As shown below, things are pretty cut & dry in Rhode Island; they only have 2 carriers participating in the individual market (Blue Cross Blue Shield and Neighborhood Health Plan). BCBSRI is asking for a 10.7% average increase, while Neighborhood is requesting 8.7% overall.

The estimated market share ratios are based on this press release from HealthSourceRI, the state ACA exchange. That doesn't include the final numbers or the off-exchange enrollment, but it should be pretty close, as there are only 2 carriers and their requested increases are so close to begin with it wouldn't make much difference. The weighted average is 9.3%.

Last night I made a big fuss about New Jersey Governor Phil Murphy signing a restoration of the ACA's individual mandate penalty into law.

It turns out that the Governor of Vermont also signed the ACA mandate restoration bill I wrote about back in March into law a few days ago as well...but it's not as noteworthy, for several reasons. As Louise Norris reports over at healthinsurance.org:

Vermont governor signs legislation to implement an individual mandate starting in 2020; working group will sort out enforcement details

Establish a robust reinsurance program to significantly lower insurance premiums for individual market enrollees,

Protect people from out-of-network "balance billing", and

Cancel out Trump's expansion of "Association Health Plans"

In addition, New Jersey already outlawed "Short-Term Plans" (and "Surprise Billing") before the ACA was passed anyway.

Well, until today, there was some lingering doubt about the first two bills (which are connected...the reinsurance program would be partly funded by the revenue from the state-level mandate penalty), as Gov. Murphy was reportedly kind of iffy about signing them. As I understand it, he's been supportive of both ideas but is concerned about the potential budget hit in case the mandate penalty revenue doesn't raise enough to cover its share of the reinsurance program.

Apparently it still has to be kicked back to the state Assembly for a final vote, but it appears to be a done deal at last:

The Virginia Senate just passed Medicaid expansion, which three Republicans joining all 19 Democrats voting in favor. The House, which already passed expansion, has to vote again. We'll have more later, but here's the backstory. https://t.co/ldFEb5vYyt

Elections have consequences: To get enough GOP votes, this Medicaid expansion includes a work requirement and premiums above the poverty line, which will cut into coverage gains. Virginia must continue the fight.

I wrote about this back in April, but even I didn't think much of it at the time--I assumed it was more of a symbolic proposal than anything, or that it would die in committee at most. The details are important, of course, but assuming they make sense, this is exactly the sort of approach I would recommend in trying to gradually transition to some type of universal single-payer like system. The biggest questions I'd want answered are 1) What type of coverage does Medicaid actually have in Nevada? It varies widely from state to state, so if NV's is pretty comprehensive, awesome, but if it's skimpy, that's not very helpful; 2) What sort of premiums/deductibles/co-pays would buy-in enrollees be looking at?; 3) What sort of impact would this have on the state budget?; and most significantly, 4) How many Nevada doctors/hospitals would accept these enrollees? Remember, the reason a significant chunk of healthcare providers don't accept Medicaid patients is because it only reimburses them around 50¢ on the dollar compared to private insurance.

More than 95% of healthcare groups that have commented on President Trump’s effort to weaken Obama-era health insurance rules criticized or outright opposed the proposals, according to a Times review of thousands of official comment letters filed with federal agencies.

The extraordinary one-sided outpouring came from more than 300 patient and consumer advocates, physician and nurse organizations and trade groups representing hospitals, clinics and health insurers across the country, the review found.

This post actually has almost nothing whatsoever to do with the Affordable Care Act itself.

Every year I dig through hundreds (thousands?) of insurance premium rate filings for carriers in every state. For the most part I ignore everything except for my core focus area, the Individual Market, although on occasion I also try to run analysis of the Small Group market filings as well. I don't really pay much attention to the Large Group market filings.

However, there's a bunch of other types of health/medical insurance as well, and one which I've written next to nothing about since I started the ACA Signups project is also one which is becoming increasingly important as the Baby Boomer generation retires: Long-Term Care insurance.

To illustrate my point, here are a few recent premium rate increase filings from carriers in Connecticut:

A couple of months ago Louise Norris of healthinsurance.org gave me a heads up about a half-dozen or so healthcare bills, mostly ACA-related, pending in the California state legislature. Some were in the state Senate, some in the state Assembly; some were more along the lines of protecting the ACA from sabotage efforts while others were about expanding upon the law.

Well, today a whole bunch of those bills (as well as a few I didn't even know about earlier) made it a major step further along the line to becoming law. Courtesy of the Health Access CA Twitter feed:

BOISE — A Medicaid expansion proposal has passed the signature threshold, officials confirmed on Thursday, but said further review is neededbefore it gets on the November ballot.

Ada County Chief Deputy Clerk Phil McGrane says county clerks across the state have verified roughly 58,000 signatures that organizers submitted earlier this month.

The effort needed at least 56,192 signatures to qualify. However, those signatures must also come from 6 percent of the registered voters in at least 18 of Idaho’s 35 legislative districts.

McGrane says it’ll be up to the state to determine if the signatures meet the legislative district requirements.

Reclaim Idaho, the group that organized the Medicaid expansion effort, did not immediately return a request for comment.

So far, only 4 states have released their preliminary 2019 ACA-compliant individual market premium rate filings: Maryland, Virginia, Vermont and Oregon.

However, it's a bit overly cumbersome for my purposes: It stretches out over 6 full pages, and includes columns for Standalone Dental Plans as well as a bunch of info regarding the Small Group Market. I did used to try tracking Small Group rates as well, but that got to be too difficult to keep up with, and I haven't really done much analysis of standalone dental plans at all. Let's face it: About 90% of the drama, controversy and confusion regarding ACA premiums is all about the individual market.

California is exploring a bold and controversial new plan to rein in health care spending by letting the state government set medical prices.

...Still, California’s new proposal is worth examining as one that steps closer to single-payer — but doesn’t go quite all the way. It’s one plausible step a state could take without any assistance from the Trump administration, as we see more blue states looking for ways to shape the future of their own health care systems.

”I think we have appreciated how much we’ve been able to do with transparency and data, and how much we’ve been able to collect, but we reached the point where we felt like we had to tackle the issue of prices head on,” says Sara Flocks, policy coordinator for the California Labor Federation, which is backing the proposal.

20 states went the full #SilverSwitcharoo route (the best option, since it maximizes tax credits for those eligible for them while minimizing the number of unsubsidized enrollees who get hit with the extra CSR load);

16 states went with partial #SilverLoading (the second best option: Subsidized enrollees get bonus assistance, though not as much as in Switch states; more unsubsidized enrollees take the hit, but they aren't hit quite as hard);

6 states went with "Broad Loading", the worst option because everyone gets hit with at least part of the CSR load except for subsidized Silver enrollees;

6 states took a "Mixed" strategy...which is to say, no particular strategy whatsover. The state insurance dept. left it up to each carrier to decide how to handle the CSR issue, and ended up with a hodge podge of the other three

3 states (well, 2 states + DC, anyway) didn't allow CSR costs to be loaded at all. Their carriers have to eat the loss, which makes little sense, but what're ya gonna do?

For a couple of months now, I've been attempting to track a slew of state-based "ACA 2.0" bills slowly winding their way through various state legislatures. However, this is really a bit of a misnomer, since some of these bills aren't so much about expanding the ACA as they are about protecting it from various types of undermining or sabotage from the Trump Administration and Congressional Republicans.

Once again: The "Blue Leg" of the Stool covers everything which ACA-compliant individual health insurance carriers are required to include: Guaranteed Issue, Community Rating, 10 Essential Health Benefits, a Minimum 60% Actuarial Value rating, no Annual or Lifetime Caps on coverage, and a long list of mandatory Preventative Services at no out-of-pocket cost when done in-network.

Commencement speakers will remind thousands of new graduates that “life can change in an instant” – making it important for them to have health coverage, so they can get the health care they need as they set out in life.

A new video distributed on social platforms will remind graduates who may be losing their health coverage to check out Covered California for affordable options.

Covered California Executive Director Peter Lee congratulates graduates and reminds them to protect their futures by getting health insurance.

Covered California provided more than 70 campus health centers with materials to educate graduating students about new health insurance options available through Covered California

The “special enrollment” campaign for graduates is launching amid new data showing California’s uninsured rate is at an all-time low.

SACRAMENTO, Calif. — Graduation season is in full bloom and Covered California is joining with commencement speakers throughout the state to remind the over 400,000 graduates and their families not to forget about the importance of health insurance during this busy time of year.

Eleven health insurers file for 2019 individual market: No bare counties

May 25, 2018

OLYMPIA, Wash. – Eleven health insurers filed 88 health plans for Washington state’s individual market yesterday, and all 39 counties will be covered in 2019.

The proposed rate changes are not public until 10 days after the OIC has determined the filings are complete. Release of the proposed rate changes is targeted for June 4.

“We can all breathe a sigh of relief knowing consumers in every county who need coverage will have access to a health plan in 2019,” said Insurance Commissioner Mike Kreidler. “Obviously, how much premiums may change and any increases to out-of-pocket costs are still key concerns, but I’m grateful that we can assure people that coverage is available, regardless of where they live.”

Establish a robust reinsurance program to significantly lower insurance premiums for individual market enrollees,

Protect people from out-of-network "balance billing", and

Cancel out Trump's expansion of "Association Health Plans"

(New Jersey actually already had several other "ACA protection" laws on the books in the first place, including protections against short-term plans and "surprise billing".)

In addition, new Governor Phil Murphy had alread proven that he understands and supports the ACA; within days of taking office he had already issued an executive order telling all state agencies to do everything they reasonably can to inform the public about how to enroll during Open Enrollment and so forth.

On another note, I also want to use this as an opportunity to point out that maintaining quality health insurance coverage needs to be a priority year in and year out. Jenks notes that "Pregnancies are often unplanned, making limited enrollment periods impractical for many women." But can't that be said of any medical condition? In fact, I would say pregnancy is one aspect of healthcare that's probably much more likely to actually be planned. While about half of pregnancies are planned, I doubt the same could be said for cancers, heart attacks, or car accidents.

In other words, while not all pregnancies are planned, overall it's a lot less "random" than most other expensive healthcare incidents.

Sen. Mike SHIRKEY (R-ClarkLake) said today he's hammered out an agreement with the administration and the House on creating work requirements for Medicaid recipients.

Speaking during a taping of "Off The Record," Shirkey said, "We have a deal." All sides have signed off on the exemptions to the work requirement, but he didn't get into all fo them pending a formal announcement coming as soon as later this week.

From the wording of this, it sounds an awful lot like "all sides" appears to refer to Republican Senator Shirkey, the rest of the Republican State Senate, the Republican State House and the Republican Governor.

Shirkey confirmed that the 29-hour job requirement in the Senate bill has been pared back to 20 to which he says, "I was hoping Michigan could take a leadership position and set a new standard for that." But rather than jeopardize the entire package, he compromised.

Kris Haltmeyer, a vice president at the Blue Cross Blue Shield Association, told reporters that the premium increases were in part due to the repeal of ObamaCare’s individual mandate in the Republican tax reform bill in December...“With the repeal of the individual mandate and the failure of Congress to enact stabilization legislation, we are expecting premiums to go up substantially,” Haltmeyer said.

...He said the premium increases are “related to the loss of the mandate and then underlying medical costs.”

“Those two things have the most impact on the rate increases,” he added.

...Oh, and what comes after mandate repeal and underlying medical costs? You guessed it: #ShortAssPlans

One of the things Ford had always found hardest to understand about humans was their habit of continually stating and repeating the very very obvious, as in ‘It’s a nice day’, 'You’re very tall’, or 'You seem to have fallen down a thirty-foot well, are you alright?’

--Douglas Adams, The Hitchhiker's Guide to the Galaxy

A top insurance industry official said Wednesday that he expects “substantial” ObamaCare premium increases for 2019.

Kris Haltmeyer, a vice president at the Blue Cross Blue Shield Association, told reporters that the premium increases were in part due to the repeal of ObamaCare’s individual mandate in the Republican tax reform bill in December. He also cited lawmakers’ failure to pass a bill aimed at lowering premiums, which fell apart earlier this year amid a partisan dispute over abortion restrictions.

It's become a tradition that every spring/summer/fall, I pore over the official SERFF database for every state, furiously searching for the ACA-compliant rate filings for the upcoming year.

The thing is, the SERFF database, in addition to being somewhat confusing and clunky to work with, includes a lot more than just "here's how much we want to raise our rates next year". Even after narrowing it down to just major medical health insurance policies, there are often still dozens of different forms and spreadsheets in the database, covering pretty much any change to any insurance policy for any carrier. If a carrier drops out of a market, there are forms. If they stop offering PPOs, there are forms. If they merge with or buy out another company, there are obviously forms. Even for the rate filings themselves, there are often a dozen or more different PDFs and/or spreadsheets included as supporting documentation.

The stage is set for a showdown in the Virginia Senate on Tuesday over a budget compromise negotiated by Senate Finance Co-Chairman Emmett Hanger, R-Augusta, and House Appropriations Chairman Chris Jones, R-Suffolk, to expand the state’s Medicaid program and pay for the state’s share through a new tax on hospital revenues that also would boost Medicaid payments for inpatient provider care.

This evening brought three major pieces of ACA-related news out of three different states:

First, in California, the State Senate passed SB-910, which wouldn't just limit short-term plans, but would outright prohibit them altogether. To my knowledge, CA would be the only state* where STPs wouldn't be allowed at all:

(*Correction: It turns out that New York, New Jersey and Massachusetts also ban Short-Term Plans as well, although according to Dania Palanker of the Center on Health Insurance Reforms at Georgetown University, California would be the first state to explicitly outlaw short-term plans as opposed to simply stating that all policies have to meet certain standards.)

SACRAMENTO – Today, the State Senate approved passage of Senate Bill 910, which prohibits the sale of short term limited duration health insurance in California.

The stage is set for a showdown in the Virginia Senate on Tuesday over a budget compromise negotiated by Senate Finance Co-Chairman Emmett Hanger, R-Augusta, and House Appropriations Chairman Chris Jones, R-Suffolk, to expand the state’s Medicaid program and pay for the state’s share through a new tax on hospital revenues that also would boost Medicaid payments for inpatient provider care.

(The article goes into all the other non-Medicaid related stuff in the budget as well, of course, although some of it is obviously healthcare-related.)

*(To be honest, all of these types of bills--work requirements for Medicaid, drug testing for welfare benefits, photo ID for voting--have at least a tinge of racism to them no matter what, but at least this one isn't blatantly racist anymore).

LANSING, Mich. (AP) — The sponsor of proposed Medicaid work requirements said Monday that lawmakers are removing a provision to exempt recipients who live in Michigan counties with high unemployment, saying it would have been too difficult to administer and denying allegations of racism.

Republican Sen. Mike Shirkey of Clarklake also told The Associated Press that the proposed 29-hour-a week workforce engagement requirement for able-bodied adults is being lowered to “very close” to 20 weeks. That is in line with the three states that have enacted Medicaid work laws and with Michigan’s work requirement for food assistance beneficiaries.

Having a doctor holding elected office is kind of hit or miss (former HHS Secretary Tom "Fly Me!" Price was an orthopedic surgeon, for instance, while Rand "Kneel before Aqua Buddha!" Paul is supposedly a "self-certified" opthamologist), but once in awhile it can be a very good thing.

Case in point: Ralph Northam, the new Governor of Virginia, a former Army doctor and pediatric neurologist, who just formally vetoed not one, not two, but four different GOP-passed healthcare bills, each of which would have further weakened and damaged the ACA individual market risk pool:

RICHMOND—Governor Ralph Northam today vetoed Senate Bills 844, 934, 935, and 964, which would put Virginians at risk of being underinsured, result in rapidly increasing Marketplace premiums, and undermine key protections in the Affordable Care Act. Governor Northam remains committed to expanding health care for nearly 400,000 uninsured Virginians, return millions to the state budget, and reduce Marketplace premiums. The Governor’s full veto statements are below.

I've written quite a few entries bashing the Short-Term Plan portion of Donald Trump's executive order opening up the floodgates on non-ACA compliant policies. However, I've written far less about the other shoe he's dropping: Association Health Plans, or AHPs. In fact, while I discussed AHPs briefly in Part Two of my Risk Pool video, the only blog post I've written to date which specifically focuses on them just quoted from this Avalere Health article:

Association Health Plans (AHPs) are health insurance arrangements sponsored by an industry, trade, or professional association that provide health coverage to their members—typically small businesses and their employees. Health insurance coverage offered through AHPs aims to make coverage available and affordable for small groups and individual employees. Importantly, these arrangements are currently governed by state and federal requirements and are subject to state oversight, including standards related to premiums and benefit requirements.

Polls in 6 Battleground States Show Voters Blame Republicans for Rate Hikes

Six new Public Policy Polling surveys in battleground states find voters will blame Republicans for the expected health care premium increases this summer by approximately 30 points and voters believe Republicans and President Trump have been actively undermining and sabotaging the Affordable Care Act.

ARIZONA Voters say they will blame Republicans if health care premiums increase this summer. 55% say they will hold Republicans in Washington responsible if rates increase, compared to just 29% who said they would not. A plurality of voters (49%) say they believe Washington Republicans and President Trump have been trying to undermine and sabotage the Affordable Care Act – and a majority of independent voters (57%) also say they agree with that statement.

OK, this doesn't technically count as an official 2019 Rate Hike analysis since none of it comes from actual carrier rate filings, but Covered California, the largest state-based ACA exchange, just released their proposed 2018-2019 annual budget, and it includes detailed projections regarding expected premium increases and enrollment impact over the next few years due specifically to the GOP's repeal of the ACA's Individual Mandate. Oddly, while they mention short-term plan expansion as another potential threat to enrollment/premiums, they do so passingly, and they don't mention association plans at all:

Since 2014, nearly 5 million people have enrolled in Medi-Cal due to the Affordable Care Act expansion, and more than 3.5 million have been insured for some period of time through Covered California. Together, the gains cut the rate of the uninsured in California from 17 percent in 2013 to a historic low of 6.8 percent as of June 2017.

Last month, after much painstaking research and analysis, I concluded that unsubsidized ACA-compliant individual market enrollees (both on & off the exchanges) are paying an average of around $960 this year (~$80/month) more in healthcare premiums nationally in 2018 than they otherwise would be if not for the various forms of ACA sabotage carried out by Donald Trump and Congressional Republicans last year.

Again, it's important to clarify that this is $960 more (around 17% more) in addition to non-sabotage-related factors such as normal medical expense inflation (around 7%), the reinstatement of the ACA carrier tax (about 2%) and other various/sundry factors (around 2%).

Back in mid-April, I crunched a bunch of numbers and concluded that around 6.5 million people enrolled in unsubsidized ACA-compliant individual market policies are, on average, paying an additional $960/year ($80/month) for their policies this year due specifically to last year's sabotage efforts by Donald Trump and Congressional Republicans. This is separate from other factors such as medical trend and the reinstatement of the ACA carrier tax. The actual 2018 "Trump Tax" ranges from as little as almost nothing at all in Vermont and North Dakota to as high as $1,500 per enrollee in Mississippi and Pennsylvania.

The 2018 sabotage impact was mainly due to 1) CSR reimbursement funding being cut off; 2) uncertainty over individual mandate enforcement; and 3) a mish-mash of Open Enrollment changes including cutting the time window in half, slashing marketing/assistance budgets by 90% and 40% respectively and so forth.

I suspect that even within the healthcare wonk community, this particular bit of information is only going to be of interest to a small number...but I'm one of them, and it's my site, so there you go.

The Kaiser Family Foundation just released an important new study which proves everything I've been saying for the past year and a half: After years of turmoil, the ACA-compliant individual market had finally quieted down and reached equilibrium last year...right up until Donald Trump, combined with total GOP control of the federal government, deliberately came in like a wrecking ball and messed everything up again:

Concerns about the stability of the individual insurance market under the Affordable Care Act (ACA) have been raised in the past year following exits of several insurers from the exchange markets for 2017, and again last year during the debate over repeal of the health law.

This post was inspired by a Twitter query by "Other Alex". He originally asked about the insanely expensive premiums for ACA policies in Charlottesville, Virginia, which I wrote about the other day. Anyway, after some back & forth between him, myself and Colin Baillio, Alex asked if I knew where the least-expensive ACA plans are.

I haven't looked it up by rating area yet (for instance, Virginia as a whole ranks 18th most expensive this year even though Charlottesville is the most expensive rating area in the country), but on a state-level basis, it appears that the least expensive state for ACA-compliant individual healthcare policies is actually...(drumroll please)...

A couple of weeks ago, Donald Trump's former HHS Secretary Tom Price openly (and rather casually) admitted at the World Health Care Conference that the GOP's repeal of the ACA's individual mandate will "harm the pool in the exchange markets & drive up costs" when it actually goes into effect in 2019.

WASHINGTON — President Trump’s plan to expand access to skimpy short-term health insurance policies, as an alternative to the Affordable Care Act, would affect more people and cost the government more money than the administration estimated, an independent federal study says.

Oregon just became the 4th state to submit their preliminary 2019 ACA individual market rate filings, and while the expected increase is smaller than expected on average (in part due to Oregon's strict control of short-term plans), repeal of the individual mandate by Congressional Republicans and Donald Trump are still responsible for the vast majority of the rate increase.

Normally, I don't start posting natoinal projections for my annual Rate Hike Project until I have at least filing data for at least a dozen or so states because the national weighted average jumps around so much early on. A "national average" of, say, 10% based on numbers from, say, Vermont, Wyoming and the District of Columbia (collective population: 1.9 million people) is gonna change radically once you add California or Florida to the mix if they're looking at a 20% hike, for example.

Having said that, seeing how advocacy organization Protect Our Care has decided to launch their own version of my Rate Hike Project, and seeing how I do have preliminary 2019 rate increase projections from at one large state (Virginia) and two mid-sized states (Maryland and Oregon), I've decided to go ahead and start posting the national projections early, with a major caveat that the national average will likely change dramatically until at least 2/3 of the states have been plugged in.

For three years now, I've been painstakingly tracking the annual average rate increases for ACA-compliant individual market policies across all 50 states (+DC) and nationally, including both the on & off-exchange markets in as much detail as possible, and at the risk of tooting my own horn too much, my track record on this has been pretty damned accurate:

Implications Of CMS Mandating A Broad Load Of CSR Costs

In October 2017, the Trump administration eliminated federal funding to reimburse insurers for cost-sharing reduction (CSR) subsidies, which they are obligated to provide to qualifying enrollees in the Affordable Care Act (ACA) Marketplace. President Donald Trump had threatened to eliminate CSR funding throughout 2017, so insurers and insurance regulators in many states had anticipated the move by adding the cost of CSRs to premiums for 2018.

Given how progressive Vermont is, you'd think that they'd be doing as much as possible to batten down the hatches in order to avoid or mitigate the latest wave of sabotage efforts from the Trump Administration and the GOP...and you'd mostly be correct.

Some of the work on that front has already been done. For one thing, Vermont (along with Massachusetts and the District of Columbia) merges their individual and small group market risk pools together, which helps smooth out premium increases and overall morbidity across a larger risk pool. For another, Vermont has fully embraced ACA provisions such as Medicaid expansion and operating their own full exchange, of course. Vermont, along with a few other states, also has pretty strict rules in place limiting both short-term and association healthcare plans, so that portion of Trump's sabotage attack is neatly cancelled out already.

It's very clear that the name of the game for healthcare policy this year seems to be "What comes after the ACA?"

For over a year now, I've been strongly urging the passage of some sort of "ACA 2.0" upgrade package, primarily based on my own wish list entitled "If I Ran the Zoo", a collection of about 20 assorted ACA fixes. The reality is that a couple of the items on my list start to move away from an "upgraded ACA" and drift over into what I've mentally compartmentalized as the next phase in achieving Universal Healthcare Coverage.

Since I first posted my wish list just over a year ago, several new proposals have been released by various Democratic politicians and 3rd-party organizations such as the Center for American Progress, some of which are revised versions of other long-proposed systems. These include:

A week or so ago, I noted that Republicans in my home state of Michigan have come up with a clever way of having their (chocolate) cake and eating the (vanilla) cake too. As first noted by Nancy Kaffer of the Detroit Free Press:

Although HB 897 threatens to end Medicaid benefits for hundreds of thousands living elsewhere in the state, it includes exemptions for people who live in counties with an unemployment rate of more than 8.5%, like the ones Schmidt represents.

Live in Detroit? You're out of luck.

The city's unemployment rate is higher than 8.5%, but the unemployment rate in surrounding Wayne County is just 5.5% — meaning Detroiters living in poverty, with a dysfunctional transit system that makes it harder to reach good-paying jobs, won't qualify for that exemption. The same is true in Flint and the state's other struggling cities.

As of today, there are 12 states which operate their own full ACA exchanges, including their own board of directors, marketing budget, bylaws and tech platform for their enrollment website. 34 states have offloaded just about all of that to the federal exchange, HealthCare.Gov. And then there are five states which are in between: They have their own state-based exchange...but their tech platform is basically piggybacked onto the federal exchange: Arkansas, Kentucky, Nevada, New Mexico and Oregon.

Arkansas and New Mexico always planned on moving off of HC.gov onto their own full exchange platform but never got around to doing so. Kentucky's ("kynect") was working perfectly well from day one, and only made the move to the federal platform after three years because new GOP Governor Matt Bevin decided he didn't like it for whatever reason. New Mexico and Oregon, meanwhile, had such major technical problems at launch that they scrapped their sites after the first year and moved to the Mothership. (As an aside, Hawaii also scrapped their exchange site after the second or third year, but they shut down their entire state-based exchange and moved everything to HC.gov).

Northam signs healthcare bill to provide relief to Virginia entrepreneurs

Published Wednesday, Apr. 11, 2018, 12:42 pm

Gov. Ralph Northam signed a new healthcare bill into law that will provide relief to many small business owners currently struggling with the Central Virginia insurance premium crisis.

Members of local advocacy group Charlottesville For Reasonable Health Insurance had provided testimony at the Virginia General Assembly and organized an email campaign, helping to ensure passage of the bill through the legislative session. Introduced by Sen. Creigh Deeds and effective July 1 2018, SB672 will allow self-employed people to take advantage of the much more affordable health plans in the small group business marketplace, without having to hire employees.

The Basic Health Program is one of the more obscure provisions of the Affordable Care Act. Very few people outside of the healthcare wonk community know anything about it...unless they live in Minnesota or New York State.

The short version is that it's an optional low-income healthcare program designed for people at the income tier just above Medicaid expansion...138% - 200% of the Federal Poverty Line, or between around $16,600 - $24,100/year for a single adult. In most states people in that income range would be expected to enroll in heavily-subsidized ACA exchange policies. In New York and Minnesota, however, they've instead set up Basic Health Programs (BHPs) for this population instead.

*(No, they aren't paying me anything, and I have no idea whether they're a good or bad company to do business with. I do know they do a reasonable amount of business and they cover most of the country, so their findings are likely reasonably representative).

The lede pretty much says it all:

A new survey by eHealth, Inc. finds that individual and family health insurance consumers are cost-stressed, confused about the state of the Affordable Care Act (ACA) and worried about the future of their benefits. They believe that all health plans should provide rich benefits, but they’re unwilling to shoulder the costs often associated with those benefits. They’re bringing their frustrations over the state of health care to the ballot box in 2018.

Louise Norris is an awesome source for all sorts of healthcare policy/insurance data, but she's especially on top of developments in her home state of Colorado, where she and her husband Jay run a small brokerage outlet.

Today Jay and Louise have a couple of interesting tidbits out of The Centennial State (yeah, I had to look up their nickname myself).

That's (sort of) an 88% retention rate through early May. I say "sort of" because this presumably includes some amount of churn (if 100 people drop coverage and 100 off-season enrollees sign up, that'd be a net change of zero). Even so, it's actually slightly better compared to prior years, when the national effectuation number had usually dropped to around 87% by the end of March.

In Part 2, I go into more detail about the different types of NON-ACA plans available on the individual market, why they mostly stink, and how the repeal of the Individual Mandate Penalty, especially when combined with Trump's yanking away restrictions on "short-term" and "association" plans, will take an existing problem and make it far worse.

Oh, yeah: It involves Dabney Coleman and Morgan Freeman.

Senate uses salary threat to push Medicaid work plan

Lansing — Michigan’s Republican-led Senate is pressuring Gov. Rick Snyder to back sweeping changes to the state’s Medicaid health insurance system, including proposed work requirements and a tougher 48-month benefit limit for the Healthy Michigan plan.

I've trashed CMS Administrator Seema Verma many times for her callous and backward-logic driven push to impose pointless, counterproductive work requirements on ACA Medicaid expansion enrollees. However, it appears that even she has her limits when it comes to treating people terribly:

The Trump administration has drawn a red line on Medicaid cuts. There are some proposals that the Centers for Medicare and Medicaid Services won’t approve.

In a letter on Monday, CMS Administrator Seema Verma told Kansas officials that her agency would not approve the state’s request to impose lifetime limits, which would have capped a person’s eligibility at three years, after which they could no longer be covered by the program.

Verma noted that the administration had approved proposals by other states to cut off benefits for Medicaid enrollees only if they fail to meet certain work requirements.

President Trump is sending a plan to Congress that calls for stripping more than $15 billion in previously approved spending, with the hope that it will temper conservative angst over ballooning budget deficits.

Almost half of the proposed cuts would come from two accounts within the Children’s Health Insurance Program (CHIP) that White House officials said expired last year or are not expected to be drawn upon. An additional $800 million in cuts would come from money created by the Affordable Care Act in 2010 to test innovative payment and service delivery models.

Those are just a handful of the more than 30 programs the White House is proposing to Congress for “rescission,” a process of culling back money that was previously authorized. Once the White House sends the request to Congress, lawmakers have 45 days to vote on the plan or a scaled-back version of it through a simple majority vote.

Insurers selling Obamacare plans in Maryland are again seeking huge rate increases for 2019, but they could be knocked down significantly by a reinsurance program the state hopes to implement for next year.

CareFirst BlueCross BlueShield wants to increase rates on average by 18.5 percent on its HMO plans, which account for more than half of the individual market this year.Kaiser Permanente, the only other insurer selling on the exchange, is seeking a 37.4 percent average increase on its HMO plans, which cover just over a third of Obamacare customers.

A couple of days ago, I posted that Virginia has become the first state out of the gate with their preliminary 2019 premium rate requests for ACA individual policies. However, I made sure to emphasize that these are preliminary requests only; carriers often resubmit their rate change requests more than once over the course of the summer/fall, and even that may not match whatever the final, approved rate changes are by the state insurance commissioner.

In addition, I generally try to make it understood that there's alotof room for error here--the weighted averages are based on the number of current enrollees, but of course that number can change from month to month as people drop policies or sign up during the off-season (via Special Enrollment Periods). Even then, the rate filing paperwork is often vague or confusing about just how many enrollees they actually have in these plans. Sometimes wonks are reduced to taking the number of "member months" and dividing by 12 to get a rough idea of how many people are enrolled in any given month. Sometimes the only number of enrollees available are from last year, which could bear zero resemblence to how many are currently enrolled. Sometimes the only number available is how many people the carrier expects to enroll in their policies next year. And so on.

Aside from Virginia, it's likely going to be another month or so before the 2019 ACA policy rate filings start trickling in, since the deadline for initial rate requests isn't until late June in most states. However, there's some interesting non-ACA policy filing stuff which is available as well. Given all the concern about non-ACA compliant policies siphoning healthy people away from the ACA market, I figured I should take a look at a few of these.

Here in Michigan, I've found three such filings: One is for "transitional" plans from Golden Rule (a subsidiary of Unitedhealthcare, I believe). The other two are for "short-term" plans (the type which Donald Trump is basically removing any regulation on).

IMORTANT UPDATE: As I suspected, it turns out that the stray rate filing posted to the California Insurance Dept. website a few days ago was posted prematurely, doesn't reflect the carrier's final* rate filing, and has since been pulled from the California Insurance Dept. website.

I've been asked to remove the filing data, and seeing how there's nothing nefarious about it (I wasn't "whistleblowing" evidence of anything criminal/unethical), I'm complying with that request. Since everything in the post related to that data, there wasn't much point in keeping the rest of it either.

*(Yes, I'm aware that none of these early filings are "final" since they tend to be revised/resubmitted throughout the summer/fall, but you know what I mean.)

...and to absolutely no one's surprise, GOP sabotage of the ACA will be directly responsible for a significant chunk of the individual market premium increases.

Every year for 3 years running, I've spent the entire spring/summer/early fall painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are going to increase (or, in a few rare instances, actually decrease).

The actual work is difficult due to the ever-changing landscape as carriers jump in and out of the market, their tendency repeatedly revise their requests, and the confusing blizzard of actual filing forms which sometimes make it easy to find the specific data I need and sometimes make it next to impossible.

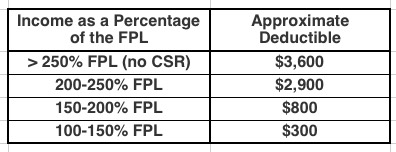

The Affordable Care Act (ACA), in section 1402, requires insurers who participate in the marketplaces established under that act to offer CSRs to eligible people who purchase silver plans through the marketplaces. CBO views that requirement as establishing an entitlement for thoseeligible.

To qualify for CSRs, people must purchase a plan through a marketplace and generally have income between 100 percent and 250 percent of the federal poverty guidelines (also known as the federal poverty level, or FPL). The size of the subsidy varies with income.

CSRs reduce deductibles and other out-of-pocket expenses like copayments. For example, in 2017, by CBOs estimates, the average deductible for a single policyholder (for medical and drug expenses combined) with a silver plan varied according to income in the followingway:

I've written quite a bit about the attempt by the GOP-controlled state legislature to push through work requirements for ACA Medicaid expansion here in Michigan. The bill (SB897) was quickly passed on partisan lines in the state Senate last week, and has now been taken up by the appropriations committee in the state House.

I actually shlepped my butt all the way out to Lansing yesterday morning to attend the committee hearing. Unfortunately, there were so many others who wanted to speak during the Public Comment period, I didn't get a chance to chime in.

As noted a few days ago, I've posted Part One of my latest crudely-produced-but-hopefully-informative video explainer.

The first part gives an overview of how healthcare Risk Pools actually work and why quarantining sick people into a separate High Risk Pool is such a terrible idea.

The second part, which I hope to post in the next few days, will go into why Donald Trump's recent Short-Term/Association Plan executive order will make a problem which already existed in 2017, and which was made worse by the GOP (by design) in 2018, even worse starting in 2019.

NOTE: Just to clarify, here's where the headline comes from:

...Sponsoring Sen. Mike Shirkey, R-Clarklake, created exemptions in the Michigan legislation that would waive the work requirement for parents with young children, pregnant women or caretakers for disabled family members. But asked about people like Maitre who could still lose health care, he told reporters the social safety net “by definition, has a lot of holes in it.”

“The best safety net ever invented by God is family,” Shirkey said, “but I’m not sure that government is supposed to supplement that process.”

Well, here we go:

#BREAKINGtomorrow morning the House Appropriations Committee is taking up SB 897. Another Republican attempt to take away healthcare from Michigan familieshttps://t.co/WsUhyntINj

Virginia’s Republican-led legislature is on the verge of doing something that would’ve been almost unthinkable just a year ago: approving legislation that would use money from the Affordable Care Act to expand Medicaid to as many as 400,000 people.

That coverage expansion would come at a price for Democratic legislators, progressive activists and low-income Virginians, however. Any Medicaid expansion bill that makes it out of the General Assembly will carry with it new work requirements for Medicaid enrollees, a priority for the GOP at large and for President Donald Trump’s administration.

Democrats in the Virginia legislature have tried in vain for six years to persuade their GOP counterparts that accepting federal dollars to extend Medicaid coverage to poor adults is the right thing to do. Accepting a work-requirements policy that would create bureaucratic obstacles to eligible Virginians appears to be the compromise needed to win the bigger fight.

HELENA — There are 91,563 Montanans participating in the Medicaid expansion HELP act as of Jan. 15, generating nearly $40 million in savings in Medicaid benefits, a state panel was told Thursday.

Members of the Legislature’s Children, Families, Health and Human Services Interim Committee reviewed a report on Medicaid expansion. The committee took no immediate action after hearing the report.

As noted earlier, I've been a bit lax with posting for a few days as I've worked on my latest 2-part video explainer about risk pools and #ShortAssPlans.

However, there's been a lot going on, so I figured I should try and at least do a quick update on a few items. First up: Medicaid expansion!

Here in my home state of Michigan, I've written several posts about how the GOP-controlled state legislature trying to shove through a draconian "work requirement" bill for Healthy Michigan, our name for ACA Medicaid expansion program which has been working just fine, thank you very much, for nearly 5 years now. The bill easily passed the state Senate (where the GOP holds a supermajority), and is now under consideration by the state House (where they have a smaller but still solid majority at the moment). The good news is that GOP Governor Rick Snyder--who championed passage of Healthy Michigan in the first place and seems to think it's fine mostly the way it is--is likely to veto the senate version of the bill. The bad news is that it might simply be tweaked somewhat by the House.

Price says that he's not a big fan of the GOP tax bill's 2019 individual mandate repeal-- says it will harm the pool in the exchange markets & drive up costs

Making my eyeballs roll even further back in my head, here's what Price said just nine months ago (shortly before he was given the boot from the HHS Dept.):