For 2017, North Carolina's unsubsidized, weighted average individual market rate hikes came in at around 24.2%. With carriers like Aetna, United Healthcare, Humana and Celtic all dropping out of the NC exchange market, there wasn't much math to do in order to find a weighted average: The only individual market carriers left were Blue Cross Blue Shield of NC, Cigna and "National Foundation Life Insurance", which is basically a non-entity shell company related to "Freedom Life", the less said about the better. Since Cigna only had around 1,200 indy market enrollees at the time (less than 0.5% of the total market share), that pretty much left BCBSNC as the only game in town, so their 24.3% hike was the whole shebang for the state.

On Tuesday, the HHS Dept., knowing that the CBO score of the passed version of the AHCA was imminent (and that it would likely be devastating), released a report which they hoped would take attention away from the CBO score: A comparison, they said, of how much individual market healthcare policy premiums have increased since the Affordable Care Act regulations were fully implemented. To do this, they compared the average monthly premiums for individual market policies in 2017 against average monthly premiums in 2013...the final year before every newly-enrolled individual market policy had to be fully ACA-compliant.

Their conclusion was that, across the 39 states covered by the federal exchange (HealthCare.Gov), average premiums have more than doubled, from $224/month in 2013 to $476/month in 2017...a 105% increase overall.

(this is Part Two of my analysis of the CBO score of AHCA 2.0 (the version which actually passed the House 3 weeks ago). Part One is here.

OK, digging into the PDF itself, let's see what else there is of interest... (this is a blog post in progress...check back for frequent updates...)

Here's a list of what HASN'T changed from the "1.0" version of the AHCA:

In this cost estimate, as in the preceding estimates, the budgetary effects related to health insurance coverage would stem primarily from the following provisions:

Reducing the federal matching rate for adults made eligible for Medicaid by the ACA to equal the rate for other enrollees in the state, beginning in 2020.

Goodbye 90% Federal funding! States would have to pony up anywhere from 25-50% of the funding if they wanted to keep those folks covered.

The critic blurb is a staple of arts advertising. Yet if you look behind some blurbs, you'll find quotes out of context, quote whores, and other questionable ad practices. Blurb Racket exposes the truth behind critics blurbs in movie ads from the New York Times.

For the second straight year, Gelf is unveiling its favorite blurbs of the year (see our favorites from 2007). Each one exemplifies a deceptive practice that is near the top of the blurb writer's toolbox. Don't like a review? Rearrange it, or cut out the negativity, or change a word entirely. Or even better, find a non-critic associated with a reputable publication who raved, and use that.

Examples from the article (and the version from a year earlier):

UPDATE 4:30PM: SCROLL DOWN FOR THE ANALYSIS OF THE CBO SCORE.

Yes, this is it, kids...the Big Day all healthcare wonks have been waiting for: The Congressional Budget Office is releasing their score of the final version of the AHCA (that is to say, the version which was actually voted on and passed by a whisker 3 weeks ago) later on today.

Remember, Paul Ryan and the House GOP insisted on ramming the vote through before the CBO score came out, which means that due to the way Congressional budget rules work, depending on how much the CBO think the final changes to the bill impact the budget, they may have to go back and make more changes which would require another vote in the House...and that's all before it moves onto the Senate, where the GOP Senators have already said they plan on starting from scratch anyway. Fun times!

Premiums for individual market coverage have increased significantly since the Affordable Care Act’s key provisions have taken effect, but most estimates have focused on annual increases and have not captured the comprehensive increase in premiums since 2013, and thus do not accurately capture the ACA’s true effect.

Comparing the average premiums found in 2013 MLR data and 2017 CMS MIDAS data shows average exchange premiums were 105% higher in the 39 states using Healthcare.gov in 2017 than average individual market premiums in 2013. Average monthly premiums increased from $224 in 2013 to $476 in 2017, and 62% of those states had 2017 exchange premiums at least double the 2013 average.

The big headline, of course, is that according to the ASPE report, individual market premiums more than doubled on average between 2013 (the last year before all newly-enrolled-in healthcare policies had to conform to full ACA regulations) and 2017.

To which I respond: Yes, I'm sure you're correct...and your point is?

Health Care Service Corp. — the parent company of the Blue Cross and Blue Shield affiliates in Illinois, Montana, New Mexico, Oklahoma and Texas — recorded an $869 million profit in the first quarter of 2017, according to the company's latest financial documents. That was a $1.3 billion turnaround after HCSC lost $442 million in the first quarter of 2016.

How to interpret this: The Affordable Care Act exchanges in some areas are hurting, but overall are not imploding. Many insurance companies continue to do well (like Florida Blue) or are turning things around (like HCSC). And HCSC carries a lot of weight, since it covers nearly 1.1 million people in ACA plans and is the largest Blue Cross and Blue Shield company after Anthem.

Note: Given the time constraint--today is the deadline for submitting a letter--I've stolen some of the following from Andrew Sprung:

Topher Spiro of the Center for American Progress acquired a letter from Senate Finance Committee Chair Orrin Hatch to healthcare "stakeholders," inviting their input by May 23 on Republican senators' efforts to write an ACA repeal bill. Hatch asked that letters be sent to HealthReform@Finance.Senate.gov.

Since the Republican senators' bill-writing process is as secretive and rushed as the House's, Spiro seized the opportunity to encourage non-privileged "stakeholders" -- all of us -- to send their two cents to the email address provided. He has offered to tweet any letters tweeted at him, with a screenshot.

The House of Representatives and Department of Justice plan to ask the DC federal appeals court to keep on hold for another 90 days a lawsuit that questions the legality of cost-sharing subsidies in the Affordable Care Act, according to four people familiar with the matter.

The White House, during that time, will continue to make payments to insurers, according to a senior administration official.

OK, assuming they do indeed ask for this, and assuming the court grants a third 90-day extension, this means that CSR reimbursement payments can continue for another 3 months. That's the good news.

Insurers planning to offer plans on the exchanges in 2018 must submit their pricing in the coming days and weeks.

This is the actual headline of an actual article posted on Breitbart.com right now:

I'm loathe to link to the article itself (I did include one somewhere on this page, feel free to look for it), but a Google search will bring it up. Even more remarkably for Breitbart, much of it is actually pretty darned accurate:

Obamacare will go into a death spiral on May 22 if the Trump administration chooses not to continue fighting in court to preserve cost-premium subsidies that were ruled illegal last year.

On May 12, 2016, U.S. District Court Judge Rosemary M. Collyer ruled House v. Burwell that the Obama Administration’s payment of cost-sharing subsidies without congressional approval was a violation of the Constitution’s Appropriations Clause.

About 5 weeks ago I noted that organizations representing pretty much the entire healthcare industry sent urgent letters to Donald Trump, HHS Secretary Tom Price, Treasury Secretary Steven Mnuchin, OMB Director Mick Mulveney and current CMS Administrator Seema Verma...basically, every major healthcare-related administration figure...practically begging them to fund the goddamned Cost Sharing Reduction reimbursements.

They made it crystal clear how vitally important doing this was, and Trump grudgingly went ahead and made the April payment, then later indicated that he was "probably" going to keep reimbursing carriers for the CSR funds legally owed to them on an ongoing basis, at least until the House vs. Price (formerly House vs. Burwell) lawsuit appeal process was completed.

The District of Columbia is the 6th state (OK, it's not a state but it's considered one legislatively for purposes of the ACA) to post their initial 2018 rate filings (h/t to Louise Norris for the heads up). For 2017, the weighted average rate increase for the individual market was a mere 7.3%, highly unusual for this year, while the small group market increase was almost non-existent: Just 0.4% overall.

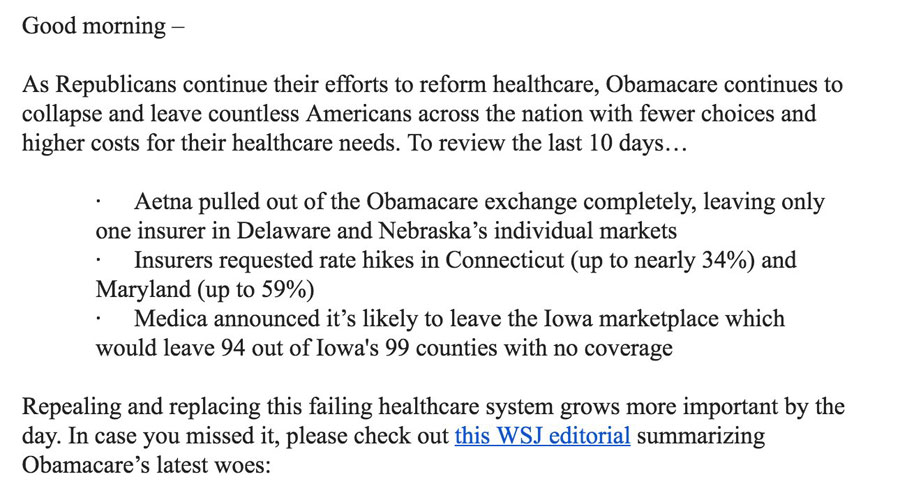

Health insurers and state officials say Trump is undermining Obamacare, pushing up rates

Health insurers across the country are making plans to dramatically raise Obamacare premiums or exit marketplaces amid growing exasperation with the Trump administration’s erratic management, inconsistent guidance and seeming lack of understanding of basic healthcare issues.

At the same time, state insurance regulators — both Democrat and Republican — have increasingly concluded they cannot count on the Trump administration to help them ensure that consumers will have access to a health plan next year.

As noted in my last post, it turns out that if the CBO score of the final version of the AHCA (that is, the one which passed two weeks ago) doesn't project the law to save at least $2 billion over a 10 year period, the House Republicans would have to start over again from scratch and re-vote on yet another version of their bill.

Now, the good news for them is that the CBO projected the prior version to save $150.3 billion over that period, so they have $148.3 billion worth of wiggle room, right? What are the odds of the CBO's new projection assuming that the passed version would eat up that much more money?

The key is does CBO assume lots of states waive benefits/community rating, and lots of healthy people use tax credits for skimpy insurance. https://t.co/vLx28MT5Bv

House May Be Forced to Vote Again on GOP's Obamacare Repeal Bill

House Republicans barely managed to pass their Obamacare repeal bill earlier this month, and they now face the possibility of having to vote again on their controversial health measure.

One of the biggest Achilles' heels of the ACA exchanges has always been that participation in them by private insurance companies is completely voluntary. There's nothing compelling any particular carrier to offer policies on the exchanges aside from them hoping to make a profit by doing so thanks to the additional policy enrollees, mostly from people who are receiving subsidized coverage via Advance Premium Tax Credits (APTC) and/or Cost Sharing Reduction (CSR) assistance.

This Axios piece by Caitlin Owens is extremely short...a mere 139 words in all...so sticking with a "fair use" quote is tricky, but I'll do my best:

Senate Finance Committee chairman Orrin Hatch says he could support delaying the repeal of the Affordable Care Act's individual mandate for a while, or even indefinitely, as a way to stabilize the marketplaces. "I wouldn't mind" postponing the repeal until after 2020, he told reporters this afternoon. "It all comes down to budgetary concerns and how it's going to be written." And he didn't rule out keeping it even longer:

"I'd like to not have it at all, but you know, it all comes down to, what's the art of the doable?"

A few days ago, CMS announced that they're retooling the ACA's SHOP program (at least on the federal exchange) so that instead of small businesses using HealthCare.Gov for eligibility verification, enrollment and payments, going forward it will only be used for verification, with the businesses then being kicked over to the actual insurance carrier website in order to actually enroll in the policies and make payments.

Although the Trump Administration and HHS Secretary Tom Price are hell bent on killing off the ACA altogether, this move didn't bother me for several reasons. For one thing, the SHOP program has always been kind of a dud anyway, with only around 230,000 people being enrolled in it nationally. For another, a business signing up their employees for coverage is a very different animal from an individual signing their family up for a policy. Finally, for several reasons, SHOP enrollment across the dozen or so state-based exchanges is actually higher than it is across the 3 dozen states covered by HC.gov, and the state-based exchanges aren't impacted by this policy anyway.

While poking around in the SERFF rate filing database for different states, I occasionally find filings which DON'T apply to ACA-compliant policies or enrollees but which are of interest to healthcare nerds such as myself. I've decided to bundle these into a single post as they pop up, so check this entry once in awhile.

IOWA: Big Kahuna carrier Wellmark submitted a filing for non-ACA compliant small group policies (either grandfathered or transitional) which have effective/renewal dates of July, August or September 2017. The requested rate increase is 7.0% on average, which is pretty typical for small group plans, and it appears that Wellmark had 51,003 people enrolled in such policies as of 12/31/16. Nothing odd there.

Julie McPeak is the Tennessee Insurance Commissioner. She was appointed by a Republican Governor, Bill Haslam, and while the position itself appears to be nonpartisan, I've found several links indicating that yes, she's a Republican herself. This is hardly surprising in Tennessee, of course, and there's nothing wrong with it...but it's noteworthy given that Tennessee is among the 19 states which has been fairly hostile towards the ACA in general over the years (no state exchange, no Medicaid expansion, total GOP control and so forth).

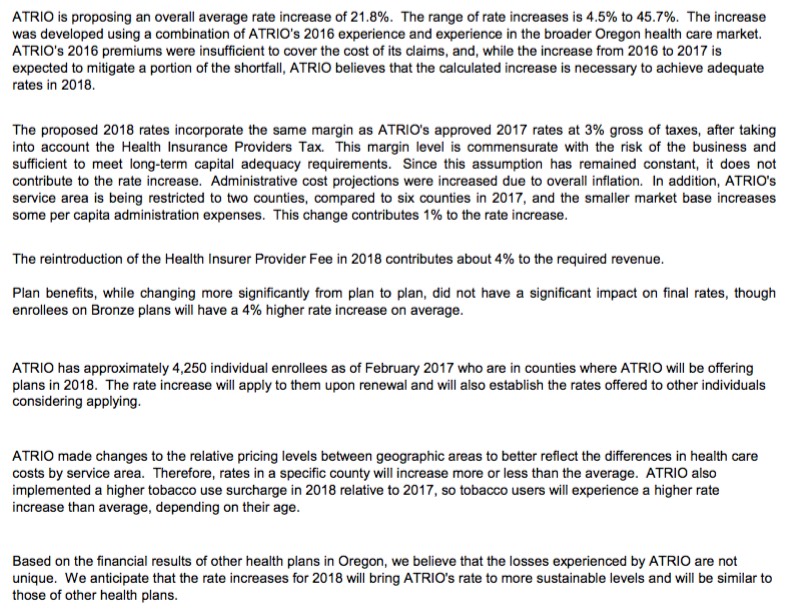

Oregon is the 5th state to post their initial 2018 rate filings. Last year their weighted average increase was roughly 26.5% across 10 individual market carriers. This year I only see 8 carriers offering policies on the indy market, but the two missing are "Trillium" and "ZOOM", neither of which had more than a handful of enrollees to begin with.

As you can see, ATRIO Health Plans was refreshingly clear in their rate justification letter, not only listing the key numbers (covered lives, average increase) but the reasons for it: 4% due to the reinstatement of the ACA's carrier tax; 1% due to them choosing to shrink their own coverage area from 6 counties to just 2; an increase for smokers., etc. They list 4,250 people being impacted by the increase; I don't know the population of the other 4 counties they're pulling out of, but assuming they're roughly equal, around 8,000 current enrollees will have to shop around this fall.

Regular readers know that generally speaking, I support the ACA overall. They also know that I also have significant criticisms of the law, and have compiled a lengthy list of fixes/improvements both small and large which I feel are necessary to stabilize the individual market. I've also written on occasion about the SHOP provision of the ACA: The small business version of the ACA exchanges.

The idea was to give small businesses with fewer than 50 employees an open marketplace to comparison shop, similar to the individual exchanges, and also to provide some amount of financial assistance to them along the lines of APTC for indy market enrollees. The ACA requires businesses with over 50 full-time employees to provide coverage, but it's voluntary for those under 50, so SHOP has always been more of a courtesy program than a necessary one.

Vermont is the 4th state to post their initial 2018 rate filings. Vermont has a couple of unusual policies re. their healthcare market: First, while they do technically have an off-exchange individual market, those policies are all fully ACA-compliant QHPs and are tracked exactly the same as on-exchange QHPs, meaning this dashboard report from February includes just about all of their individual market enrollees: 28,775 on exchange + 5,662 off-exchange, for a total of 34,437 ACA-compliant enrollees. Vermont didn't allow transitional plans, so aside from an unknown number still enrolled in grandfathered plans, that should represent their entire individual market.

Assuming this ratio hasn't shifted much over the past 8 years, around 28% of the total U.S. population are mothers,

Of course, women over 64 (mostly on Medicare) are much more likely than the general population to be mothers...but girls under 18 are far less likely to be (well...under 16, anyway...the birth rate varies from state to state, of course), so I'm assuming that these cancel each other out, resulting in that 28% rate being roughly accurate.

Senate Republicans are working on a potential breakthrough that could help push through an Obamacare repeal bill – by making insurance subsidies look a lot like Obamacare.

There’s growing support for the idea of pegging the tax credits in the House repeal bill to income and making aid more generous for poorer people. But those moves — while they may win consensus among Senate moderates — are unlikely to sit well with House conservatives.

The financial assistance in the House bill “is just not robust enough to make sure that low-income individuals can actually afford a [health] plan,” said Sen. John Hoeven (R-N.D.). “If you bring those income limits down for people who really need the help, you can give them more help.”

Over the past year or so, Andrew Sprung of Xpostfactoid, Michael Hiltzik of the L.A. Times and I have repeatedly noted that as much as most insurance carriers may be griping about the individual market, their bread and butter is generally in other divisions, including the large group market but especially Managed Medicaid and Medicare Advantage:

The expansion of Medicaid benefits, thanks largely to the Affordable Care Act, helped increase enrollment in private health plans by 3.4 million in the last year,according to a new report from consulting firm PwC.

...PwC said 73% of Medicaid beneficiaries — or 54.7 million of the 75.2 million Americans covered by the health benefit program for the poor – are enrolled in private plans that contract with the Medicaid program.

...But the growth in the last year wasn’t as fast as 2015 when health plans added more than 8 million Medicaid beneficiaries as more states agreed to expand such coverage under the ACA.

I'm not sure what the original source for this is, but the following initial filing deadlines were provided by Stephen Holland via Twitter. I've already posted analyses of the Virginia, Maryland and Connecticut filings. The California and Oregon filings are supposed to have been submitted already but don't appear to be publicly available yet. In addition, it's my understanding that in many states the rates can still be adjusted/resubmitted until as late as August 16th, so I'm not really sure how useful these dates are anyway, but it's at least a guideline.

May 11, 2017 - 21% Of U.S. Voters Approve Of Revised GOP Health Plan, Quinnipiac University National Poll Finds; Voters Reject Trump Tax Plan Almost 2-1

Only 21 percent of American voters approve of the Republican health care plan passed by the U.S. House of Representatives last week, a slight improvement over the 17 percent who approved of the first health care plan in March, according to a Quinnipiac University national poll released today. Overall, the current health plan goes down 56 - 21 percent.

Apparently throwing $8 billion (over 5 years) to the junk pile gave it a 4 point increase. I wonder what would happen if they restored the $840 billion (over 10 year) that the bill takes away from Medicaid?

Except for an anemic 48 - 16 percent support among Republicans, every listed party, gender, educational, age and racial group opposes the plan, the independent Quinnipiac (KWIN- uh-pe-ack) University Poll finds.

KIMMEL: "Will the Senate make sure that the millions of children that count on Medicaid don't lose access to medical care because this House bill would cut, they say $880 billion, mostly to benefit wealthy Americans?"

CASSIDY: "Let me answer your question first technically...then more broadly...and then more broadly yet. Most children are covered under the CHIP program, and so they are gonna get the coverage they need. That's almost independent from Medicaid. Under Medicaid itself, though, clearly, if we're gonna fulfill President Trump's sort of "Contract with the American People", that people would maintain their coverage, Medicaid will be a part of that."

I'm not even gonna get into the fact that Donald Trump's word is as worthless as a diploma from Trump University. I'm just gonna focus on the bold section above.

UPDATE 6/5/17: NO SITE UPDATES UNTIL WEDNESDAY, AS I'LL BE TRAVELLING TO/FROM D.C. FOR THE 2017 NIHCM FOUNDATION HEALTHCARE DIGITAL MEDIA AWARDS DINNER...

The National Institute for Health Care Management (NIHCM) Foundation is a nonprofit, nonpartisan organization dedicated to improving the health of Americans by spurring workable and creative solutions to pressing health care problems.

...The NIHCM Foundation Health Care Digital Media Award recognizes excellence in digital media that improves understanding of health care topics through analysis grounded in empirical evidence. The three-year-old award carries a $10,000 prize and is judged by an independent panel of experts:

12. LEGALLY TIE MEDICARE ADVANTAGE/MANAGED MEDICAID CONTRACTS TO EXCHANGE PARTICIPATION.

Andrew Sprung, Michael Hiltzik and I have all written about this before. I have no idea whether it's even legally feasible/practical or not, but if so, it makes a lot of sense to me: Remember, many of the same carriers whning about losing hundreds of millions of dollars on the individual market are simultaneously making billions of dollars in profit off of their other divisions...which include fat federal and state contracts to manage Medicare and/or Medicaid plans. If they want to play in the managed care sandbox, make exchange participation a requirement as well. I'm not saying they should have to treat it as a loss leader--they'd still be able to raise their premiums at an actuarially responsible rate as appropriate--but they should have to at least participate.

We appreciate getting to meet with you and your team yesterday to update you on BlueCross’s position relative to the individual Marketplace for Tennessee as the first deadline for 2018 approaches.

To summarize: For months now I've been predicting/warning that regardless of whatever legitimate risk pool issues the ACA exchanges may still be having in many parts of the country which could lead to significant rate 2018 rate hikes no matter what, there's the additional Fear/Uncertainty/Doubt factor which is being deliberately created by Donald Trump, Tom Price and the Congressional GOP. Insurance carriers hate uncertainty above all else, and I've been expecting them to do one of two things as the 2018 rate filing deadlines approach: Either jack their rates up significantly to cover themeselves for the unholy mess brewing ahead...or to simply get out of Dodge by either dropping out of the exchanges or fleeing the entire individual market altogether, on & off exchange. Most likely, I've been saying, it'll be a combination of both.

UPDATE: As I've been warning for months, several carriers have now openly stated that perhaps 40% of their requested rate hike is due specifically to concerns about the Trump administration & the GOP's ongoing sowing of confusion and outright sabotage of the ACA and the individual market.

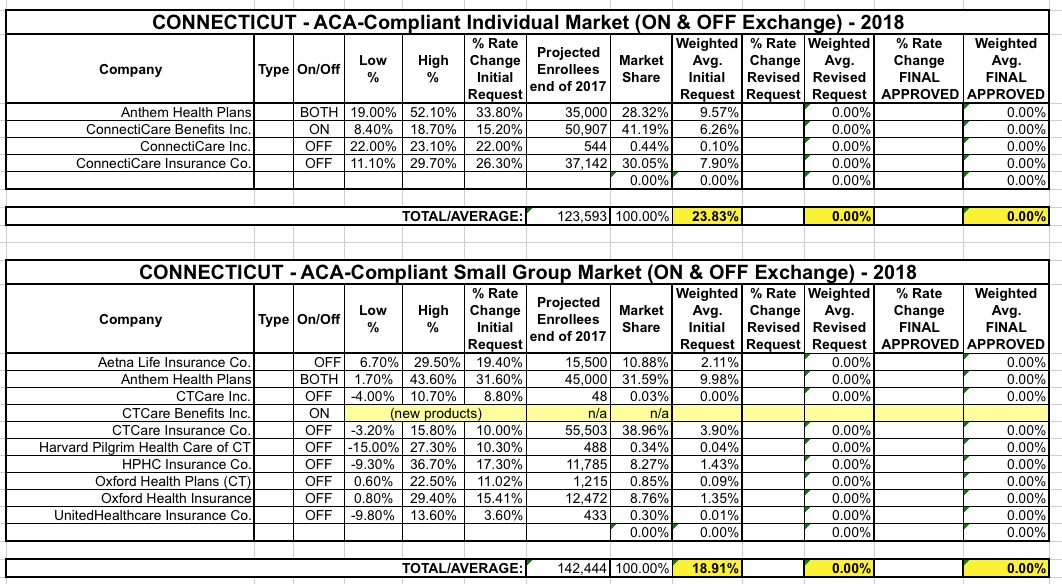

Unlike most states, Connecticut did all the legwork for me, making it incredibly easy to plug the numbers into a spreadsheet for weighted average (requested, unsubsidized) rate hikes for both the individual and small group markets:

Over the past few months, my Congressional District Breakdown tables estimating how many people would likely lose healthcare coverage if the ACA were to be "cleanly" repealed (with no replacement) have gotten a lot of attention. This was followed by the Center for American Progress (CAP) running their own estimates of how many would likely lose coverage if, instead of a "clean" repeal of the ACA as a whole, the ACA were to be partially left in place, with the GOP's AHCA (Trumpcare) bill, which dramatically changes the ACA, being signed into law instead.

UPDATE: As I've been warning for months, at least one of Maryland's carriers has openly stated that perhaps 40% of their requested rate hike is due specifically to concerns about the Trump administration & the GOP's ongoing sowing of confusion and outright sabotage of the ACA and the individual market.

Last year they had 6 carriers participating in the individual market; this year it looks like all 6 are still planning to participate:

CareFirst Blue Choice, Inc

CareFirst of Maryland Inc.

Group Hospitalization and Medical Services Inc. (GHMSI)

Cigna Health and Life Insurance Co.

Evergreen Health, Inc.

Kaiser Foundation Health Plan of the Mid-Atlantic States

The initial 2018 filings for four of the six carriers are pretty straightforward. Two of them are a bit tricky, though: Kaiser Permanente and Evergreen Health.

UPDATE: As I've been warning for months, at least one of VA's carriers has openly stated that perhaps 40% of their requested rate hike is due specifically to concerns about the Trump administration & the GOP's ongoing sowing of confusion and outright sabotage of the ACA and the individual market.

A couple of weeks ago I noted that Virginia is one of the first states to post their initial premium rate hike filings. At the time, they hadn't posted the actual filings but at least listed the insurance carriers which were planning on participating in the individual and small group markets next year, both on and off the ACA exchange:

There are so many stories I could be writing right now about the fallout, potential fallout, next steps and so forth of yesterday's House vote on the AHCA. But this one in particular really says it all.

Watch: Chris Collins admits he didn't read health care bill

WASHINGTON – Rep. Chris Collins told CNN that he didn't read the entire Republican health care bill that the House passed Thursday.

And then he told The Buffalo News that he was unaware of a key provision in the bill that decimates a health plan that serves 635,000 New Yorkers.

Asked by CNN's Wolf Blitzer if he had read the entire health bill, Collins, R-Clarence, said: "I will fully admit, Wolf, that I did not. But I can also assure you my staff did. We have to rely on our staff. ... I'm very comfortable that we have a solution to the disaster called Obamacare."

Welp. I've done everything I can to help stop them, but it looks like the House Republicans have decided to go ahead and vote on their big ol' dumpster fire of a bill after all.

No CBO score. No review. No debate. No transparency. No time for anyone to read the bill. Everything they falsely accused the Democrats of 7-8 years ago (yes, I gave a range of 7-8 years, because there was a solid year of debate, discussion, meetings, arguments and so forth before the final votes were cast).

Maybe they'll pull it off. Maybe they won't. If it passes the House, what'll happen to it in the Senate? Who the hell knows, but the fact remains that anyone who votes for this piece of crap doesn't deserve to hold office any more than the racist, misogynistic, xenophobic con-artist moronic pussy-grabbing asshole who leads their party.

Linda Qui is a NY Times Fact Checker, formerly of PolitiFact. She cited me as a fact-check source twice for PolitiFact: Once in October 2015 and again just before the election last fall (I can't find the link for that one). The first time around it was about Donald Trump's claim that premiums were skyrocketing (again, this was back in 2015, referring to 2016 rates increases). After a phone discussion, here's what I wrote her:

Yes, some people in some plans through some carriers in some states are, indeed, looking at rate hikes of “35 - 50%” if they stick with those plans in 2016. Alaska, Minnesota and Hawaii, for instance, are all looking at 30-40% average hikes, and individual plans (or individual carriers) in a few states are indeed jacking up rates by that much.

However, by my current estimates, here’s the state-by-state breakdown:

Back in January, I wrote a long rant about High Risk Pools. The general thrust was that in theory HRPs aren't necessarily a horrible idea; on paper they can be made to work...assuming the math adds up and they're properly funded on a permanent basis.

However, I also pointed out that due to the very nature of HRPs (i.e., segregating out a small, highly vulnerable group of people from the rest of society), it's incredibly easy for legislators not to properly fund or maintain them, especially after the initial funding comes up for renewal.

"Layers of protection." As Jeffery Young of the Huffington Post noted...

You always test out new talking points when you're winning. It's a sign of great confidence in the policy and politics of your situation. https://t.co/CTgnppDP01

The latest iteration of the AHCA is supposedly being scheduled for a vote (for real, this time) sometime this week. The pressure is high on both sides, the whip counts are bouncing around, the tension is palpable, etc etc.

The first time around, the biggest tug-of-war was over Medicaid expansion. This time, the major issue seems to be Pre-Existing Condition coverage...and along with it, Guaranteed Issue and Essential Health Benefits; the three have to be pretty much joined at the hip, since removing one effectively makes the other two pointless in practice. It doesn't do most people much good to be told that yes, they'll be covered even if they have cancer if that coverage is gonna cost them $50,000/month.

Anyway, people are furiously scrambling to call their member of Congress and lighting up social media spreading the word...while Donald Trump, MIke Pence and Paul Ryan are running around DC desperately trying to squeak out 216 "Yes" votes from the Republican caucus.

Regular visitors know that I write an occasional freelance piece for healthinsurance.org. The only problem is that both that site and mine have pretty narrow audiences, comprised mainly of those who are already actively seeking out analysis/opinion about health insurance matters, as opposed to the general public.

I also cross-post my diaries frequently over at Daily Kos, where the ACA Signups project originated, of course.

I've attempted to fully explain how absurdly complex the U.S. healthcare system is (and thus why it's so difficult to make major changes to it) in a way which is easy for the average Joe to get (with a few poop jokes thrown in to keep within the Cracked tradition).

Anyway, I'm a long-time fan of Cracked, so I'm pretty geeked about this. Check it out!