The average rate increase included in this filing is 19.3%, affecting over 210,000 members.

The main factors driving the need for this increase are:

Alabama market membership loss and remaining members projected to be less healthy following expiration of enhanced premium subsidies in place since 2021

Projected claim cost trends are higher for 2025 than anticipated in the 2025 filing and are projected to continue into 2026

Administrative costs increased in 2025 and are expected to rise further in 2026 due to new eligibility and billing rules, along with a higher Exchange User Fee

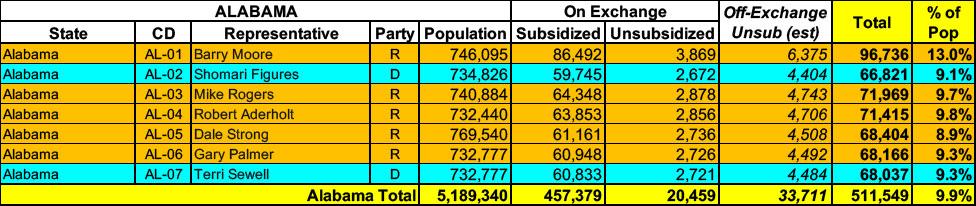

Alabama has around 477,000 residents enrolled in ACA exchange plans, 96% of whom are currently subsidized. I estimate they also have perhaps another ~33,000 unsubsidized off-exchange enrollees.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

The good news is that RateReview.HealthCare.Gov has posted the preliminary 2025 rate filing summaries for every state, making it much easier to pin down which carriers are actually participating in the individual & small group markets next year, as well as what the carriers average requested rate changes are in states which don't publish that data publicly (or which make it difficult to track down if they do).

The bad news is that in many of those states, acquiring the actual enrollment data is even more difficult, as their rate filings tend to be heavily redacted.

I strongly suspect that at least one of the remaining holdout states will join the expansion crowd this year, most likely Georgia, Mississippi or Alabama...but it likely will be some state-specific variant as described above. Stay tuned...

...As I noted, however, in all three [states] it's pretty likely they'll go with at least a partially privatized version as Arkansas has instead of a "clean" expansion of Medicaid proper.

February 28th:

BREAKING: The Mississippi House just passed Medicaid expansion by a 96-20 vote.

That's more than enough to overcome a veto from Gov. Tate Reeves.

It now heads to the Senate.

I strongly suspect that at least one of the remaining holdout states will join the expansion crowd this year, most likely Georgia, Mississippi or Alabama...but it likely will be some state-specific variant as described above. Stay tuned...

...As I noted, however, in all three [states] it's pretty likely they'll go with at least a partially privatized version as Arkansas has instead of a "clean" expansion of Medicaid proper.

February 28th:

BREAKING: The Mississippi House just passed Medicaid expansion by a 96-20 vote.

That's more than enough to overcome a veto from Gov. Tate Reeves.

It now heads to the Senate.

I strongly suspect that at least one of the remaining holdout states will join the expansion crowd this year, most likely Georgia, Mississippi or Alabama...but it likely will be some state-specific variant as described above. Stay tuned...

...As I noted, however, in all three [states] it's pretty likely they'll go with at least a partially privatized version as Arkansas has instead of a "clean" expansion of Medicaid proper.

Of course, as one Alabama-based advocate put it...

Well, it looks like Ms. Adams may end up being disappointed...

BREAKING: The Mississippi House just passed Medicaid expansion by a 96-20 vote.

That's more than enough to overcome a veto from Gov. Tate Reeves.

It now heads to the Senate.