Arkansas: Where the hell is Huckabee Sanders getting these numbers??

Wed, 09/24/2025 - 2:38pm

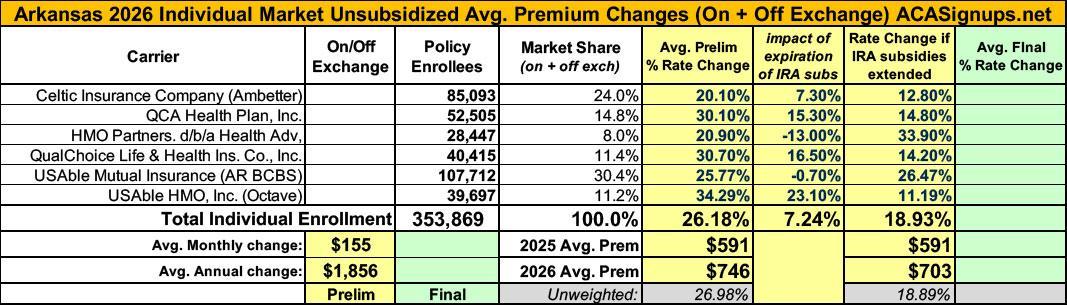

Back in July I posted my analysis of the preliminary 2026 rate filings by the 6 Arkansas insurance carriers participating in the individual market. At the time, they looked like this:

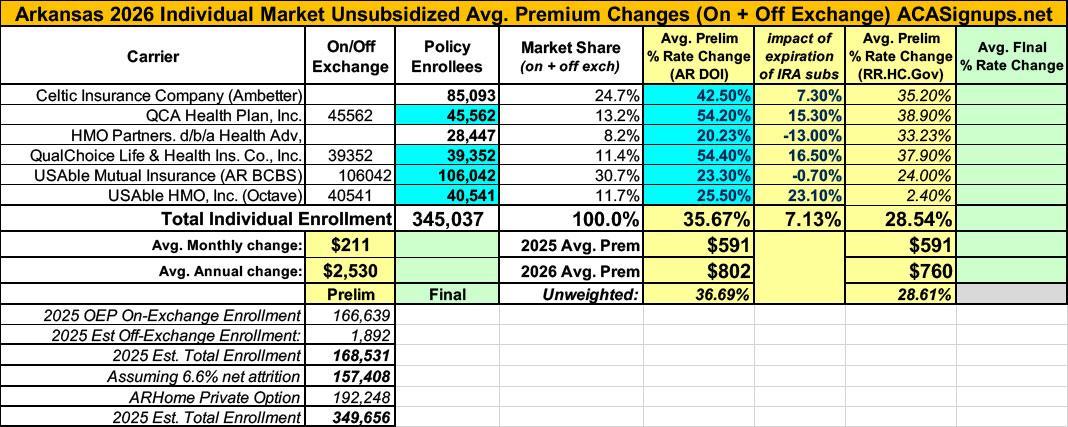

A few weeks later, however, the carriers refiled for 2026 with dramatically higher premium increase requests, like so:

You'll notice that in addition to the rate changes being updated (increasing from a weighted average hike of 26.2% to 35.7%), most of the current enrollee figures were also modified, although these only changed slightly in most cases. Overall the total number of current individual market enrollees statewide dropped a bit from ~354,000 to ~345,000.

Minor changes like this aren't unusual; sometimes the carriers make slight tweaks as more recent data comes in or clerical errors are corrected; other times they round off the enrollee totals (that doesn't seem to be the case here, however).

When the higher filings were published, Arkansas Governor Sarah Huckabee Sanders issued something of a public temper tantrum over it, declaring that...

“Arkansans are tired of getting outrageous bills from multi-billion-dollar insurance companies, and my administration will not allow them to take advantage of our people. Nothing justifies year-over-year premium increases of this scale – it’s wrong and prohibited under Arkansas law.

“Arkansas’ Insurance Commissioner is required to disapprove of proposed rate increases if they are excessive or discriminatory, and these are both. I’m calling on my Commissioner to follow the law, reject these insane rate increases, and protect Arkansans.”

By sheer coincidence (?), the Arkansas Insurance Commissioner, Alan McClain, announced his resignation on the same day, and was replaced by a man named Jimmy Harris.

Cut to a few weeks ago, when I reported that a local reporter, Benjamin Hardy, had used FOIA requests to acquire internal email correspondence within the AR Insurance Dept. & Commerce Dept. showing that the state plans on responding to the impending expiration of the enhanced ACA premium tax credits in a very positive way: By implementing a robust Premium Alignment policy to maximize the effectiveness of the remaining federal subsidies:

Earlier this year, Bulletin 4-2025 was issued by the Arkansas Insurance Department that provided standardized guidance on the application of the silver load. In previous years, the amount of this load was determined by each insurer, based on their individual experience. This standardized guidance will protect access to zero-premium and lower deductible plans for low- and middle-income individuals by ensuring remaining federal subsidies go where they are most effective for Arkansans.

In my most recent post I gave full credit & praise where due to the Arkansas Insurance & Commerce Depts for doing this; maximized Premium Alignment (which includes but isn't limited to robust Silver Loading) is something I and other healthcare wonks have been pushing every state to do for several years now, and I'm glad to see that Arkansas is joining nearly a dozen other states in implementing this practice.

HOWEVER, I also went on to note that some of the other language and claims being presented (again, internally only for now) within the Arkansas state agencies was either confusing, questionable or both. In particular:

- They may be overstating the positive impact of implementing Premium Alignment compared to the current pricing methodology; and

- They're definitely understating the number of current ACA enrollees who will be negatively impacted by the lost federal subsidies by a massive amount.

The short version of the second point is this:

- Total individual market enrollment: ~350,000 (give or take)

- Of this, around 180,000 are enrolled in the state's ARHOME "Private Medicaid Option" program & aren't part of this equation (actual ARHOME enrollment in ACA plans was 191,000 as of May, but I'm willing to give them the benefit of the doubt on this one)

- This leaves ~170,000 or so actually enrolled in ACA individual market policies impacted by the upcoming rate changes.

- However, the AR Insurance Dept. (AID) only lists this figure as being around 80,000.

The logic of AID seems to be that the other 85K or so enrollees will be priced completely out of the market and therefore "don't count" as seeing their premiums increase, which is a pretty novel logical leap.

To be clear, I'm not certain that this is what they're doing, but I've yet to hear any other explanation as to why they're simply leaving out over 50% of the current enrollees in their pitch.

In any event, that's where I left this saga...until today.

A few days ago, Hardy, the Arkansas Times reporter who dug up the internal emails, published his own story on the issue, which, in addition to going into some detail about Silver Loading & Premium Alignment as well as the curious "missing" ~85,000 enrollees, includes some additional eyebrow-raising elements:

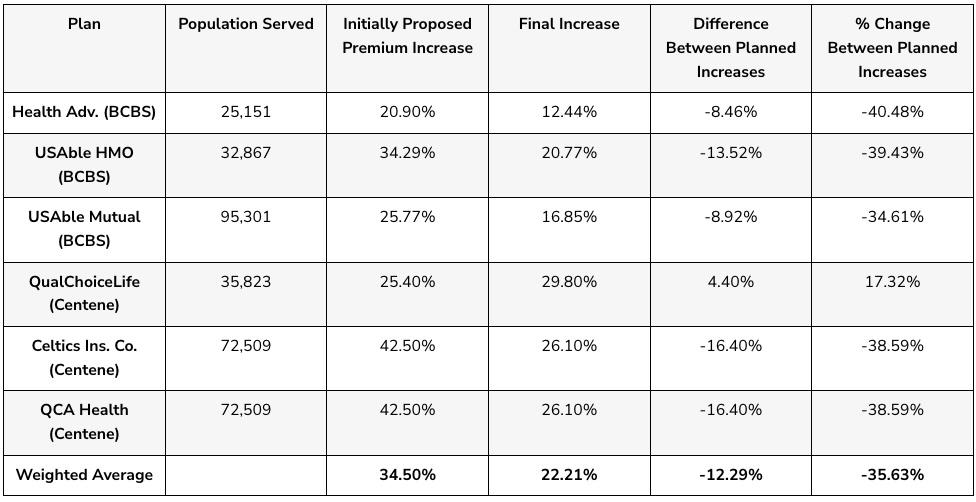

On Friday morning, Gov. Sarah Sanders said she had “secured average rate increases that are 35.8% lower than previously proposed” from BlueCross and Centene, the two insurance companies that sell plans on the Arkansas Health Insurance Marketplace. (The marketplace is how people who aren’t covered through an employer, family member, or Medicaid typically buy health insurance.)

Sanders, who publicly slammed BlueCross and Centene in August for proposing “insane” 2026 rates (an average hike of 36%), claimed this as a victory for Arkansans. “More work remains, but this is a good starting point and shows that when we stand up to insurance companies, we can win tangible benefits for the people of our state,” she said.

But that 35.8% price reduction she touted? That’s simply a comparison to the initial proposal from insurers back in August. What ultimately matters to Arkansas health insurance consumers is the price bump that remains: The average premium increase next year will still be more than 22%, according to a chart included in the governor’s statement.

So far, this is normal spin: A bit misleading but technically accurate: The carriers were asking for a ~36% bump but she's taking credit for knocking that down to "only" 22.2%. Fair enough.

HOWEVER...there's a couple of major problems with Sanders' bold proclamation which go beyond spinning a huge rate hike as a rate reduction. As Hardy notes:

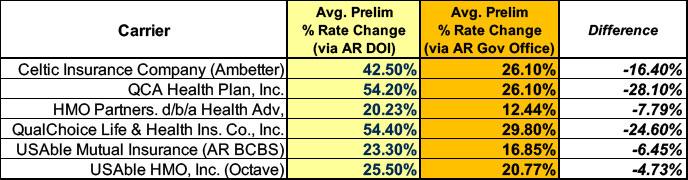

Muddying the waters further, there’s something peculiar about the numbers in the chart from Sanders’ office: The “initially proposed” increases aren’t the same figures as the ones released to the public in August by the Insurance Department.

Both the governor’s office figures released Friday and the insurance department figures released in August are expressed in topline numbers for each of six carriers (all of which are owned by either Centene or Blue Cross). Five of the six numbers listed in the governor’s chart are different (higher or lower) than those released by the insurance department in August, sometimes dramatically so (one changed by 29 percentage points).

Here's what's currently displayed on the actual AID website as of today:

...and here's the chart published as part of Gov. Sanders press release:

The order of the filings is different, so here's what they look like side by side:

Now, if the reduced rate filings are the final ones, then yes, it would be good news. However...

It’s unclear how the governor’s new numbers might have been calculated. The governor’s office has not responded to queries, so there is simply no way to know where the figures are coming from. Strangely, the governor’s press release referred to one eye-popping increase (54.2%) that was listed on the August insurance department release but not in the governor’s own figures. It’s a mystery.

Not only is there no source for the lower rate hikes shown in the Sanders' chart, but the enrollment numbers ("Population Served" in her chart) don't make any sense either.

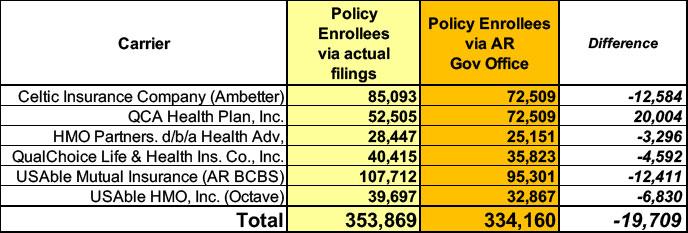

Here's the actual carrier filing enrollment numbers side by side with what Sanders claims in her press release:

As I noted earlier, there's often some slight tweaks to the estimated enrollment numbers by the carriers over the course of the filing process...but the numbers put out by Gov. Sanders don't seem to show up anywhere in the actual carrier filings, nor do they show up on the Arkansas Insurance Dept's own website.

Furthermore, take a closer look at Celtic/Ambetter and QCA Health Plan: Not only does Sanders claim that both carriers are increasing premiums by exactly the same amount (26.10% each), she also claims that both carriers have identical numbers of enrollees (exactly 72,509 apiece).

This is, to put it mildly, highly unlikely...especially since in order for this to be true, QCA would have to have mysteriously increased their enrollment by 20,000 people (over 38% more!) at the same time that all 5 of the other carriers saw theirs drop significantly.

On top of this, take a look at this section of Sanders' press release:

The six health plans included in this announcement are managed by Centene and Arkansas Blue Cross Blue Shield and are available on the federally managed healthcare exchange established by the Affordable Care Act. They cover 308,662 Arkansans.

Huh??? Where the hell does she get that number from? That's over 45,000 fewer than the carriers themselves say they have enrolled, and it's even over 25,000 fewer than the total included in the press release's chart itself!

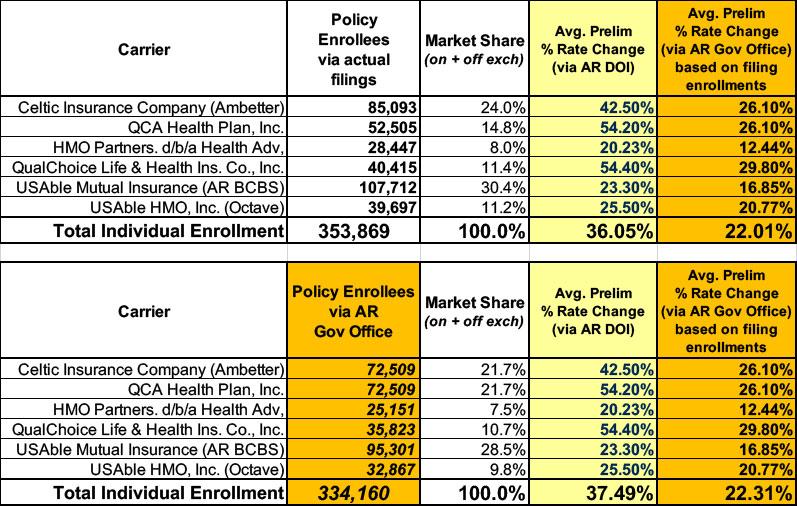

But wait, there's more! Take a look at that "Final Increase Weighted Average" at the bottom of Sanders' chart: +22.21%.

I've tried plugging in the numbers all four ways (using either the carriers or Sanders' rate hikes and using either the carriers or Sanders' enrollment figures) and none of them come out to 22.21% (although one does come close, at 22.31%):

Normally I wouldn't make a big deal about a press release's claimed figure being off by a few tenths of a percentage point, but given how unlikely & confusing some of the other numbers surrounding it are, it's one more red flag for me in this case.

What makes this mess especially puzzling is that, as I noted in my previous Premium Alignment post, the state insurance & commerce dept. commissioners seem to be making an honest effort to minimize the massive damage about to be caused to ACA enrollees across Arkansas, so I don't think that they're trying to cook the books or whatever here.

As for Gov. Sanders herself, I don't know if this is part of a deliberate attempt to obfuscate the situation or simply a case of rushed press release to generate positive PR, but it's pretty unflattering either way.

The irony is that if she had simply waited another week until the actual 2026 rate filings were locked in and then promoted the Premium Alignment action instead, that would have been something she could honestly have been proud of her administration for doing.

Instead, by apparently jumping the gun and posting this sloppy, confusing mess of a press release, she seems to have stepped on her own foot.

Advertisement