Healthy Alliance Life Insurance Company (HALIC) has filed for premium rate changes for its Affordable Care Act (ACA) compliant Individual health insurance plans. This filing includes an average rate change of 21.23%, effective January 1, 2026, with plan prices changing between 18.75% and 24.73%. The price changes will impact about 52,000 people that have HALIC plans now and will keep HALIC plans next year. An insured person’s actual rate increase could be higher or lower depending on their benefit, where they live, how old they are, number of children, and if they use tobacco.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Aetna Life Insurance Co:

(Aetna/CVS is dropping out of the individual market in all states; I estimate they have around 35,000 enrollees in Kansas who will have to find a different carrier for 2026)

Blue Cross Blue Shield of Kansas City:

Blue Cross and Blue Shield of Kansas City (BCBSKC) is requesting an average rate change of -6.1% for 2025 individual rates as compared to 2023 individual rates and calculated by the URRT. The changes vary by plan, with a minimum rate change of -10.8% and a maximum rate increase of 1.8%.

(Moda has heavily redacted their actuarial memo and isn't providing the number of current enrollees)

The average rate change is X.XX% as shown on Worksheet 2 of the URRT. The proposed rate Proposed Rate Increase change varies by product and plan, and the proposed rates vary by plan, age, geographic area, and tobacco use. The average rate change was calculated by comparing the weighted average premium for members on current plans and rates to the weighted average premium for members on renewal plans and rates.

A summary of the major components and their contribution to the rate change is provided in the table below.

The proposed rate change of 39.0% applies to approximately 142,324 individuals. Ambetter of Magnolia Inc.’s projected administrative expenses for 2026 are $89.76 PMPM. Administrative expense does not include $34.22 for taxes and fees. The historical administrative expenses for 2025 were $73.84 PMPM, which excludes taxes and fees. The projected loss ratio is 84.4% which satisfies the federal minimum loss ratio requirement of 80.0%.

Blue Cross Blue Shield of MS:

The 2026 monthly health insurance premium is made up of four pieces: estimated claim costs, administrative costs, taxes and fees, and risk/profit margin.

SACRAMENTO, Calif. — Covered California is kicking off its open-enrollment period for 2026 coverage on Nov. 1 amid uncertainty surrounding the enhanced premium tax credits that have delivered greater affordability and record enrollment across the nation.

This marks the 13th open-enrollment period under the Patient Protection and Affordable Care Act, which since its inception has helped tens of millions of Americans access health insurance, including a record nearly 2 million Californians heading into 2026. Today, more than 24 million Americans are insured through a marketplace plan.

HARTFORD, Conn. (Oct. 30, 2025) — Access Health CT (AHCT), Connecticut’s official health insurance marketplace, today announced it will hold several enrollment fairs in November to help Connecticut residents shop, compare and enroll in health or dental coverage. They can also renew their coverage. Enrollment fairs are one-day events for customers to get in-person help from experts. The fairs will take place in Danbury, Manchester, Norwalk, Norwich, New London, Stratford and Willimantic. All help is free.

Open Enrollment begins Nov. 1, 2025 and ends Jan. 15, 2026.

When you enroll affects when your coverage starts. If customers enroll on or before Dec. 15, 2025, coverage will start Jan. 1, 2026. If they enroll between Dec. 16, 2025 and Jan. 15, 2026, coverage will begin Feb. 1, 2026.

Denver, Colo.– Health insurance premiums will increase for many people who buy health insurance through Colorado’s official marketplace and fewer customers in 2026 will qualify for financial help to offset those costs, according to a new analysis from Connect for Health Colorado, the state’s official health insurance marketplace. Most of the cost increase is the result of Congress allowing federal enhanced Premium Tax Credits (ePTCs) to expire.

Connect for Health Colorado’s analysis is based on the Colorado Division of Insurance’s announcement of final health insurance premium rates for plan year 2026, and reflects the expiration of ePTCs and the benefit of the introduction of Colorado Premium Assistance, which will reduce premiums for some customers.

On Monday I noted that around 20 state-based ACA exchange websites had launched 2026 Open Enrollment "window shopping," which allows residents to plug in their household information (zip code, ages, income, etc) and browse the various health insurance policies they have to choose from for coverage starting January 1st...as well as whatever federal (and state, in some cases) tax credits they'll be eligible for.

Last month I posted an analysis of total enrollment in ACA health insurance exchange coverage nationally which broke the data out by Congressional District partisan lean as well as according to what percent of the vote Donald Trump received a year ago.

My conclusion? Around 20% more QHP/BHP enrollees live in House districts won by Republicans than those won by Democrats last fall…but there’s still an awful lot of blue district residents who are getting hit hard.

Over 26 million Americans in BOTH red and blue districts & states are going to be screwed in the near future if the enhanced tax credits are allowed to expire & the PAPI change is kept in place, and millions of them will lose healthcare coverage completely.

Today, with Supplemental Nutrition Assistance Program (SNAP) benefits also about to be cut off to over 40 million Americans by Congressional Republicans, I decided to take a similar look at how that breaks out along partisan lines.

North Dakota has around ~43,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. I estimate they also have another ~16,000 unsubsidized off-exchange enrollees.

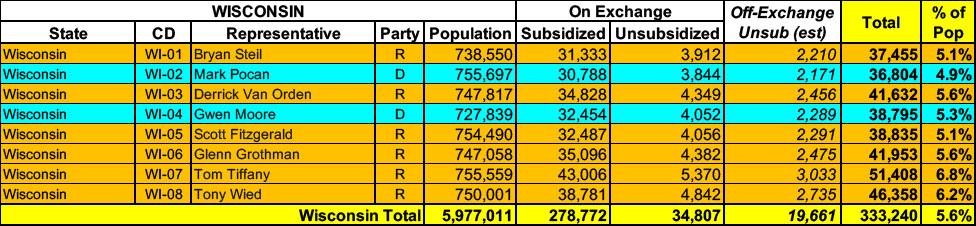

Wisconsin has around ~293,000 residents enrolled in ACA exchange plans, 98% of whom are currently subsidized. I estimate they also have another ~19,000 unsubsidized off-exchange enrollees.

West Virginia has ~67,000 residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most).

The average proposed rate increase of 12.6%, effective January 1, 2026 is expected to impact 13,677 members, based on membership as of March 31, 2025. The rate increase varies by plan, ranging between 4.4% and 20.5%. Rate changes vary by plan due to the impact of changes in benefits and rating adjustments to account for the non-funding of Cost Sharing Reduction (CSR) payments.

(unfortunately, CareSource WV's actuarial memo is heavily redacted)

Highmark BCBS WV:

Highmark West Virgina (“Highmark WV”) is requesting an average ACA individual market rate increase of 17.0%, ranging from 15.2% to 23.3%. Products submitted with this filing will have effective dates from January 1, 2026 to December 31, 2026. This rate change is projected to affect 28,179 members.

Historical Financial Experience:

Highmark WV incurred an underwriting gain in its ACA individual market programs in 2024.

(Unfortunately, BCBSND's actuarial memo is heavily redacted, so I don't know their current enrollment. I've had to make an educated guess on that; see below.)

Congressional failure to extend the enhanced premium tax credits will lead to an estimated 225,000 Coloradans seeing an average 101% increase in health insurance premiums

DENVER - The Colorado Division of Insurance (DOI), part of the Department of Regulatory Agencies (DORA), today released the final approved premium information on private health insurance plans for 2026 for the individual market (for people who don’t get coverage from an employer plan). These filings have been reviewed and updated to reflect the passage of HB25B-1006, which blunted some of the premium increases.

I've already noted that 17 states have launched window shopping for the 2026 ACA Open Enrollment Period (OEP), allowing residents of the following states to plug their household information into their states ACA exchange website to see just how much their net health insurance premiums are going to increase starting January 1st, 2026:

(Aetna/CVS is pulling out of the entire individual market nationally; I've estimated their current enrollment, see below for methodology)

AmeriHealth HMO:

AmeriHealth HMO, Inc. ("AHNJ”) is revising premium rates for the New Jersey Individual Health ACA compliant products, effective from January 1, 2026. Rate increases average 16.8%, ranging from 16.8% to 16.8%. The proposed revisions to each plan are shown on the last page of this exhibit. About 35 members will be affected.

This is the best OEP ever for the ACA for several reasons:

The expanded/enhanced premium subsidies first introduced in 2021 via the American Rescue Plan, which make premiums more affordable for those who already qualified while expanding eligibility to millions who weren't previously eligible, are continuing through the end of 2025 via the Inflation Reduction Act;

A dozen states are either launching, continuing or expanding their own state-based subsidy programs to make ACA plans even more affordable for their enrollees;

100,000 or more DACA recipients are finally eligible to enroll in ACA exchange plans & receive financial assistance!

Colorado has around ~282,000 residents enrolled in ACA exchange plans, 80% of whom are currently subsidized. I estimate they also have another ~39,000 unsubsidized off-exchange enrollees.

Annual Family Premiums for Employer Coverage Rise 6% in 2025, Nearing $27,000, with Workers Paying $6,850 Toward Premiums Out of Their Paychecks

More of the Largest Firms Cover GLP-1s for Weight Loss, and Use Is Higher Than Expected; Some May Be Limiting Coverage

Family premiums for employer-sponsored health insurance reached an average of $26,993 this year,KFF’s annual benchmark health benefits survey of large and smaller employers finds. On average, workers contribute $6,850 annually to the cost of family coverage, with employers paying the rest.

I've already noted that 14 states have launched window shopping for the 2026 ACA Open Enrollment Period (OEP), allowing residents of the following states to plug their household information into their states ACA exchange website to see just how much their net health insurance premiums are going to increase starting January 1st, 2026:

Chaos from Congressional Republicans Leads to Average Premium Increases of Over 28% for 2026

Average increases as high as 38% have been requested for the Western Slope, and insurance companies estimate nearly 100,000 Coloradans will lose their health insurance coverage

DENVER - The Colorado Division of Insurance (DOI), part of the Department of Regulatory Agencies (DORA) released the preliminary information on private health insurance plans for 2026 for the individual market (for people that don’t get coverage from an employer plan). The filings will be public once the DOI finishes the preliminary completeness review on or about Friday, July 18.

Last week I noted that thirteen states have launched window shopping for the 2026 ACA Open Enrollment Period (OEP), allowing residents of the following states to plug their household information into their states ACA exchange website to see just how much their net health insurance premiums are going to increase starting January 1st, 2026:

DIFS Encourages Michiganders to Plan for Health Insurance Coverage Now for 2026

(LANSING, MICH) The Michigan Department of Insurance and Financial Services (DIFS) is encouraging Michiganders to be ready for the upcoming Health Insurance Marketplace Open Enrollment period, which starts Nov. 1. A record 530,000 Michiganders are currently enrolled in health insurance through the Marketplace. Recent federal changes, as well as expiring tax credits, mean it has never been more important to review your insurance coverage and make a selection during the upcoming Open Enrollment period.

(Aetna/CVS announced last spring that they're pulling out of the individual market in EVERY state in 2026.)

AmeriHealth Caritas Florida:

Amerihealth Caritas Florida, Inc. (AHC) has offered comprehensive and fully insured coverage to members in the individual ACA market since 2023. AHC is filing a rate increase for 2026 products. The plans associated with this filing will be offered both on and off the Federally Facilitated Marketplace (FFM) in Florida.

Overall preliminary rate changes via SERFF database, state insurance dept. website and/or the federal Rate Review database.

Ambetter Health of LA:

The proposed rate change of 16.4% applies to approximately 97,401 individuals. Ambetter Health of Louisiana’s projected administrative expenses for 2026 are $91.51 PMPM. Administrative expense does not include $17.45 for taxes and fees. The historical administrative expenses for 2025 were $79.64 PMPM, which excludes taxes and fees. The projected loss ratio is 81.4% which satisfies the federal minimum loss ratio requirement of 80.0%.

CHRISTUS Health Plan:

(as far as I can tell, CHRISTUS is dropping out of the Louisiana individual market...they aren't listed on the federal Rate Review database website, nor do they show up in the LA SERFF filings or on the LA Insurance Dept. website.)

Merged Market Summary for Proposed Rates Effective for 2026

The following tables depict the proposed overall weighted average premium increase and the key assumptions behind premium development for the merged (individual and small employer) market filed by insurance carriers as part of the Massachusetts Division of Insurance rate review process (for rates effective in 2026). This information is subject to change as the rate review process continues.

The Health Care Access Bureau within the Massachusetts Division of Insurance is currently reviewing these assumptions. This review process will culminate in a final decision in August 2025.

There are 711,563 consumers enrolled in merged (individual/small group) market plans (data as of December 2024).

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

The Affordable Care Act premium tax credits at the center of federal shutdown discussions help almost 217,000 Washingtonians pay their monthly health insurance costs through Washington Healthplanfinder

OLYMPIA, Wash. – Washington Health Benefit Exchange CEO Ingrid Ulrey issued a statement today about Affordable Care Act tax credits that help Americans pay for health insurance, and which have become a central issue in the debate regarding the government shutdown.

“As we enter the third week of the federal government shutdown with a focus on the enhanced premium tax credits (ePTCs), it is important to remember what is at stake for Washingtonians.

“This year, these tax credits help nearly 217,000 Washingtonians afford the coverage they need for themselves and their families. If the enhanced level of these tax credits is allowed to expire, it will be people in our most rural counties, those who run small businesses or who are self-employed and older adults who are not yet eligible for Medicare who will face the steepest premium increases.

Funding supports free one-to-one assistance to residents looking for coverage through the State’s Official Health Insurance Marketplace

TRENTON — Governor Phil Murphy and New Jersey Department of Banking and Insurance Commissioner Justin Zimmerman today announced $5 million in Navigator grant awards among 30 community organizations to provide assistance in connecting uninsured residents to health coverage through Get Covered New Jersey, the State’s Official Health Insurance Marketplace, during the Open Enrollment Period and throughout the year. The 2025–2026 Open Enrollment Period starts November 1, 2025, and ends January 31, 2026.

Grant-funded Navigators will provide free, unbiased outreach, education, and enrollment assistance, in more than 10 languages in all 21 counties, to residents shopping for quality, affordable health insurance and will also assist residents in applying for financial help. Since 2019, the Murphy Administration has awarded over $28 million to fund Navigator organizations.

Just a few days ago I reported that the final, approved 2026 individual market rate filings in Michigan have been published to the SERFF database, for an overall weighted average rate increase of 20.1% marketwide:

This hasn't been officially published by the Michigan Dept. of Insurance & Financial Services yet, and technically speaking the filings aren't 100% approved yet, but 10 out of 11 filings have been moved to "complete pending form review" which I think just means that a supervisor has to give the paperwork a final once-over to make sure there are no typos etc.

*Also, Meridian Health Plan (which holds an impressive 30% of the total ACA indy market in MI when you include the carriers dropping out) is listed as "draft decision forwarded to Manager" so if any of them end up being off I'd guess it would be that one.

The average rate increase included in this filing is 19.3%, affecting over 210,000 members.

The main factors driving the need for this increase are:

Alabama market membership loss and remaining members projected to be less healthy following expiration of enhanced premium subsidies in place since 2021

Projected claim cost trends are higher for 2025 than anticipated in the 2025 filing and are projected to continue into 2026

Administrative costs increased in 2025 and are expected to rise further in 2026 due to new eligibility and billing rules, along with a higher Exchange User Fee

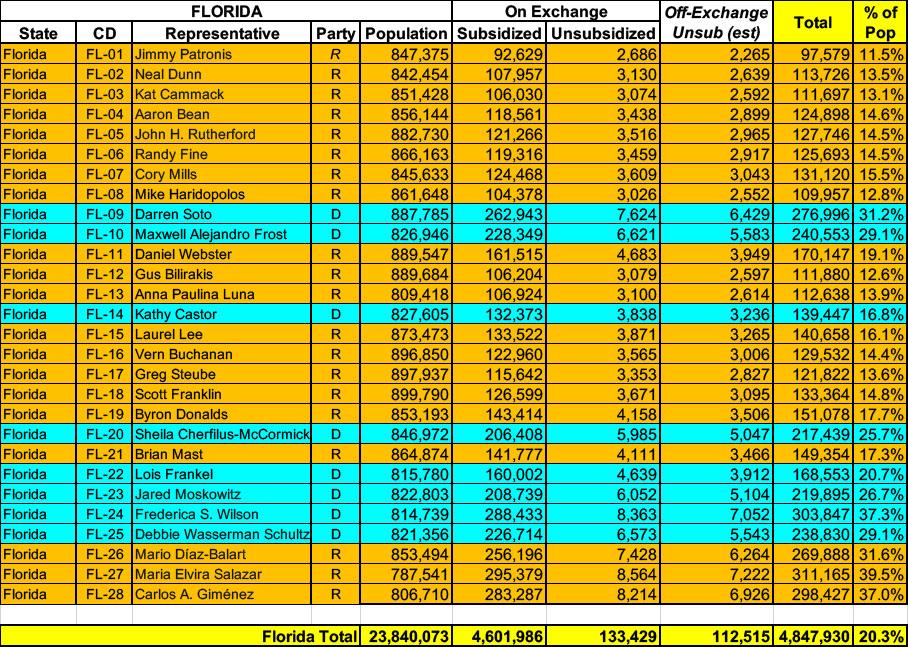

Florida has over ~4.7 MILLION residents enrolled in ACA exchange plans, 97% of whom are currently subsidized. I also estimate they have perhaps ~112,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.8 million people, or a stunning 20.3% of their total population. 1 in 5 Floridians are enrolled in ACA exchange healthcare coverage (assuming CMS's 6.6% net national attrition rate applies to Florida specifically, the actual number of current enrollees is more like 4.5 million, or 19% of the state population).

Originally posted 7/21/25; See important updates below.

It's a little awkward to try & pull quotes from Georgia's actuarial memos because they're heavily redacted (see attachments below), but fortunately I also have access to other "just the facts" filing documents which include the hard data I need to compile my weighted averages. These forms--officially called "Rate Filing Transmittal Form LH-T1" and "Unified Rate Review" forms--include, among lots of other numbers, the preliminary avg. rate change being requested for the carrier's individual (or small group) market plans, as well as the number of current effectuated enrollees they have.

In addition, I have alternate rate filings for Georgia individual market carriers which specifically state what their requested rate changes would be if the enhanced premium tax credit subsidies provided by the American Rescue Plan Act & Inflation Reduction Act were to be extended for at least one more year, providing a clear apples to apples comparison.

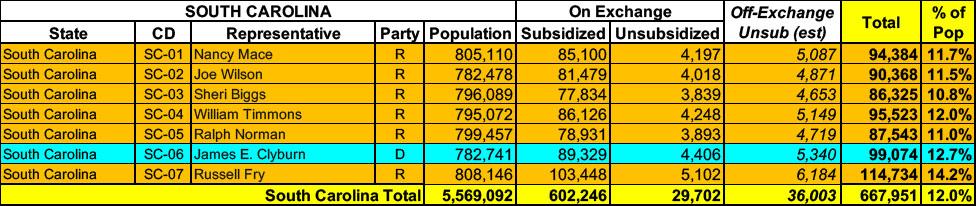

South Carolina has around ~632,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~36,000 unsubsidized off-exchange enrollees.

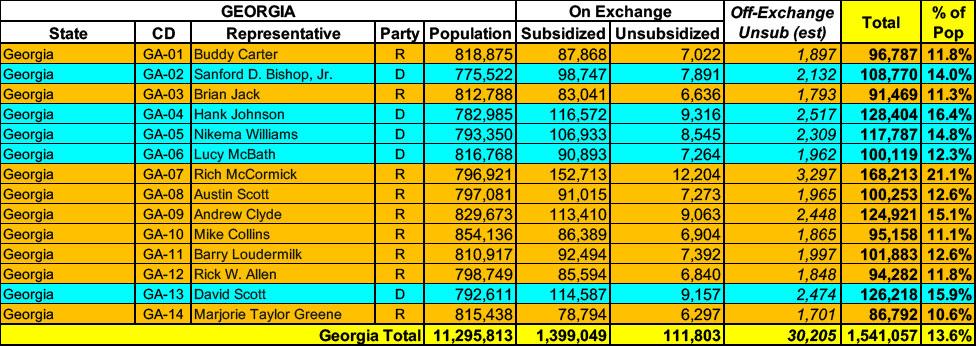

Georgia has around ~1.5 MILLION residents enrolled in ACA exchange plans, 93% of whom are currently subsidized. I estimate they also have another ~30,000 unsubsidized off-exchange enrollees.

BCN is filing a year-over-year average rate increase for 2026 for all individual products that were offered in 2025 of 16.3%. Significant contributors to rate change are outlined in the table below:

Experience Restate 4.0%

Medical and pharmaceutical price and utilization trend 5.4%

ARPA Subsidy Expiration Impact 4.6%

Benefit Change and CSR -2.6%

Margin Impact 1.2%

...Incorporated in the above, BCN assumed an additional pharmacy price trend due to tariffs, as follows:

Generic +2.5%

Brand +10%

Specialty 0%

Total Impact +2.5%

...Consistent with the 2025 filing, BCN has assumed no CSR payments will be made by the federal government for 2026. Therefore, rates for Silver plans offered on exchange are 20.5% higher than if the federal government funded CSR subsidies.

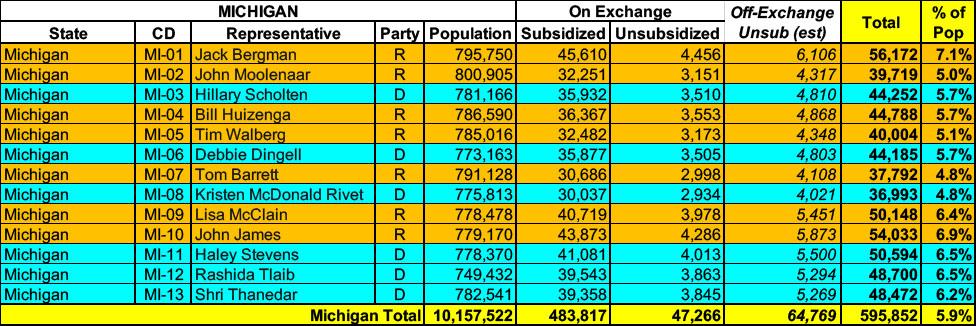

Michigan has around 531,000 residents enrolled in ACA exchange plans, 91% of whom are currently subsidized. I estimate they also have another ~64,000 unsubsidized off-exchange enrollees.

The proposed rate change of 27.3% applies to approximately 204,837 individuals. Absolute Total Care’s projected administrative expenses for 2026 are $90.21 PMPM. Administrative expense does not include $17.94 for taxes and fees. The historical administrative expenses for 2025 were $78.35 PMPM, which excludes taxes and fees. The projected loss ratio is 82.6% which satisfies the federal minimum loss ratio requirement of 80.0%.

Pennsylvanians can submit comments on rate requests and filings through September 2

Harrisburg, PA – The Pennsylvania Insurance Department (PID) today announced that the 2026 rate changes requested by insurance companies currently operating in Pennsylvania’s individual and small group markets are now available. On average, all Pennsylvania health insurers are requesting premium increases in plan year 2026: 19% increase to premiums in the individual market (for people who buy their own insurance), and a 13% increase to premiums in the small group market (for small businesses).

Last week I noted that six states have launched window shopping for the 2026 ACA Open Enrollment Period (OEP), allowing residents of the following states to plug their household information into their states ACA exchange website to see just how much their net health insurance premiums are going to increase starting January 1st, 2026:

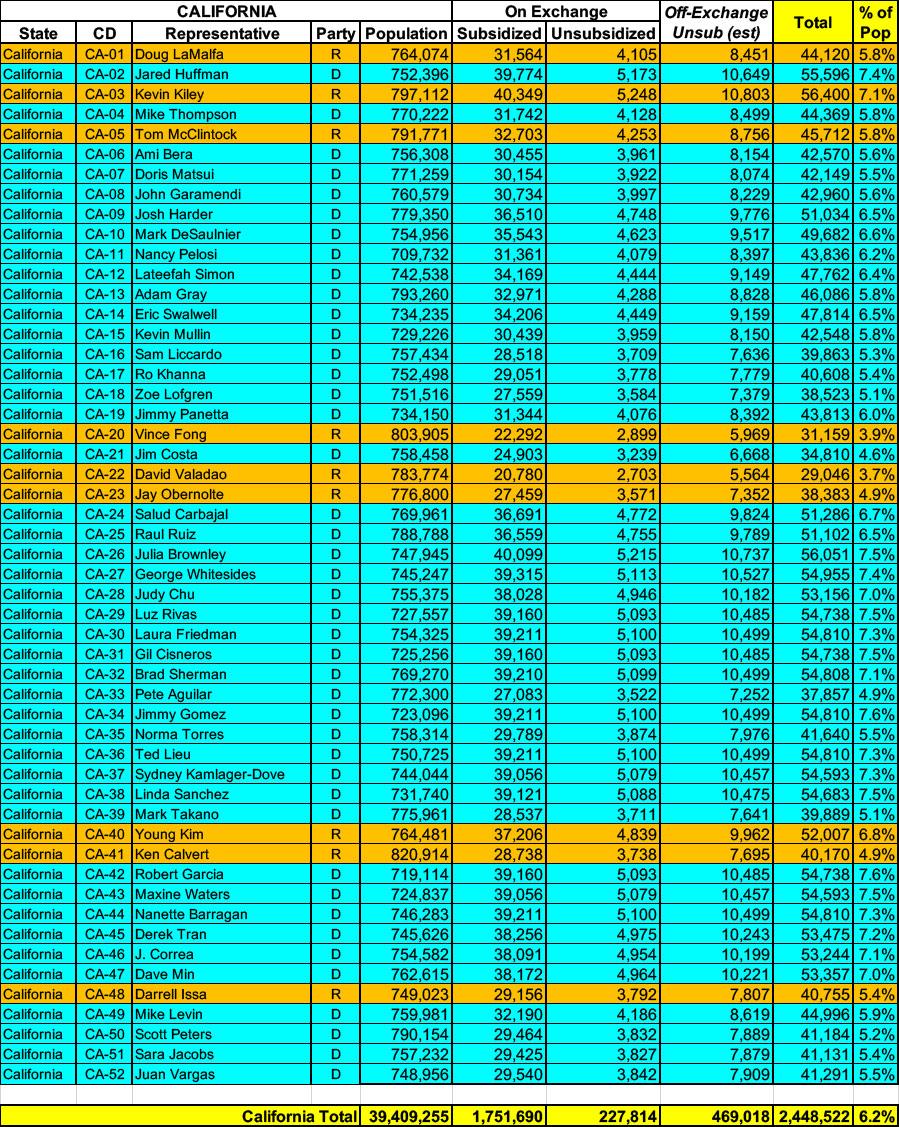

California has ~1.98 MILLION residents enrolled in ACA exchange plans, over 88% of whom are currently subsidized. They also have an estimated ~470,000 off-exchange enrollees. Combined, that's over 2.4 million people, or 6.2% of their total population.

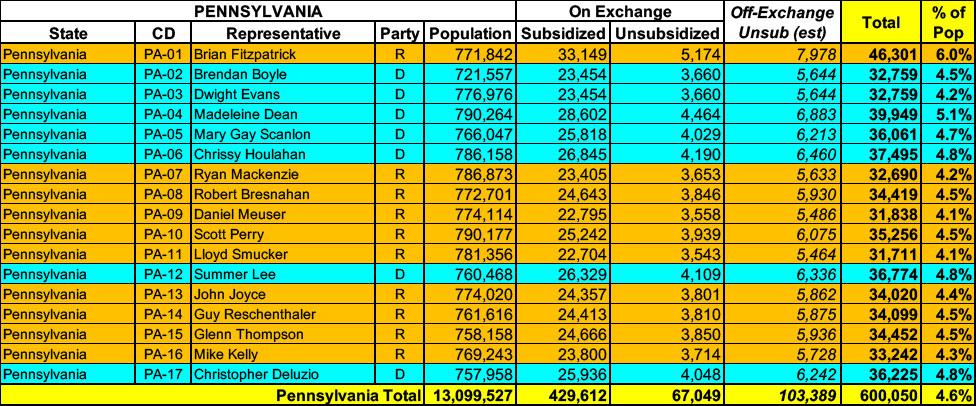

Pennsylvania has around ~496,000 residents enrolled in ACA exchange plans, 87% of whom are currently subsidized. I estimate they also have another ~103,000 unsubsidized off-exchange enrollees.

Idaho has around 117,000 residents enrolled in ACA exchange plans, 86% of whom are currently subsidized. I estimate they also have another ~9,000 unsubsidized off-exchange enrollees, although the actual rate filings (summarized later in this post) put the off-exchange total at a much higher ~47,000.

Combined, that's 6.2 - 8.0% of their total population.

Pilot expansion of ConnectorCare reshapes affordability and plan options through the Health Connector

This historic expansion allows for more access to health insurance plan choices that are both affordable and better suited to meeting an individual’s health needs

BOSTON – Today, the Massachusetts Health Connector Board of Directors approved regulatory changes that will expand access to the Marketplace’s landmark ConnectorCare program through a two-year pilot program, creating the opportunity for tens of thousands of people to access more affordable health care. The ConnectorCare program is currently available for people who make up to 300 percent of the Federal Poverty Level (FPL) and do not have access to health coverage, such as through an employer.

As anyone not under a rock for the past few months knows by now, the improved federal Affordable Care Act tax credits which were put into place by President Biden and Congressional Democrats starting in 2021 are currently scheduled to expire at the end of December, just 2 1/2 months from now.

On top of this, the Trump Regime has also made administrative regulatory changes to how the ACA is structured resulting in the remaining tax credit formula becoming even less generous yet, while also eliminating eligibility for either financial assistance or even ACA enrollment whatsoever to many other Americans.

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Banner/Aetna CVS:

(Dropping out of the individual market for 2026.)

I am writing to notify the Department that Banner Health and Aetna Health Plan Inc. (“Banner | Aetna”) will exit the individual health insurance market effective December 31, 2025. This notification is sent pursuant to Department guidance and Arizona statute 20-1380(D)(1). We made this decision after careful consideration and after evaluating the evolution of business at Banner | Aetna. The details of our individual market exit include the following:

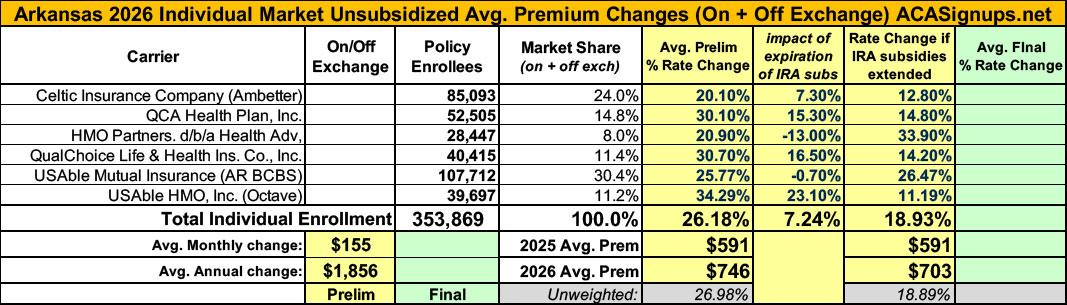

I still have the preliminary 2026 rate filings to analyze for about 10 more states, but I'm taking a break to go back and revisit ARKANSAS.

Back on July 18th, I posted my original analysis of ACA-compliant individual & small group market filings for Arkansas insurance carriers. At the time, I found that the weighted average increases being requested for individual market policies averaged a disturbingly high 26.2%. Here's what the breakout looked like:

Arkansas has around 166,000 residents enrolled in ACA exchange plans, 92% of whom are currently subsidized. I estimate they also have perhaps another ~11,000 unsubsidized off-exchange enrollees.

For many years, the District of Columbia has had among the most generous Medicaid income eligibility thresholds in the country, with children and pregnant women in households earning up to 324% of the Federal Poverty Level (FPL) being eligible as well as parents earning up to 216% FPL and childless adults earning up to 210% FPL*. As a result, nearly 37% of DC's total population is enrolled in Medicaid.

Oregonians continue to have at least five health insurance companies to choose from in every Oregon county as companies file 2026 health insurance rate requests for individual and small group markets

In-depth rate review process just beginning, opportunities for public review and input remain through June 20

June 2, 2025

Oregon health insurers have submitted proposed 2026 rates for individual and small group plans, launching a months-long review process that includes public input and meetings.

Five insurers will again offer plans statewide (Moda, Bridgespan, PacificSource, Providence, and Regence), and Kaiser is offering insurance in 11 counties, giving six options to choose from in various areas around the state.

(sigh) OK, I'm not sure if we've reached the 5th or 6th chapter in this ongoing saga, but I hope it's the last one.

When we last left our story (just 5 days ago), I noted that both the current number of enrollees as well as the average rate increases for each of the carriers on the Arkansas individual market had jumped all over the place at least 4 times, and that while it's common for these numbers to change a bit here and there throughout the multi-month filing process, both the degree of some of the changes as well as the circumstances surrounding them were often far beyond what I've typically seen in over a decade of tracking this stuff:

Given all the confusing numbers I've posted before, I've boiled it all down to the simplified tables below which illustrate the mess:

New Mexico has around ~70,000 residents enrolled in ACA exchange plans, 85% of whom are currently subsidized. I estimate they also have another ~8,000 unsubsidized off-exchange enrollees.

I already wrote about this over a month ago but it didn't get the attention it deserved at the time, and given that we're much closer to the actual 2026 ACA Open Enrollment Period starting and that there's been another important development since then, I figured I should post an updated entry about it.

Santa Fe, NM – The New Mexico Office of the Superintendent of Insurance (OSI) has approved 2026 rates for individual market Affordable Care Act (ACA) plans sold on and off BeWell, the New Mexico Health Insurance Marketplace, with an average increase of 35.7%. Today, 75,000 New Mexicans buy health insurance through BeWell and 88% of enrollees qualify for federal and state premium assistance.

With the 2026 ACA Open Enrollment Period officially starting on November 1st, and with millions of ACA enrollees being bombarded with scary letters from their insurance carriers and headlines warning of massive premium hikes, residents of six states* (as of this writing) can already enter their own household information to find out how much their net health insurance premiums are going to increase starting January 1st, 2026:

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of June 2025:

Twelve years ago, the Wall St. Journal ran a story about the impact of the American Taxpayer Relief Act of 2012, a sweeping tax bill signed into law by President Obama which locked in the Bush tax cuts for lower & middle-class households while allowing them to expire on schedule for wealthier Americans:

A compromise measure, the Act gives permanence to the lower rate of much of the Bush tax cuts, while retaining the higher tax rate at upper income levels that became effective on January 1 due to the expiration of the Bush tax cuts. It also establishes caps on tax deductions and credits for those at upper income levels. It does not tackle federal spending levels to a great extent, rather leaving that for further negotiations and legislation. The American Taxpayer Relief Act passed by a wide majority in the Senate, with both Democrats and Republicans supporting it, while most of the House Republicans opposed it.

(Aetna/CVS is pulling out of the entire individual market nationally)

Anthem Blue Cross of CA (DMHC)

This is a rate filing for the Individual market ACA‐compliant plans offered by Anthem Blue Cross (Anthem). The proposed rates in this filing will be effective for the 2026 plan year beginning January 1, 2026, and apply to plans both On‐Exchange and Off‐Exchange.

Anthem will continue to participate in its 2025 marketplace footprint consisting of rating areas 1-10 and 12-14 with EPO plans and rating areas 11 and 15‐19 with HMO plans.

The projected average rate change for plans effective January 1, 2026 is 16.0% which is an average rate change of about $87 per member per month (pmpm). Because 16.0% (or about $87) is an average, it is possible to have a different rate change. Factors affecting a member's premium are age, tobacco use, family composition, plan, and geographic area. Expected cost differences by product are updated every year to ensure premium differences are appropriate. BridgeSpan has approximately 200 members enrolled in this line of business as of March 2025.

...The rate change described above is driven by the following factors:

Medical Trend : 9.1%

Change in Benefits, Age, Area, and Network : -1.5%

Change in Market Morbidity : 5.0%

Exchange User Fees : 1.0%

Other : 2.0%

Other includes: actual results vs. expected, changes to admin expenses, and rx rebates. Actual results vs. expected reflect differences between actual results and past assumptions, including a true-up of market morbidity estimates

In the most recent chapter of the ongoing 2026 Arkansas rate filing saga, I noted that both the total number of residents enrolled in ACA individual market policies as well as the average 2026 rate increases for the six insurance carriers participating in the individual market next year kept changing, often in ways which were contradictory with other numbers claimed within the same press releases:

You'll notice that in addition to the rate changes being updated (increasing from a weighted average hike of 26.2% to 35.7%), most of the current enrollee figures were also modified, although these only changed slightly in most cases. Overall the total number of current individual market enrollees statewide dropped a bit from ~354,000 to ~345,000.

Minor changes like this aren't unusual; sometimes the carriers make slight tweaks as more recent data comes in or clerical errors are corrected; other times they round off the enrollee totals (that doesn't seem to be the case here, however).

Iowa Code §505.19 requires the Commissioner to hold a public hearing on a proposed individual health insurance rate increase which exceeds the average annual health spending growth rate as published by the Centers for Medicare and Medicaid Services of the United State Department of Health and Human Services. For 2026 the growth rate is 5.6%.

The Iowa Insurance Commissioner will hold a public hearing regarding the relevant rate increases on August 19, 2025.

The purpose will be to hear public comments on the proposed increase in the base premium rate. Consumers wishing to make a public comment at the hearing are encouraged to attend the hearing via the live webcast.

All comments received will be considered public records and will be posted here. The Consumer Advocate will present the public comments received at the hearing.

Iowa has around 136,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. I estimate they also have another ~9,600 unsubsidized off-exchange enrollees.

Every year, I spend months painstakingly tracking every insurance carrier rate filing (nearly 400 for 2025!) for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

I really only need three pieces of information for each carrier:

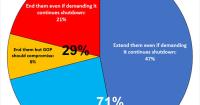

A Washington Post poll conducted on Oct. 1, the first day of the shutdown, found that 47% of U.S. adults blame Trump and Republicans in Congress, while 30% blame Democrats and 23% said they're not sure.

The survey found that independents blamed Trump and Republicans over Democrats by a wide margin of 50% to 22%. And one-third of Republicans were either unsure who to blame (25%) or blamed their party (8%).

Federal subsidies that reduce the cost of Affordable Care Act health insurance plans are scheduled to end at the end of this year. Should these subsidies...

Federal policy shifts drive higher 2026 rates for individual and small group health plans

State actions blunt increases tied to the reconciliation bills and policy direction of the federal government

St. Paul, MN: Health insurers have submitted their proposed increased rates to the Minnesota Department of Commerce for 2026 plans available to Minnesotans who buy individual or small group health insurance through MNsure or directly through insurers. These proposed rates apply to coverage starting Jan. 1, 2026, with open enrollment beginning Nov. 1, 2025.

The Department of Insurance receives preliminary health plan information for the following year from insurance carriers by June 1 and reviews the proposed plan documents and rates for compliance with Idaho and federal regulations.The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

{kind=link}