For nearly a year now I've been shouting from the rooftops about the eye-popping net premium hikes which millions of ACA enrollees are going to see starting one month from today, assuming the enhanced Advanced Premium Tax Credits (eAPTC) which have been in place for the past five years are allowed to expire on New Year's Eve.

I've put together 51 bar graphs showing examples of what these net premium increases will look like for various households at different income levels in every state. Since there's so many variables from state to state including different Rating Areas, different levels of carrier participation, different provider networks and different benchmark Silver plans from county to county (and even from zip code to zip code), I decided to use the capital city of each state as my rule of thumb.

For the households, I went with four case studies: A single 50-yr old adult w/no dependents; a 30-yr old single parent with one child; a "nuclear family" (40-yr old couple with two kids age 15 & 12); and a pre-retiree couple (64 yrs old, just shy of Medicare eligibility age).

IMPORTANT:Premium Alignment is NOT a substitute for making the enhanced ACA tax credits permanent. It does little to help the lowest-income folks who are still better off with Silver plans thanks to robust CSR assistance, and the benefits of it will be mediocre for those over 400% FPL if the enhanced tax credits expire.

Even for those it benefits the most (primarily those who earn between 200 - 400% FPL), it's a complement to the upgraded subsidies, not a replacement for them.

HOWEVER, it's still hugely helpful to those who know how to take advantage of it, and particularly in the states newly implementing it, it should relieve a huge portion of the pain being caused by the enhanced APTC expiring next month.

I've written multiple times in the past about "Silver Loading," the ACA health insurance policy pricing strategy in which insurance carriers load the extra cost of their Cost Sharing Reduction financial burden (the portion of deductibles, co-pays & coinsurance which they're required to cover themselves for low-income enrollees who select Silver plans) onto the gross premium of those same Silver plans.

It gets a bit wonky, but the bottom line is that Silver Loading results in the gross price of Silver ACA plans increasing significantly even if the price of Bronze, Gold & Platinum plans only go up modestly. This may sound bad, but stay with me.

From the carriers perspective, how the CSR load is allocated doesn't matter much as long as they aren't left stuck with the bill...but pricing the plans in this fashion has major implications for the enrollees themselves.

(sigh) OK, I'm not sure if we've reached the 5th or 6th chapter in this ongoing saga, but I hope it's the last one.

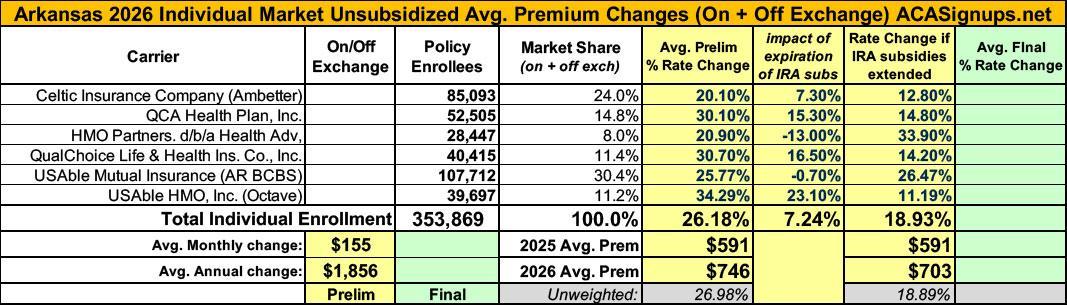

When we last left our story (just 5 days ago), I noted that both the current number of enrollees as well as the average rate increases for each of the carriers on the Arkansas individual market had jumped all over the place at least 4 times, and that while it's common for these numbers to change a bit here and there throughout the multi-month filing process, both the degree of some of the changes as well as the circumstances surrounding them were often far beyond what I've typically seen in over a decade of tracking this stuff:

Given all the confusing numbers I've posted before, I've boiled it all down to the simplified tables below which illustrate the mess:

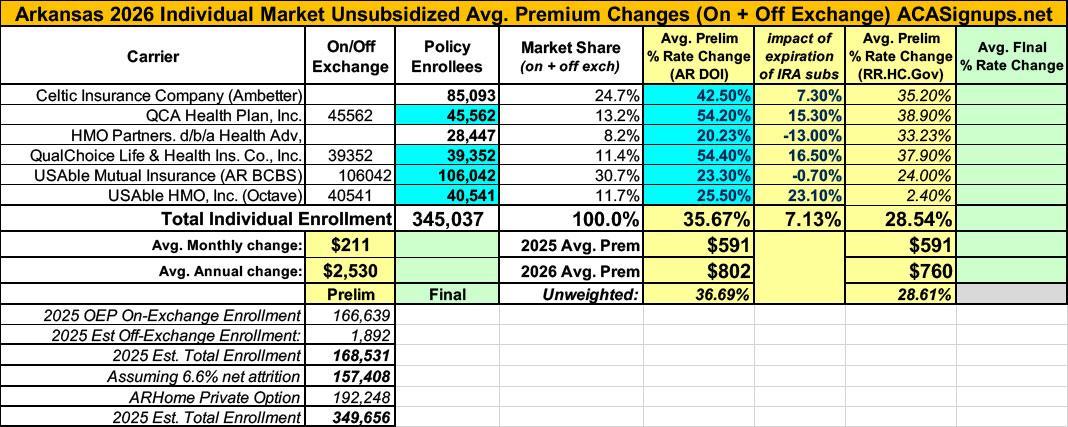

In the most recent chapter of the ongoing 2026 Arkansas rate filing saga, I noted that both the total number of residents enrolled in ACA individual market policies as well as the average 2026 rate increases for the six insurance carriers participating in the individual market next year kept changing, often in ways which were contradictory with other numbers claimed within the same press releases:

You'll notice that in addition to the rate changes being updated (increasing from a weighted average hike of 26.2% to 35.7%), most of the current enrollee figures were also modified, although these only changed slightly in most cases. Overall the total number of current individual market enrollees statewide dropped a bit from ~354,000 to ~345,000.

Minor changes like this aren't unusual; sometimes the carriers make slight tweaks as more recent data comes in or clerical errors are corrected; other times they round off the enrollee totals (that doesn't seem to be the case here, however).

Back in July I posted my analysis of the preliminary 2026 rate filings by the 6 Arkansas insurance carriers participating in the individual market. At the time, they looked like this:

I just finished writing up a deep dive into the Arkansas Insurance Dept's move from laissez faire-style Silver Loading to fully-regulated & maximized Premium Alignment in an attempt to mitigate the massive net premium damage about to be caused if the enhanced ACA premium tax credits expire at the end of 2025.

However, it's not just Arkansas which has finally seen the light and joined about a dozen other states in putting full-bore Premium Alignment (PA) pricing into place to help reduce the financial burden on ACA individual market enrollees in 2026.

Other states which have already done so in the past include Colorado (sort of), Texas, New Mexico, Maryland, Pennsylvania (somewhat), Illinois, Vermont and Wyoming.

Warning: This isn't just gonna get deeply wonky, it also requires digging deep into hisory. You've been warned.

Chapter 1: The (simplified) Backstory:

The ACA includes two types of financial subsidies: Advance Premium Tax Credits (APTC), which reduce monthly premiums; and Cost Sharing Reductions (CSR), which cut down on deductibles, co-pays & other out-of-pocket (OOP) expenses for low-income enrollees.

In 2014, then-Speaker of the House John Boehner filed a lawsuit on behalf of Congressional Republicans against the Obama Administration, in part because they claimed that CSR payments were unconstitutional because they weren't explicitly appropriated by Congress in the text of the Affordable Care Act.

A long legal process ensued, the end of which resulted in a federal judge ruling in the GOP's favor and ordering that CSR payments stop being made...but also staying that same order pending appeal of her decision by the Justice Department (then still run by the Obama Administration).

I've been following this bill for awhile now but never got around to writing about it until after it passed through both chambers of the Illinois legislature. That's a shame, because it's a pretty Big F*cking Deal for Illinois residents.

The Illinois House passed the Healthcare Protection Act Saturday to help curb predatory insurance practices and protect consumers.

Gov. JB Pritzker's monumental plan could make Illinois the first state to ban prior authorization for in-patient adult and children's mental healthcare. The legislation also bans step therapy, or the fail first method, where insurers force people to receive less effective treatment before moving to options initially recommended by doctors.

...The measure requires prior approval from the Department of Insurance before large group insurance plans can increase rates and states premiums must align with the actual cost of providing care as well.

Today I want to address the question of Actuarial Value (AV)...that is, what percent of medical expenses (in aggregate) a given healthcare policy actually pays for. As a quick reminder, ACA policies are generally broken into four AV categories, labeled by metal levels: Bronze, Silver, Gold and Platinum, which generally cover roughly 60%, 70%, 80% or 90% of enrollees in-network medical expenses per year (there's a fifth category in front of Bronze called Catastrophic plans, but these have limited eligibility and hardly anyone enrolls in them anyway).