Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of August 2025:

Total Medicare beneficiaries are up to 69.3 million (up ~86K month over month)

Traditional/FFM Medicare beneficiaries are at 33.79 million (down ~31K m/m)

Medicare Advantage beneficiaries reached 35.49 million (up ~55K m/m)

11.73 million Medicare enrollees (around 16.9% of the total) were "Dual Eligibles"...that is, enrolled in both Medicare and Medicaid.

The only number which seems odd is the 375K drop in Dual Eligibles...I'm not sure what to make of that.

I recently joined Ana Marie Cox & Open Mike Eagle on the Past Due Podcast to discuss the how to deal with this year's crazy ACA Open Enrollment Period. Tune in!

Yesterday, Politico reported that the Trump 2/3 White House was planning on rolling out his own counterproposal to Democrats demand that the enhanced ACA tax credits (which are still scheduled to expire just 36 days from now) be extended (preferably permanently, but at the bare minimum by at least a few years).

According to the Politico story, the Trump proposal supposedly included the following provisions:

Via Politico this morning, a mixed bag of good & bad news on the enhanced ACA tax credit saga today:

The White House expects to soon unveil a health policy framework that includes a two-year extension of Obamacare subsidies due to expire at the end of next month and new limits on eligibility, according to three people granted anonymity to discuss the unannounced plans.

...The White House plan is expected to include new income caps for enrollees to qualify for the ACA tax credits as well as minimum premium payments, according to the two people with direct knowledge of the proposal.

The planned eligibility cap would limit the subsidies to individuals with income up to 700 percent of the federal poverty line — aligning with what a bipartisan group of senators have been discussing separately, according to a fourth person granted anonymity to share knowledge of the negotiations.

At a bare, bare minimum, do not settle for a one- or two-year extension of the eAPTCs.

Kicking this particular can down the road for only one or two years would not only be an absolute gift to Republicans politically (since it would push the pain out until just past the midterms, which is of course the only reason why any Republicans are willing to discuss doing so at all), but it would also mean we'd be right back here with the exact same scary headlines a year or two from now, with 24 million people never knowing whether their health insurance premiums are going to skyrocket from year to year.

Nothing is worse for the insurance industry than uncertainty, and anytime they're uncertain about anything you can be sure they'll jack up rates as a "just in case" cushion.

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2026. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin coverage. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2026 is December 15, 2025. Consumers who select a plan between December 16, 2025 and January 15, 2026 will have coverage beginning February 1, 2026.

In my post about the U.S. Senate vote to end the federal government shutdown last week, I concluded that:

I'll have a lot more to say about this "HSAs for All" silliness which Trump & Sen. Cassidy are suddenly pitching, but in the meantime, whether you think 8 of them voting for the CR Sunday night was the right thing to do or not, once they did so, shifting the national dialogue back to healthcare policy (where Dems are strongest and Republicans are weakest) and the Epstein Files is probably the best outcome Democrats could've realistically hoped for from that point forward.

Almost every day since the, various Republican House & Senate members have underscored my point:

ST. PAUL, Minn.—MNsure, Minnesota’s official health insurance marketplace, assures UCare members that their health plans through MNsure will not change in coverage or cost for plan year 2026.

Medica has announced a definitive agreement to acquire individual and family health plans from UCare, a Minnesota-based nonprofit health plan. This is a change for the individual market, but MNsure assures consumers that their coverage remains unchanged and will not be interrupted.

For consumers who are currently enrolled in a 2025 UCare private plan:

There are no changes to coverage.

They can continue to access care as usual.

As long as they have paid their premiums, current coverage goes through December 31, 2025.

For consumers who have selected a 2026 UCare private plan through MNsure:

Americans for a Balanced Budget released the findings of a national survey of 800 likely voters on November 18, 2025, conducted by pollster John McLaughlin of McLaughlin & Associates, across 16 GOP-held battleground districts rated Toss Up or Lean Republican by the Cook Political Report.

A haruspex was a person trained to practice a form of divination called haruspicy in the religion of ancient Rome, the inspection of the entrails of sacrificed animals, especially the livers of sacrificed sheep and poultry.

I realize I'm a little late to the party on this, but nine days ago, Donald Trump posted one of his online rants in response to the then-ongoing government shutdown standoff in the U.S. Senate, which was primarily focused on the imminent expiration of enhanced ACA tax credits:

In all the (understandable) panic & controversy over the enhanced ACA tax credits expiring just 6 weeks from today, I wanted to take a quick moment to note that the 2026 Medicare Parts A & B Premiums & Deductible increases have been formally published by the Centers for Medicare & Medicaid Services:

On November 14, 2025, the Centers for Medicare & Medicaid Services (CMS) released the 2026 premiums, deductibles, and coinsurance amounts for the Medicare Part A and Part B programs, and the 2026 Medicare Part D income-related monthly adjustment amounts.

Medicare Part A Premium and Deductible

Medicare Part A covers inpatient hospital, skilled nursing facility, hospice, inpatient rehabilitation, and some home health care services. Approximately 99% of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment, as determined by the Social Security Administration.

I was up to my ears in data crunching over the entire weekend working on my deep dive into the 14 states with Premium Alignment pricing in place for 2026, so I haven't had a chance to chime in on Sunday evening's Continuing Resolution vote in the U.S. Senate until now.

After enough of them held out for 40 days and 14 votes (I think) to prevent the House Republican version of the CR bill from passing & the federal government from re-opening, 7 Democratic Senators and 1 Dem-caucusing Independent finally agreed to vote for a modified Senate version of the bill...none of whom, by what I'm sure is sheer coincidence, are up for re-election next year (2 are retiring; the other 6 aren't up again until either 2028 or 2030, and one of them will likely retire before then anyway).

NEW YORK – New York Attorney General Letitia James and Department of Health (DOH) Commissioner Dr. James McDonald today issued a consumer alert warning New Yorkers about common health insurance scams as 2026 open enrollment begins through the NY State of Health Marketplace. Health insurance scams spike during open enrollment periods, and the Office of the Attorney General (OAG) and DOH are providing consumers with tips to protect themselves against potential scams.

“As health care costs skyrocket and federal support hangs in the balance, access to affordable health insurance is more important than ever,” said Attorney General James. “We cannot allow predatory scammers to swindle New Yorkers out of their hard-earned money. I urge all New Yorkers to remain vigilant and contact my office if they believe they are the target of a scam or fraud. My office will always work to hold bad actors and fraudsters accountable.”

New Mexico Open Enrollment 2026 - Enrollment Summary

Last Refreshed On: November 12th 2025

Officially, they're reporting 70,485 Qualified Health Plan (QHP) enrollments already, which is actually slightly higher than the 70,373 which they ended with during the 2025 Open Enrollment Period (OEP) last January.

HOWEVER...and this is a major caveat...that 70,485 includes all current enrollees being auto-renewed for 2026, which doesn't really count for my purposes. Most state exchanges used to hold off on lumping in the auto-renewals until after the initial December deadline, only reporting current enrollees who actively re-enroll along with new enrollees.

IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

SACRAMENTO, Calif. — Covered California Executive Director Jessica Altman issued the following statement on Speaker Emerita Nancy Pelosi’s announcement of her retirement on Thursday:

“After nearly four decades of unmatched public service, Speaker Emerita Pelosi leaves behind a legacy that continues to affect the lives of millions of Americans every day.

“Speaker Emerita Pelosi was one of the architects of the Patient Protection and Affordable Care Act and the driving force in making sure the landmark legislation became the law of the land in 2010.

“She was again the speaker of the House when the current Enhanced Premium Tax Credits were passed in 2021, further bringing down costs for consumers and making health insurance more affordable and accessible to more Americans than ever.

“Thanks to the speaker emerita’s tireless efforts, enrollment in Affordable Care Act marketplaces has more than doubled nationwide and currently provides health care coverage to over 24 million Americans, including nearly 2 million here in California.

Nevadans can now enroll in health insurance for 2026: 140 Qualified Health Plans from eight insurance carriers and new Battle Born State Plans for Nevadans to choose from

CARSON CITY, Nev. (November 3, 2025) – On November 1, Nevada Health Link kicked off the Open Enrollment Period for Plan Year 2026 with 140 Qualified Health Plans through eight brand-name private insurance carriers, including the new state-approved Battle Born State Plans (BBSPs). Nevadans can view, compare and shop plans now through January 15, 2026 on NevadaHealthLink.com.

New this year, Nevada Health Link will offer Battle Born State Plans or BBSPs.

Like all plans on the Marketplace, BBSPs will cover all ten essential health benefits, including hospitalization, doctor visits, emergency care, lab work and prescription drugs. These plans are required to be offered statewide, while also meeting specific reduction targets to bring costs down. This is especially significant for Nevadans living in rural areas, who will have more options this year when selecting a plan.

New “Yes, NY” Campaign Encouraging New Yorkers to Enroll in Quality, Affordable Health Coverage

Open Enrollment for 2026 Qualified Health Plans Began November 1 and Ends January 31, 2026

Enhanced Dental Benefits Introduced for 2026

ALBANY, NY (November 6, 2025) – The New York State Department of Health today announced the start of Open Enrollment for 2026 health insurance coverage through NY State of Health, the Official Health Plan Marketplace, launching a new statewide “Yes, NY” campaign to encourage New Yorkers to enroll in affordable, high-quality health coverage. Open enrollment runs from November 1, 2025, to January 31, 2026.

Amid federal health care changes negatively impacting Americans, Get Covered Illinois is here to help.

CHICAGO – Get Covered Illinois kicked off 2026 open enrollment and launched its “Here to Help” campaign across the state.

Open enrollment, which began on November 1 and runs through January 15, is the annual opportunity for Illinoisans to enroll in, renew, or change their health insurance plans. Nearly 466,000 Illinoisans purchased health coverage through Get Covered Illinois during open enrollment last year, a 17% increase from the previous year.

This year, Illinoisans will experience a new marketplace. Enrollees will apply for and enroll directly on GetCoveredIllinois.gov now that Illinois has officially transitioned to a state-based marketplace. They will also have access to increased support that is more tailored to their needs.

I've written multiple times in the past about "Silver Loading," the ACA health insurance policy pricing strategy in which insurance carriers load the extra cost of their Cost Sharing Reduction financial burden (the portion of deductibles, co-pays & coinsurance which they're required to cover themselves for low-income enrollees who select Silver plans) onto the gross premium of those same Silver plans.

It gets a bit wonky, but the bottom line is that Silver Loading results in the gross price of Silver ACA plans increasing significantly even if the price of Bronze, Gold & Platinum plans only go up modestly. This may sound bad, but stay with me.

From the carriers perspective, how the CSR load is allocated doesn't matter much as long as they aren't left stuck with the bill...but pricing the plans in this fashion has major implications for the enrollees themselves.

Wyoming has ~46,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees (likely only a few thousand at most). Combined, that's around 8% of their total population.

(Note, however, that the official actuarial rate filings for the 3 carriers offering coverage in the Wyoming individual market only report a combined total of around 39,000 enrollees as of spring 2025, or 6.6% of the total population).

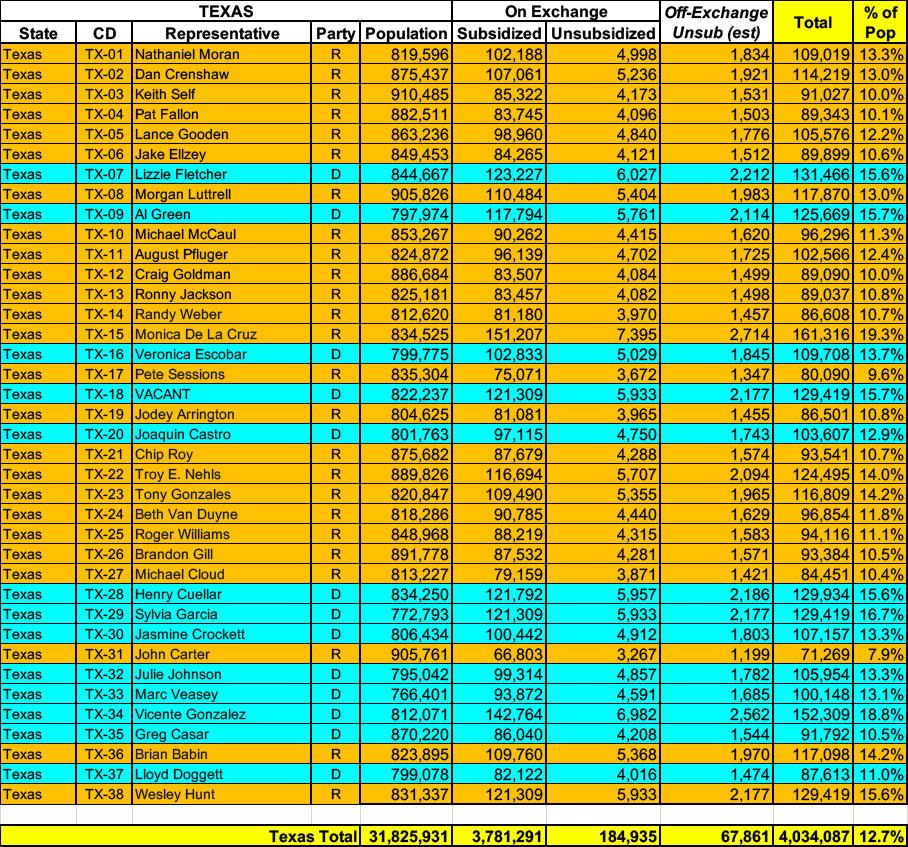

Texas has ~3.9 MILLION residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have perhaps ~67,000 unsubsidized off-exchange enrollees.

Combined, that's over 4.0 MILLION Texans, although although assuming the national average 6.6% net enrollment attrition rate applies, current enrollment would be back down to more like ~3.8 million statewide.

Blue Cross Blue Shield of Wyoming (BCBSWY) has offered comprehensive and fully insured coverage to members in the Individual ACA market since 2014. BCBSWY is filing a rate increase for 2026 products. All plans will be offered statewide; plans with be offered either on or off the Federally Facilitated Marketplace in Wyoming.

(Access to Care Health Plan is a division of Sendero; unfortunately, they've heavily redacted their actuarial memo and I can't find a justification summary)

Aetna Health:

Aetna is dropping out of the individual market nationally in 2026. In texas, they've provided a market withdrawl letter which includes the exact number of current enrollees in each region of the state:

"Aetna is totally withdrawing from the individual (off and on-exchange) market, effective December 31, 2025. Individuals currently covered under an Aetna plan will need to make a different plan selection for 2026. In accordance with Texas and federal law, consumers will be given 180 days’ notice of the termination of their policy."

Initial Affordable Care Act Rates for 2026 have been posted

The North Carolina Department of Insurance has posted the rate changes requested by insurers for the 2026 plan year individual and small-group market plans offered under the Affordable Care Act.

Posting of the requested rates is part of the rate review process required by the Centers for Medicare and Medicaid Services (CMS). Unlike some types of insurance, the NCDOI does not set rates for health insurance.

Tennessee ACA exchange carriers were instructed to provide two sets of rate filings for 2026: One which assumes CSR reimbursement payments won't be reinstated, one which assumes they are reinstated. In addition, both sets of filings assume that IRA subsidies won't be extended; all but one carrier clarified how much extending the IRA subsidies would impact 2026 premium changes.

Alliant Health Plans: Alliant is requesting a nominal 0.3% increase next year if CSR payments aren't reinstated and a 1.0% drop if they are. In both cases, premiums would be 2.8% lower if IRA subsidies were to be extended by Congress:

Mississippi has around ~338,000 residents enrolled in ACA exchange plans, 98% of whom are currently subsidized. I estimate they also have another ~14,000 unsubsidized off-exchange enrollees.

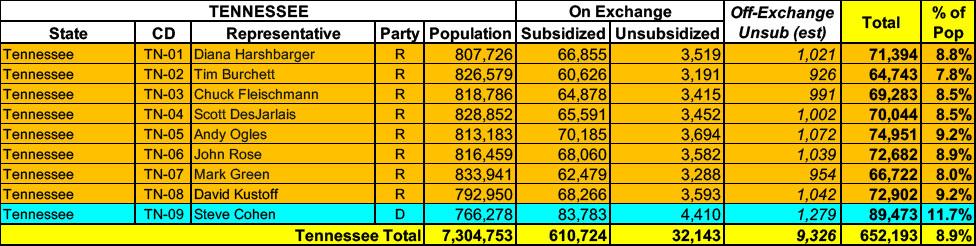

Tennessee has around ~642,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~9,000 unsubsidized off-exchange enrollees.

Nebraska has around ~136,000 residents enrolled in ACA exchange plans, 95% of whom are currently subsidized. I estimate they also have another ~2,000 unsubsidized off-exchange enrollees.

Alaska has around ~28,000 residents enrolled in ACA exchange plans, 88% of whom are currently subsidized. They also have an unknown number of off-exchange enrollees in ACA-compliant individual market policies. Overall, including net attrition, I estimate their total enrollment both on & off exchange to be perhaps ~27,000 or so.

Kansas has around 200,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~6,000 unsubsidized off-exchange enrollees.

New Hampshire has around ~70,000 residents enrolled in ACA exchange plans, 71% of whom are currently subsidized. I estimate they also have another ~14,000 unsubsidized off-exchange enrollees.

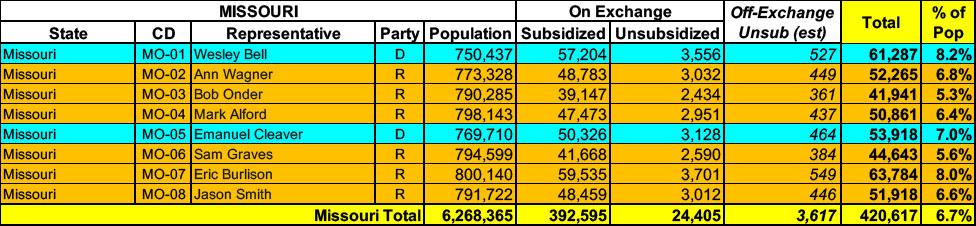

Missouri has around ~417,000 residents enrolled in ACA exchange plans, 94% of whom are currently subsidized. I estimate they also have another ~3,600 unsubsidized off-exchange enrollees.

Scope, Range, and Best Estimate of the Rate Increase

Blue Cross and Blue Shield of Oklahoma (BCBSOK) is filing new rates to be effective January 1, 2026, for its Individual ACA metallic coverage. As measured in the Unified Rate Review Template (URRT), the range of rate increases for these plans is 12.3% to 51.5%.

...Changes in allowable rating factors, such as age, geographical area, or tobacco use, may also impact the premium amount for the coverage.

There are currently 128,181 members on Individual Affordable Care Act (ACA) plans that may be affected by these proposed rates.

(Unfortunately, Anthem has redacted their current enrollment total; see below)

This is a rate filing for the Individual market ACA-compliant plans offered by Anthem Health Plans of New Hampshire, Inc., also referred to as Anthem. The policy forms associated with these plans are listed below. The proposed rates in this filing are for a new HMO product that will be effective for the 2026 plan year beginning January 1, 2026, and apply exclusively to off-exchange plans.

Blue Cross and Blue Shield of Nebraska (BCBSNE) is setting new rates for its Individual ACA market business in Nebraska. The rate change will take effect January 1, 2026, and will impact an estimated 22,300 members. On average, rates will go up by 20.5% compared to 2025 individual rates. Depending on the network and plan, rate changes will range from a decrease of 1.1% to an increase of 33.3%. Additionally, premiums will go up a bit each year as people get older, even if their plan rates stay the same.

BCBSNE used its own claims and enrollment data, and other publicly available information to set these rates.