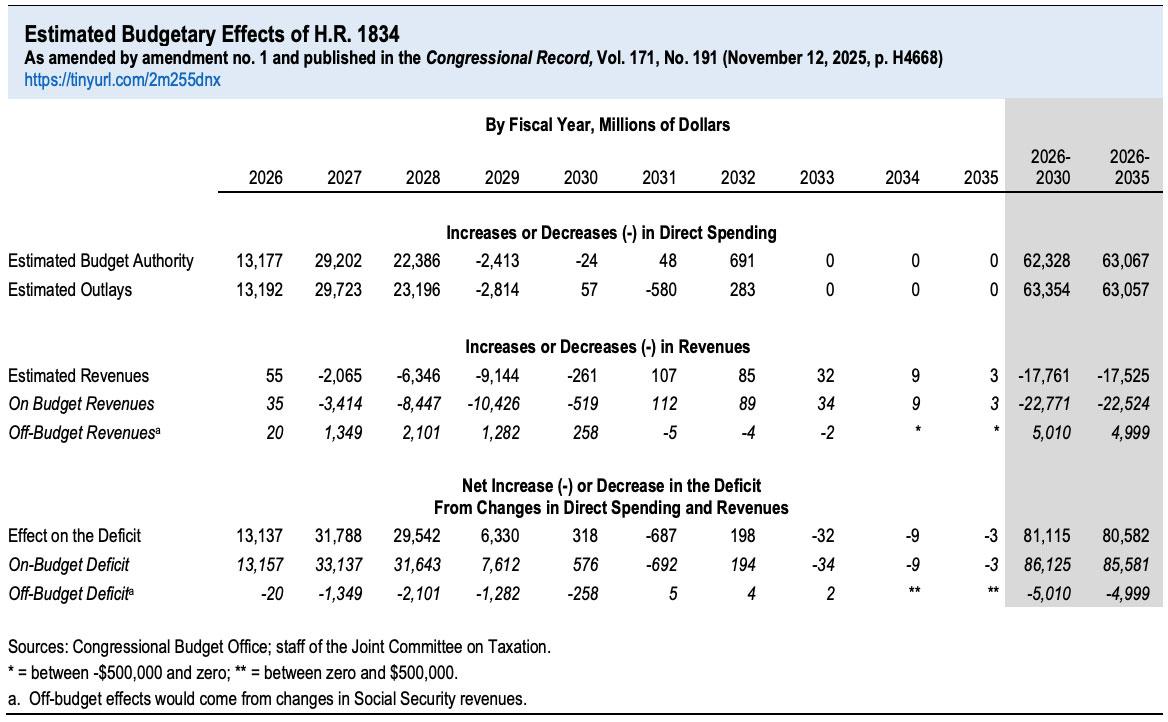

H.R. 1834 would authorize an extension through 2028 of the premium tax credit structure provided in the American Rescue Plan Act of 2021 and later extended through calendar year 2025 by the 2022 reconciliation act. The advanceable and refundable premium tax credit reduces out−of-pocket costs for the premiums enrollees pay for health insurance obtained through the marketplaces established by the Affordable Care Act.

Budget-wise, the CBO is pegging a 3-yr extension at costing around $80.6 billion net (they had previously pegged a 10-yr extension at ~$350B, but that assumes 10 years of inflation/etc as well).

If this happens, it would mean the ACA exchange market would drop by more than 1/3 from the ~24.2 million currently enrolled (myself & my own family included).

However, I've repeatedly stated that even this is likely a low estimate--the remaining ~16 million exchange enrollees would still be hit with MASSIVE (and in some cases eye-poppingly huge) premium hikes which would force them to drop to far worse plans (meaning much higher deductibles & co-pays; worse provider networks and so on).

Re: The Effects of Not Extending the Expanded Premium Tax Credits for the Number of Uninsured People and the Growth in Premiums

Dear Chairman Wyden, Ranking Member Neal, Senator Shaheen, and Congresswoman Underwood:

You have asked the Congressional Budget Office to discuss the effects on health insurance coverage and premiums that will result from not extending—either for one year or permanently—the expanded premium tax credit structure provided in the American Rescue Plan Act of 2021 (ARPA, Public Law 117-2).

ARPA reduced the maximum amount eligible enrollees must contribute toward premiums for health insurance purchased through the marketplaces established by the Affordable Care Act, and it extended eligibility to people whose income is above 400 percent of the federal poverty level (FPL). Those provisions were extended through calendar year 2025 in the 2022 reconciliation act (P.L. 117-169).

For ten years now, I've had Google Alerts set up to send me links to stories about the Affordable Care Act using various commonly-used phrases like "health exchanges" and such. Normally these bring up the most recent articles about the law, but last night one of them included a surprising link to a Reuters article from...March 2013:

Washington could wind up running more health exchanges - official

March 14, 2013

...The Obama administration has given 17 of the 50 states conditional approval to set up online exchanges where working families would purchase private plans at subsidized rates. The remaining 33 states will all have federally run markets, at least in the early years of the coming reform era.

But Gary Cohen, who spearheads exchange implementation for the U.S. Department of Health and Human Services, said some of the approved states face hurdles that could require Washington to step in with federal exchanges before open enrollment starts on Oct. 1.

Since the collapse of the Build Back Better Act in the U.S. Senate last December (reminder: It passed the House but came to a screeching halt when all 50 Republican Senators along with conservative Democrat Joe Manchin refused to support it), Congressional Democrats have been quietly trying to put at least some of the pieces of the bill back together in an attempt to salvage something out of President Biden's signature social spending agenda.

Personally, I'm most focused on making the enhanced/expanded ACA subsidies under the American Rescue Plan (ARP) permanent, of course, which the Congressional Budget Office estimated would cost roughly $220 billion over 10 years to implement. If the ARP subsidies are allowed to expire (which would revert the ACA back to the original subsidy formula, including bringing back the hated "Subsidy Cliff"), over 13 million Americans would find their health insurance premiums jump by an average of over $700/year apiece, with some households seeing theirs skyrocket by as much as $17,000/year (that's not a typo).

Regular readers may have noticed that I haven't checked in on the status of #BidenCare (aka #ACA 2.0) since way back in early August. There's several reasons for this: At first I was swamped with my COVID vaccination/case/death rate project; then, more recently, I had to scramble to get my annual Rate Change project up to date.

Both of these have indeed monopolized my time, but the main reason is simply that President Biden's Build Back Better (BBB) plan (which ACA 2.0 is a part of) has gotten bogged down over the past few months due to infighting and intransigence by a handful of "moderate/centrist" Democrats in the House but especially by two Democratic Senators in particular (Joe Manchin of West Virginia and Kyrsten Sinema of Arizona).

(Needless to say, I'm not even mentioning any Republicans in either the House or Senate, since not a single one of them is willing to support the bill.)

It seemed a bit pointless to write up a lengthy, in-depth analysis of the latest developments on the bill when what does or doesn't have a serious shot at making the final cut kept changing every few days.

A couple of weeks ago I went on a bit of a rant about some terribly irresponsible reporting about how much the American Rescue Plan is spending on subsidizing private health insurance and how many people that money is expected to provide insurance premium assistance for.

The bottom line is that a whole lot of people got both the numerator and denominator wrong: Instead of being ~$53 billion to cover ~1.3 million people (which would be an insane $40,000 per person for just six months), it's actually more like ~$61 billion to help cover ~18.6 million people (roughly $3,300 per person per year on average).

NOTE: SEE SUMMARY TABLE IN UPDATE ALL THE WAY AT THE END.

I'm doing my best to stop myself from putting my head through a wall this weekend.

You may have seen this viral tweet making the rounds over the past day or so:

The Democrats just spent $52 billion to subsidize COBRA for 1.3 million people until September. That’s $40k per person for less than 6 months of health insurance. Most countries spend about $5-6k per person per year for universal healthcare.

This was posted at 12:22pm on Friday, March 12th, 2021. It's still live as of 11:00am on Sunday the 14th, has over 32,700 Likes and has been retweeted over 7,300 times as of this writing, but in case it's deleted by the time you read this, here's a screen shot:

A few minutes ago the Congressional Budget Office released a new report on a national, universal single payer healthcare system (commonly known as "Medicare for All" these days, although that's a bit of a misnomer since the proposed "Medicare for All" bills are quite different from today's definition of Medicare).

It's important to note that while this report came from the CBO, it is not a budget analysis of either the House or Senate MFA bills; it instead lays out the structural components which would be required to be in place in order to put such a system together and, I presume, in order to run such a budget analysis.

I'm swamped today between the rollouts of both the Choose Medicare Act and the revised Medicare for America Act as well as this new CBO report, so for the moment I'll just repost the summary and link to the report itself, along with a few notes as I'm able to add them:

I'm a little late to the party on this one, but a week or so ago, the Congressional Budget Office released their own report breaking out estimates of just how many Americans have different types of major helathcare coverage (public or private) for each of the past four years (2015 - 2018).

Their conclusions show a far less dramatic change compared to the survey released by Gallup back in January, which claimed that the uninsured rate for adults over 18 increased from 10.9% at the end of 2016 (just as President Obama left office) to 13.7% at the end of 2018. Based on their estimates, that amounts to around 6.8 million adults losing coverage over that time...and that doesn't include children, so the Gallup estimates, if accurate, would top 7 million people losing coverage.