislation that would add hundreds of thousands of poor Georgians to the state’s Medicaid rolls — and bring in billions of federal dollars to subsidize it — as part of a compromise to roll back hospital regulations.

Here's the preliminary 2024 rate filings for Iowa's individual & small-group markets. Unfortunately, I only have the enrollment data for the two smaller carriers on the individual market (and for only one carrier on the small group market). Oddly, while the Iowa Insurance Dept. has detailed rate filings for Medica and Oscar, it doesn't have one for Wellmark posted...and on the small group market, they only have publicly-available filing documentation for two of the eleven carriers.

Interestingly, CareSource Iowa, which only joined the state's individual market this year, appears to be dropping out of it again in 2024...or at least they don't have a listing showing up at RateReview.HealthCare.Gov as of this writing. Similarly, Aetna seems to be dropping out of the small group market as well.

In any event, based on my estimate of Iowa's total ACA-compliant individual market, I can make an educated guess as to the former's weighted average, which should be roughly a 5.7% drop in premiums.

The Children’s Health Insurance Program (CHIP) is offered through the Healthy and Well Kids in Iowa program, also known as Hawki. Iowa offers Hawki health coverage for uninsured children of working families.

No family pays more than $40 a month. Some families pay nothing at all. A child who qualifies for Hawki health insurance will get their health coverage through a Managed Care Organization (MCO).

Here's the preliminary 2023 rate filings for Iowa's individual & small-group markets. Unfortunately, I only have the enrollment data for the two smaller carriers on the individual market (and none for the small group market), but based on my estimate of Iowa's total ACA-compliant individual market, I can make an educated guess as to the weighted average, which should be roughly 2.0%.

Unfortunately I can't do the same for the small group market; for that, the unweighted average rate increase is around 5.1%.

I should also note that Iowa also has 35,400 residents still enrolled in pre-ACA ("transitional" or "grandmothered") medical policies, with nearly all of them being via Wellmark: