It may not make any difference but believe it or not sometimes it does, even under the Trump regime...and in fact in some cases they're actively stating that they're seeking comment as opposed to just ramming the proposed changes through.

The Patient Protection & Affordable Care Act includes a long list of codified instructions about what's required under the law. However, like any major piece of legislation, many of the specific details are left up to the agency responsible for implementing the law.

It may not make any difference but believe it or not sometimes it does, even under the Trump regime...and in fact in some cases they're actively stating that they're seeking comment as opposed to just ramming the proposed changes through.

The Patient Protection & Affordable Care Act includes a long list of codified instructions about what's required under the law. However, like any major piece of legislation, many of the specific details are left up to the agency responsible for implementing the law.

UPDATE: Someone correctly pointed out that it’s a bit unfair to tell people to “be afraid” without giving them any action items to try and stave off the uglier changes being proposed. You have until March 13th to submit a comment to CMS. It may not make any difference but believe it or not sometimes it does, even under the Trump regime.

The Patient Protection & Affordable Care Act includes a long list of codified instructions about what's required under the law. However, like any major piece of legislation, many of the specific details are left up to the agency responsible for implementing the law.

Marketplace 2026 Open Enrollment Period (OEP) Report: National Snapshot

The Centers for Medicare & Medicaid Services (CMS) reports that 23.0 million consumers have signed up for 2026 individual market health insurance coverage through the Marketplaces since the start of the 2026 Marketplace Open Enrollment Period (OEP) on November 1, 2025.

This includes 15.8 million Marketplace plan selections in the 30 states using the HealthCare.gov platform for the 2026 plan year and 7.2 million plan selections in the 20 states and the District of Columbia with state-based Exchanges (SBEs) that are using their own eligibility and enrollment platforms.[1]

The Centers for Medicare & Medicaid Services (CMS) reports that 22.8 million consumers have signed up for 2026 individual market health insurance coverage through the Marketplaces since the start of the 2026 Marketplace Open Enrollment Period (OEP) on November 1, 2025. This includes 15.6 million Marketplace plan selections in the 30 states using the HealthCare.gov platform for the 2026 plan year and 7.2 million plan selections in the 20 states and the District of Columbia with state-based Exchanges (SBEs) that are using their own eligibility and enrollment platforms.

Total nationwide plan selections include 2.8 million consumers who are new to the Marketplaces for 2026, and 20.0 million consumers who had active 2025 coverage and selected a plan for 2026 coverage or were automatically re-enrolled.

Quick ACA Update: More than 15.6 million Americans have enrolled in a plan on the federally run exchanges so far — compared to roughly 16 million Americans last year.

Notably, this small drop follows several important CMS actions over the past year to combat fraudulent and improper enrollments, which have already removed more than enough people from premium subsidies who are covered elsewhere to account for the modest enrollment change. That said, there is a politically motivated lawsuit that has paused critical actions to make sure Biden-era improper enrollments are fully knocked out.

IMPORTANT NOTE: For those who need insurance and have not already signed up — go to HealthCare.Gov to see if you qualify and what types of plans you can get. Most Americans can access a plan for $21 a month!

The Centers for Medicare & Medicaid Services (CMS) reports that nearly 950,000 consumers who do not currently have health care coverage through plans in the individual market Marketplace have signed up for coverage in 2026, since the start of the Marketplace Open Enrollment Period (OEP) on November 1, 2025. Existing consumers are also returning to the Marketplace to actively renew their coverage, and anyone who does not actively renew will be automatically re-enrolled for 2026. Over 4.8 million existing consumers have already returned to the Marketplace to select a plan for 2026.

Definitions and details on the data in this report are included in the glossary.

As usual, I'll start out with the top line numbers, compared to the same point last year:

On Monday I noted that around 20 state-based ACA exchange websites had launched 2026 Open Enrollment "window shopping," which allows residents to plug in their household information (zip code, ages, income, etc) and browse the various health insurance policies they have to choose from for coverage starting January 1st...as well as whatever federal (and state, in some cases) tax credits they'll be eligible for.

The Affordable Care Act includes a long list of codified instructions about what's required under the law. However, like any major piece of legislation, many of the specific details are left up to the agency responsible for implementing the law.

While the PPACA is itself a lengthy document, it would have to be several times longer yet in order to cover every conceivable detail involved in operating the ACA exchanges, Medicaid expansion and so forth. The major provisions of the ACA fall under the Department of Health & Human Services (HHS), and within that, the Centers for Medicare & Medicaid (CMS)

Every year, CMS issues a long, wonky document called the Notice of Benefit & Payment Parameters (NBPP) for the Affordable Care Act. This is basically a list of proposed tweaks to some of the specifics of how the ACA is actually implemented for the following year.

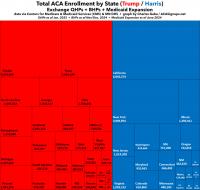

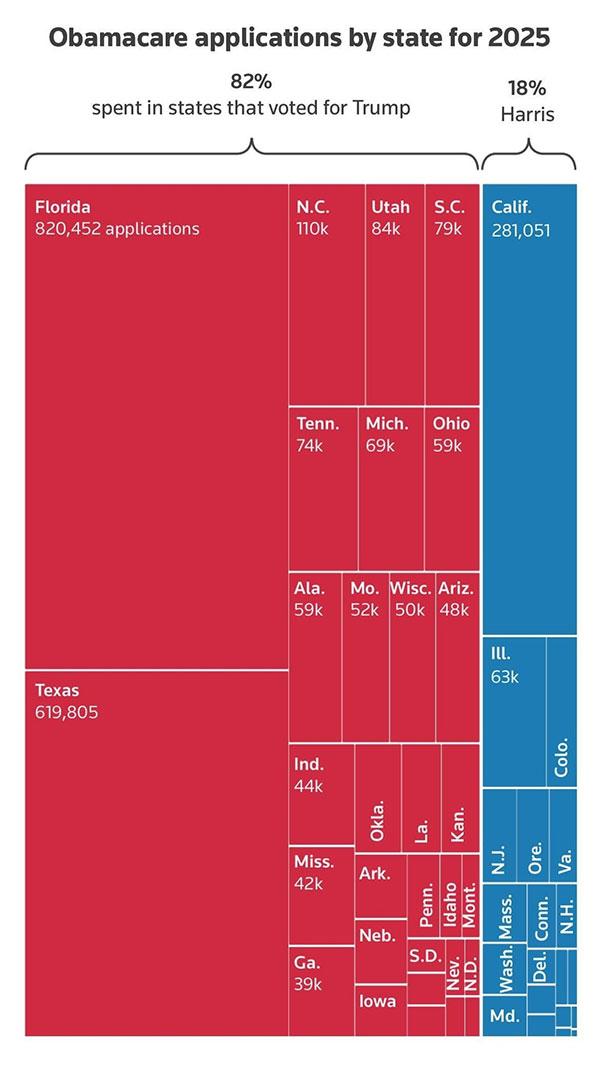

The graph purported to break out "Obamacare applications by state for 2025" by states which voted for Donald Trump vs. those which voted for Kamala Harris in November 2024. Here's what it looked like:

As I noted at the time, this graph was technically accurate...while simultaneously being jaw-droppingly misleading, for several reasons, including: