Back in June, the New York Department of Financial Services published the preliminary annual rate filings for both the individual and small group health insurance markets. At the time, the NY DFS put the weighted average rate increases on the ACA-compliant individual market at 20.9% statewide, although my own calculations based on the officially-reported market share enrollment came in slightly lower, at 20.7%.

Meanwhile, they put small group market, NY DFS put it at a 15.3% average increase (almost identical to my 15.4%).

However, I made sure to include an important caveat:

It's important to remember that these are not final rate increases--New York in particular has a tendency to slash the requested rate hikes down significantly before approving them.

As the Writers Guild of America's ongoing strike enters its fifth month (and the Screen Actors Guild-American Federation of Television and Radio Artists, or SAG-AFTRA, approaches 50 days with their own strike for similar demands), Jackie Fortier has an interesting article at NPR about one of the less-discussed aspects which is often much higher profile in union strikes: Health insurance:

The health insurance offered by both unions is predicated on the notion that it is for members who work consistently and lucratively enough to make a minimum amount of money.

...the policy offered by the screenwriters guild, for instance, feels like a holdover from a bygone age. It has no monthly premiums, costs $600 per year to cover the rest of your immediate family and has deductibles that are in the hundreds – not thousands – of dollars.

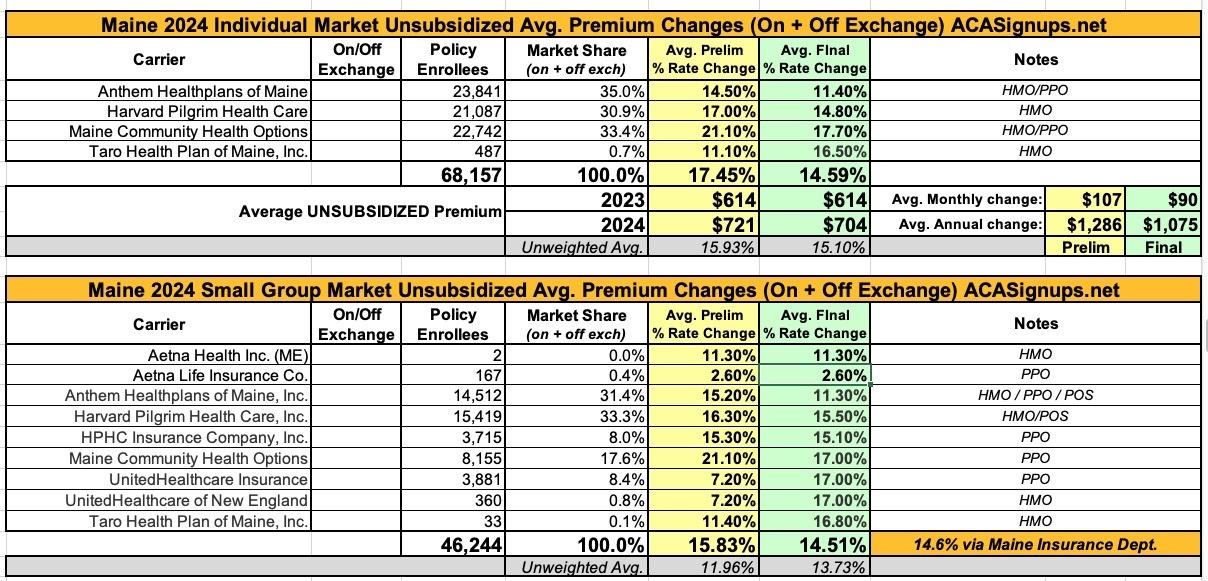

At the time, the weighted average rate increases requested by insurance carriers in Maine were a steep 17.9% hike for the individual market and a 15.8% increase on the small group market.

CMS Takes Action to Protect Health Care Coverage for Children and Families

States must assess and fix their systems so eligible children and families can stay covered.

Today, and as part of its ongoing work to make sure all Americans have access to health care coverage, the Centers for Medicare & Medicaid Services (CMS) sent a letter to all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islandsrequiring them to determine whether they have an eligibility systems issue that could cause people, especially children, to be disenrolled from Medicaid or the Children’s Health Insurance Program (CHIP) even if they are still eligible for coverage, and requiring them to immediately act to correct the problem and reinstate coverage.

In July, Covered California announced the preliminary weighted average 2024 premium rate changes for the ACA individual market. They still haven't released the final/approved rates, or the small group market average rate changes, but today they released the final rate changes for standalone dental plans:

SACRAMENTO, Calif. — Covered California announced that the statewide weighted average rate change for dental coverage in 2024 will be 4.31 percent. The rate increase is the first since 2020 and continues a trend of holding costs steady for consumers.

Marketplace Hosts Informational Campus Events, Enrollment Assistors Help Eligible New Yorkers Maintain Health Coverage as Renewal Deadlines Approach

ALBANY, N.Y. (August 28, 2023) – NY State of Health, the state’s official health plan Marketplace, today announced a state-wide college campaign, with informational events taking place on campuses as students return. Certified enrollment assistors will be available in popular spots on campus to educate students on affordable, quality health insurance through the Marketplace, and help current enrollees renew their coverage.

There Are Just a Few Days Left for Friday Health Plans Customers to Avoid a Gap in Coverage

08/29/2023

Customers must enroll in a plan by this Thursday to have coverage that starts Sept. 1

DENVER— Friday Health Plans customers have less than three days to choose a new health insurance plan before their current health insurance coverage ends. Last month, the Colorado Division of Insurance announced that it had asked the courts to move Friday Health Plans into liquidation, ending coverage for all Friday Health Plans customers on August 31, 2023. Connect for Health Colorado, the state’s official health insurance marketplace, continues to urge Friday Health Plans customers to sign up for a new plan on or before this Thursday, August 31, to avoid a gap in coverage.

Since 2013, Navigators have helped Americans understand their health insurance options and facilitated their enrollment in health insurance coverage through the Federally-facilitated Marketplace (FFM). As trusted community partners, their mission focuses on assisting the uninsured and other underserved communities. Navigators serve an important role in connecting communities to health coverage, including communities that historically have experienced lower access to health coverage and greater disparities in health outcomes. Entities and individuals cannot serve as Navigators without receiving federal cooperative agreement funding, authorized in the Affordable Care Act, to perform Navigator duties.

New York's implementation of the ACA's Basic Health Plan provision (Section 1331 of the law) is called the Essential Plan. It currently serves over 1.1 million New Yorkers, or over 5x as many residents as ACA exchange plans do.

Under the ACA, most states have expanded Medicaid to people with income up to 138 percent of the poverty level. But people with incomes very close to the Medicaid eligibility cutoff frequently experience changes in income that result in switching from Medicaid to ACA’s qualified health plans (QHPs) and back. This “churning” creates fluctuating healthcare costs and premiums, and increased administrative work for the insureds, the QHP carriers and Medicaid programs.

The out-of-pocket differences between Medicaid and QHPs are significant, even for people with incomes just above the Medicaid eligibility threshold who qualify for cost-sharing subsidies.

Not much noteworthy here other than that Celtic is joining the Delaware individual market for the first time next year. Aetna Health seems to have added a second division in the small group market as well, but perhaps not since both the requested rate change and the current enrollment are identical to the existing Aetna Health listing, so I'm not sure what to make of that. It's a nominal number of enrollees, however, so it doesn't really move the needle anyway.

In any event, Delaware carriers are asking for an average 4.7% rate increase on the individual market and an 8.7% hike for small group plans...subject to state regulatory approval, of course.

The list includes 9 major items (some of which actually include a lot more than one provision within them). It really should include ten, since I forgot about implementing a Basic Health Plan program like New York and Minnesota have (and as Oregon is ramping up to do soon as well), but it's still a pretty full plate.

For the first time, Medicare will be able to negotiate prices directly with drug companies, lowering prices on some of the costliest prescription drugs.

For the first time, thanks to President Biden’s Inflation Reduction Act – the historic law lowering health care costs – Medicare is able to negotiate the prices of prescription drugs. Today, the U.S. Department of Health and Human Services (HHS), through the Centers for Medicare & Medicaid Services (CMS), announced the first 10 drugs covered under Medicare Part D selected for negotiation. The negotiations with participating drug companies will occur in 2023 and 2024, and any negotiated prices will become effective beginning in 2026. Medicare enrollees taking the 10 drugs covered under Part D selected for negotiation paid a total of $3.4 billion in out-of-pocket costs in 2022 for these drugs.

Every year, I spend months painstakingly tracking every insurance carrier rate filing for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need. The actual data I need to compile my estimates are actually fairly simple, however. I really only need three pieces of information for each carrier:

Georgia's health department doesn't publish their annual rate filings publicly, but they don't hide them either; I was able to acquire pretty much everything via a simple FOIA request. Huge kudos to the GA OCI folks!

Back in July, I compiled the weighted average requested rate changes for 2024 for both the Georgia individual and small group markets. At the time, individual market carriers were asking for rate hikes ranging from a relatively modest 6% (UnitedHealthcare) to a stunning 27.7% increase (Cigna). The weighted average came in at right around 15% even.

On the small group market, meanwhile, only around half the carrier filings were available at all, so I couldn't really run a proper average, although of those which had filed theirs, the average came in at 12.6%.

Earlier today I acquired the most recent rate filings for every carrier in both markets. I don't know for certain whether these are the final, approved rates for 2024, but it seems likely:

Medicaid recipients deemed ineligible for coverage may be eligible for financial assistance and are encouraged to contact Nevada Health Link to avoid a lapse in health coverage

CARSON CITY, Nev. – As the redetermination process associated with the unwinding of the Public Health Emergency continues, Nevada Health Link, Nevada’s health insurance marketplace, is continuing to work diligently to streamline the enrollment process for individuals and households whose increased income no longer qualifies them for Medicaid coverage.

2023-24 Enacted Budget Invests in Health Equity by Adopting Key Evidence-Based Interventions to Better Care for New York Parents and Newborns

ALBANY, N.Y. (August 24, 2023) – The New York State Department of Health announced several key initiatives aimed at improving maternal and newborn health. Enacted as part of the 2023-24 New York State Budget, the state is committing to multiple Medicaid investments that will expand access to prenatal and postnatal care and support better birth outcomes. This announcement is released on the heels of the State’s adoption of the federal option to extend Medicaid and Child Health Plus (CHPlus) postpartum coverage from 60 days to a full year following pregnancy.

The Inflation Reduction Act of 2022 was signed into law on August 16, 2022. The new law provides meaningful financial relief for millions of people with Medicare by improving access to affordable treatments and strengthening the Medicare Program both now and in the long run. The law makes improvements to Medicare by expanding benefits, lowering drug costs, keeping prescription drug premiums stable, and improving the strength of the Medicare program. The law also extends enhanced financial help to purchase HealthCare.gov and state-based Marketplace plans and expands access to Advisory Committee on Immunization Practices (ACIP) recommended vaccines for adults with Medicaid coverage.

NJ Department of Banking and Insurance Announces Federal Approval of Section 1332 State Innovation Waiver Extension to Continue Reinsurance Program

Reinsurance Program Improves Health Insurance Affordability

TRENTON – The New Jersey Department of Banking and Insurance today announced the state received federal approval of a Section 1332 State Innovation Waiver Extension to continue a reinsurance program that lowers health insurance premiums in the individual market by 15 percent. The reinsurance program increases certainty and stability in New Jersey’s individual health insurance market.

ST. PAUL, Minn.—The Minnesota Insulin Safety Net Program was created in 2020 to help Minnesotans who face difficulty affording their insulin. During the 2023 legislative session, the Minnesota Legislature made important changes to the program that will improve access to this life-saving drug for undocumented Minnesotans who are struggling to afford their insulin.

Starting August 1, 2023, Minnesotans can use an Individual Taxpayer Identification Number (ITIN) as an accepted form of identification for program eligibility. This change provides a pathway to access the program for those who do not have a valid Minnesota identification card, driver’s license or permit, or tribal-issued identification. For minors under the age of 18 who need help affording insulin, a parent or legal guardian can use an ITIN as an accepted form of identification.

Open Enrollment Period at Get Covered New Jersey Begins November 1, 2023

Historic Levels of Financial Help Remain Available for the Upcoming Year

TRENTON — The New Jersey Department of Banking and Insurance today announced it is accepting applications for community organizations to serve as Navigators to assist residents with health insurance enrollment for the upcoming Get Covered New Jersey Open Enrollment Period and throughout 2024. This year, the department is making available a total of $5 million in grant funding for Navigators in an effort to ensure enrollment assistance is available in the community for residents seeking coverage through Get Covered New Jersey, the state’s official health insurance marketplace.

Last month the Centers for Medicaid & Medicaid Services (CMS) director of the Center for Consumer Information & Insurance Oversight (CCIIO...yeah, those names & acronyms just roll off the tongue, don't they?) informed the state of Georgia that they're gonna have to wait one more year before launching their own fully state-based ACA exchange (SBE) platform.

There were several reasons given for the 1-year delay, but many of them stemmed from the fact that Georgia was attempting to skip the "Federally-Facilitated" SBE phase which every other state which has made the transition to their own full state-based platform has undergone for at least one year.

Individual Coverage Health Reimbursement Arrangements, or the unfortunate-soundingICHRA for short, are a type of health insurance arrangements which were created via Trump administration-era regulations back in 2019.

So far, about 46 percent of these customers have picked a new plan*

DENVER— Friday Health Plans customers have about two and half weeks* to choose a new health insurance plan before their current health insurance coverage ends. Connect for Health Colorado, the state’s official health insurance marketplace, is urging Friday Health Plans customers to sign up for a new plan before the end of the month to avoid a gap in coverage.

*Note that this press release was issued 9 days ago, so CO Friday enrollees actually only have 8 days left.

OK, after several weeks of this site turning into AnnualRateFilingsDotCom, I'm finally catching up on some other important ACA/healthcare-related developments which are happening.

I've finally completed my Annual Individual & Small Group Market Rate Filing project for preliminary 2024 rate filings, having analyzed & crunched the numbers for the individual and small group markets across all 50 states + DC, so it's time to step back and see where things stand nationally.

It's important to remember that these are preliminary filings only--many of the carriers will have their final 2024 rate changes reduced, although in many cases they tend to be approved as is.

It's also important to note that I only have weighted average rate changes for 30 states (+DC). For the other 20 states, I've only been able to generate unweighted average rate changes--that is, I have to assume every carrier in that state has the same number of ACA enrollees since their rate filing forms are either unavailable or heavily redacted, making it impossible for me to know how many people are enrolled in their policies.

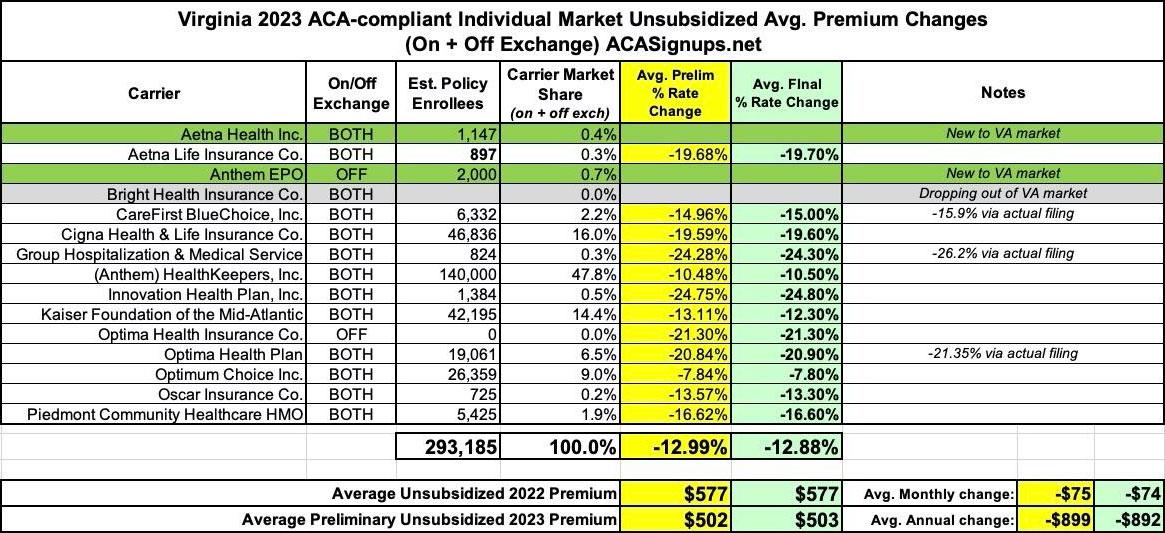

The main reason for this was the implementation of a so-called "reinsurance" program which was originally passed by the (then Democratically-controlled) state legislature:

The most significant thing to impact Virginia carriers 2023 filings was the state's Section 1332 Reinsurance Waiver. I wrote about this way back in 2018 when the state was originally considering applying for one, but it didn't actually go into effect until January 2023:

Shapiro Administration Announces Public Comment Period On Proposed 2024 Health Insurance Rate Increases

Harrisburg, PA – Pennsylvania Insurance Commissioner Michael Humphreys today welcomed public comment on the requested rate changes insurance companies currently operating in Pennsylvania's individual and small group market filed for 2024. The comment period on the proposed rate increases will close on September 8.

"The Shapiro Administration is committed to raising awareness about the importance of health insurance and providing increased access to affordable, comprehensive health coverage," said Humphreys. "We strongly encourage individual market consumers to shop for coverage on Pennie® where they may qualify for financial assistance that, as we consistently hear from Pennsylvanians, makes coverage more affordable than they thought might be possible."

Oklahoma is another state where I have no access to the actual enrollment data--all I have to go by are the average requested rate changes for each carrier on the individual and small group markets. As a result, the averages for each market are unweighted.

For individual market plans, that unweighted average is just 2.2%, though the carriers range from as low as a 3.5% drop to as high as a 6.1% increase. It's also worth noting that Friday Health Plans are kaput.

Similarly, for the small group market, average requested rate hikes range from as little as 0.8% for CommunityCare to as much as a 9.3% for Aetna. The unweighted average is 4.9%.

Not much to report about the 2024 individual and small group market rate filings. I could only find current enrollment numbers for two of the three indy market carriers and for three of the five small group market carriers. However, based on last year's total enrollment, I'm estimating ND's total indy market at being roughly 50,000 people, which means I was able to make an educated guess at how many are enrolled in Sanford Health Plan policies.

Based on this, I have a (mostly) weighted requested average rate increase of 4.4% for individual market plans and an unweighted average of 6.5% for small group market plans.

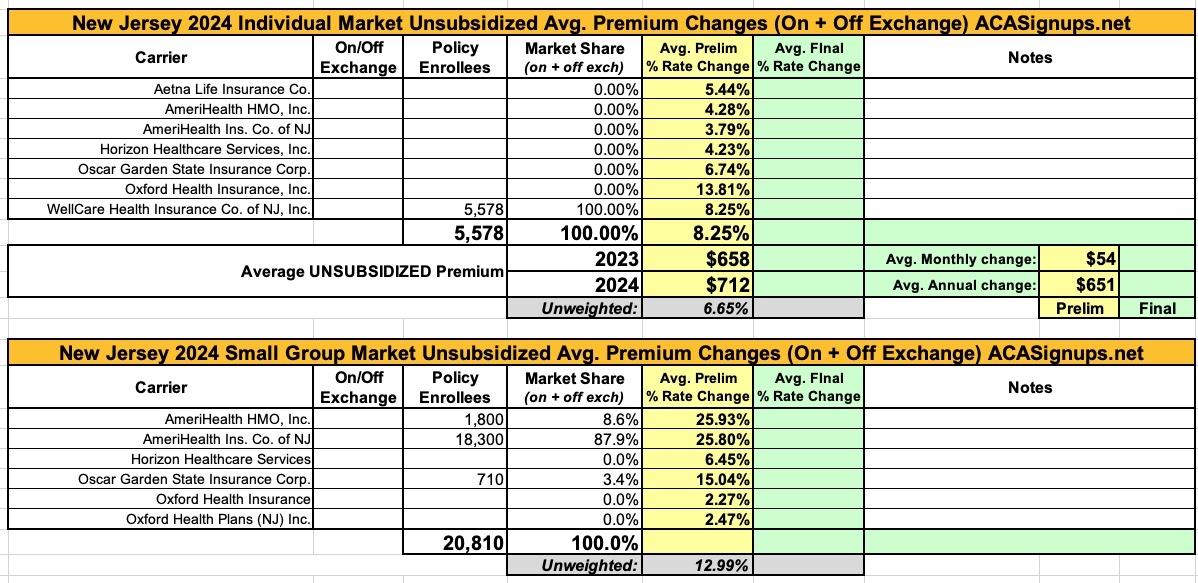

New Jersey individual & small group market carriers are asking for unweighted average rate increases of 6.7% and 13.0% respectively for 2024. However, the unweighted averages don't tell the whole story--the carriers are asking for rate hikes ranging from as low as 3.8% to as high as 13.8% on the individual market, and from as low as 2.3% to a stunning 25.9% for small group plans.

As is the case with far too many states these days, most of the rate filing memorandums are heavily redacted in New Jersey, making it nearly impossible to get ahold of the actual enrollment numbers, which means I have no way of running a weighted average on either market.

While nearly 16.4 million Americans selected Qualified Health Plans (QHPs) via the federal and state ACA exchanges/marketplaces during the official 2023 Open Enrollment Period (along with an additional 1.2 million signing up for a Basic Health Plan (BHP) program in New York & Minnesota, which CMS continues to inexplicably treat as an afterthought in such reports), not all of them actually pay their first monthly premium (for January) for various reasons:

The good news about New Hampshire's health insurance market is that they're the only state without its own ACA exchange which produces publicly-accessible monthly reports on individual on-exchange market enrollment. The bad news is that they don't seem to publish the actual rate filings in an easy-to-read format, which means I'm left with the federal rate review website, which sometimes posts average rate requests which don't match up with the actual filings...but it's gonna have to do here.

With these two data sources in hand, New Hampshire's individual market carriers are asking for a weighted average increase of 3.1%. It's important to note that Anthem Health Plans and Matthew Thornton Health Plan are listed as separate carriers on the federal Rate Review website (with separate average rate requests), but on the state's monthly report, they're merged into a single listing.

Nevada used to be a state where the annual individual & small group rate filings were fairly transparent. They have a pretty easy-to-use searchable filing database which clearly lists the carriers, market, maximum & minimum rate changes and even includes the SERFF Tracking numbers for every filing.

Unfortunately, this year at least, most of that proves useless for my purposes. The average rate changes are posted, but the enrollment data is still hidden from public view--entering the SERFF Tracking Numbers still brings up nothing in the SERFF database, and the actuarial memos posted at RateReview.HealthCare.Gov are mostly redacted. As a result, I'm only able to enter enrollment data for one of the nine carriers on the Nevada individual market, and none on the small group market.

Interestingly, the one I have enrollment data for (Aetna Health of Utah) also has a curious discrepancy: The filing itself lists the average requested rate increase as being 6.97%, but on the RR.HC.gov site it only shows up as 1.36%. The other eight carriers all match up (or are within a tenth of a percentage point, anyway).

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has 10 different carriers participating in the individual market.

One thing which sets Massachusetts (along with Vermont) apart from every other state is that their Individual and Small Group risk pools are merged for premium setting purposes.

Normally you would think this would make my job easier, since I only have to run one set of analysis instead of two...but until recently, it was surprisingly difficult to get ahold of exact enrollment data for each carrier on the merged Massachusetts market (and even more difficult to break out how many are enrolled in each market since they're merged...not that that's relevant to the actual rate changes).

Kentucky is yet another state where the actuarial memos are heavily redacted, making it difficult to acquire information such as the number of enrollees...which in turn makes it impossible to run a weighted average requested rate change for the individual or small group markets.

There are four carriers offering policies on the KY individual market (Anthem, CareSource, Molina and WellCare), with an unweighted average rate change request of 4.1%. Molina has provided an unredacted actuarial memo which includes their enrollment...but it's only 505 people, while KY's total indy market is likely closer to 75,000 or so including the off-exchange market.

While numerous other states have already done the same thing (and several more are in the process of doing so as well), Georgia's move to their own enrollment platform was especially noteworthy for two reasons:

First, because it represents as complete 180-degree policy turn from their prior attempts (over the course of several years) to eliminate any formal ACA exchange (federal or state-based) in favor of outsourcing it to private insurance carriers & 3rd-party web brokers.

Back in late 2021, Colorado launched their own new, state-based ACA financial subsidies on top of federal subsidies which have already been enhanced (at least through the end of 2025) via the American Rescue Plan and Inflation Reduction Act:

The financial help you can get to lower your out-of-pocket costs are healthcare discounts called Cost-Sharing Reductions. Connect for Health Colorado is the only place you can apply for financial help to lower the cost of private health insurance. Due to the American Rescue Plan, Coloradans are now eligible for more savings than ever before.

Consider a Silver plan if your Health First Colorado (Medicaid) coverage recently ended or your income is over the limit to qualify

Connect for Health Colorado launched a new state-funded program recently to provide even more healthcare savings to people shopping on the Marketplace for 2022 whose income is just over the limit to receive Health First Colorado (Medicaid) and who enroll in a Silver-level plan.

The IDOI will finalize its review of the 2024 ACA compliant filings both on and off the federal Marketplace by August 17, 2023. The Centers for Medicare and Medicaid Services (CMS) will issue the ultimate approval for the Marketplace plans sold in Indiana. CMS will issue its approval on or before September 20, 2023.