Initial Affordable Care Act Rates for 2026 have been posted

The North Carolina Department of Insurance has posted the rate changes requested by insurers for the 2026 plan year individual and small-group market plans offered under the Affordable Care Act.

Posting of the requested rates is part of the rate review process required by the Centers for Medicare and Medicaid Services (CMS). Unlike some types of insurance, the NCDOI does not set rates for health insurance.

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

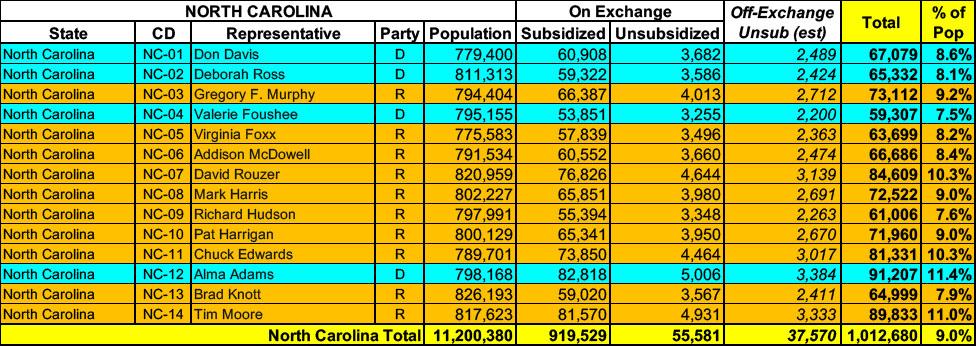

North Carolina has around ~975,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~37,000 unsubsidized off-exchange enrollees.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

As of today, 650,000 North Carolinians have access to affordable health care thanks to Medicaid expansion! When leaders come together across political differences, we can make people’s lives better.

Now we must come together to defend this bipartisan victory from proposed federal cuts. People’s health and our health care system depend on it.

Governor Josh Stein announced that as of today, 650,000 newly eligible North Carolinians have gained access to affordable health care through Medicaid expansion, including veterans and workers in child care, construction, hospitality, home health care and other industries essential to the state.

Ah, at last, another state which includes both the average requested rate changes for 2024 as well as the number of enrollees each carrier has for both the individual and small group markets in clear, transparent language!

Generally, according to NC Insurance laws, health insurance rates must not be excessive, inadequate, or unfairly discriminatory, and must exhibit a reasonable relationship to the benefits provided in the policy.

Overall, individual market carriers in North Carolina are requesting 7% rate increases in 2025 for unsubsidized policies, while small group market carriers are asking for a 6.5% bump. It's worth noting that one of the three (!) UnitedHealthcare divisions is pulling out of the NC small group market next year for whatever reason.

Back in May I noted that North Carolina's ACA Medicaid expansion initiative, which started in December 2023, had officially enrolled more than 450,000 of the estimated 600,000 NC residents eligible for the program.

North Carolina Celebrates More Than 500,000 Enrolled in Medicaid Expansion

PRESS RELEASE — More than half a million North Carolinians have now enrolled in Medicaid expansion since the program began seven months ago. Beneficiaries are now able get the quality health care they need at low cost. Governor Roy Cooper was joined by North Carolina Department of Health and Human Services Secretary Kody Kinsley, Dr. Karen L. Smith MD, FAAFP, a family physician in Raeford and Verlina Lomick,CHW-IV, Director of Community Outreach & Advocacy for Kintegra Health and health care advocates to celebrate reaching this major milestone, which had originally been projected to take as long as two years.

Last month I noted that North Carolina's ACA Medicaid expansion initiative, which started in December 2023, had officially enrolled more than 400,000 of the estimated 600,000 NC residents eligible for the program.

Today, Governor Cooper announced that more than 400,000 North Carolinians now have access to health care through the state’s Medicaid expansion following record enrollment numbers and a coordinated campaign to enroll North Carolinians across the state.

“So many younger, working people desperately need affordable health insurance and Medicaid Expansion fills the bill for thousands of them and with people all the way through age 64,” said Governor Roy Cooper. “This milestone and the speed at which we’ve reached it shows just how lifechanging Medicaid expansion is for our state and we will continue to get more eligible North Carolinians enrolled.”