About 200,000 Virginians will be eligible to tap into new state funding meant to offset costs for insurance through the state’s Affordable Care Act exchange, starting in November.

This means that participants could save about 70% on their monthly premium, after state lawmakers and Gov. Abigail Spanberger approved $150 million dollars for it in the state budget late last month.

The move comes after federal funding shifts triggered by Congress’ failure to renew expiring ACA subsidies. Thousands of Virginians have dropped their coverage so far this year as premiums have shot up.

Virginia’s Health Benefit Exchange estimates that about 100,000 Virginians have lost their health coverage this year as a result of higher premiums, according to a new press release.

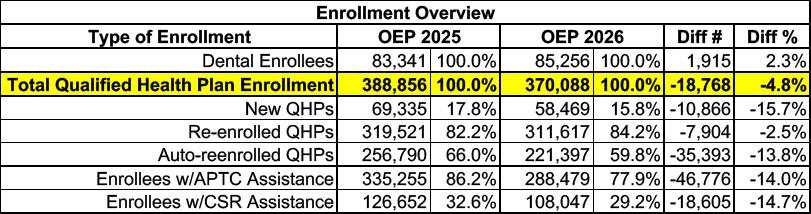

Here's the overview of Virginia ACA exchange enrollment over the course of OEP 2026 vs. 2025. Stand-alone dental plan enrollment is up 2.3%, which is nice, but overall major medical plan (Qualified Health Plan, or QHP) enrollment dropped by nearly 19,000 people, or 4.8% year over year.

There's also 14% fewer enrollees receiving federal tax credits than last year (nearly 47,000 people), while another 15% lost Cost Sharing Reduction assistance (CSR).

16 Million Americans Would Become Uninsured Due to Reconciliation Bill and Loss of Tax Credits; 8.2 Million in Marketplaces Alone

Leaders from State-based Health Insurance Marketplaces, Enrollees, Providers, and Small Business Highlight Potential, Devastating Impacts

(Washington, DC) The Congressional Reconciliation bill and loss of federal tax credits would result in 16 million Americans losing health coverage, including 8.2 million enrolled in Health Insurance Marketplaces. By stripping millions of lives from the Marketplaces, health care will be more expensive, harder to access, create a strain on health care systems, and hurt small businesses.

Virginia’s Insurance Marketplace is proud to announce that more than 388,000 Virginians successfully enrolled in health care coverage during the Marketplace’s Open Enrollment Period, which ran from November 1, 2024, to January 22, 2025.

Among the 388,856 Virginians who secured health insurance plans through Virginia’s Insurance Marketplace, 69,000 were new enrollees. This is a 21% increase in new enrollments from last year’s Open Enrollment Period, marking a significant milestone for the Marketplace.

New enrollments may be up 21%, but overall enrollments are down 2.8% vs. last year, which is a bit of a head-scratcher since there doesn't seem to be any specific reason for enrollment to drop in VA this year (as opposed to NY, OR & NC which each had cannibalization of exchange enrollees by their Medicaid or Basic Health Plan programs this year).

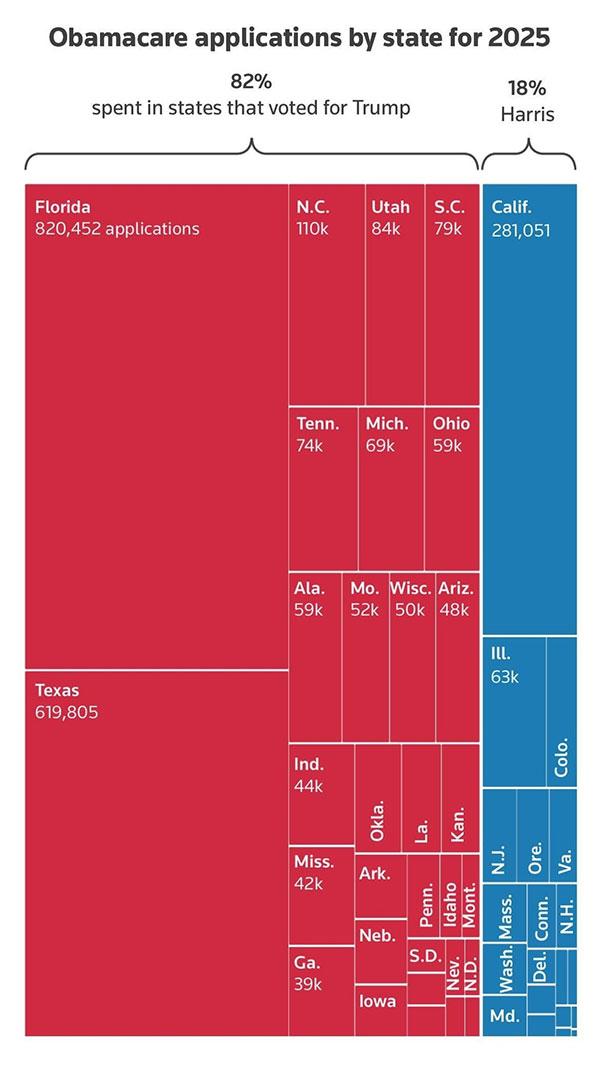

The graph purported to break out "Obamacare applications by state for 2025" by states which voted for Donald Trump vs. those which voted for Kamala Harris in November 2024. Here's what it looked like:

As I noted at the time, this graph was technically accurate...while simultaneously being jaw-droppingly misleading, for several reasons, including:

This morning, the Twitter account NewsWire_US, which claims to be a "U.S. and world news aggregator," posted an amazing-looking graph which purports to break out "Obamacare applications by state for 2025" by states which voted for Donald Trump vs. those which voted for Kamala Harris last month.

Here's the graph, which includes no further context (including any data sources...NewsWire claims it came from Reuters but I can't find the original link to a story by them with this graph) beyond making it look like a whopping 82% of ACA enrollees live in Trump states:

Update: Here's the original Reuters article, which was actually published on Dec. 11th, which at least explains why it only includes data through Nov. 16th/9th, anyway.

The Centers for Medicare & Medicaid Services (CMS) has published two 2025 ACA Open Enrollment Period "snapshot reports," both of which had above-the-fold numbers which make it look as though enrollment numbers are lagging significantly behind last year's record-breaking totals:

The Centers for Medicare & Medicaid Services (CMS) is committed to creating a robust Marketplace Open Enrollment process for consumers so they can effortlessly purchase high-quality, affordable health care coverage. CMS reports that nearly 988,000 consumers who do not currently have health care coverage through the individual market Marketplace have signed up for plan year 2025 coverage.

The Centers for Medicare & Medicaid Services (CMS) is committed to creating a robust Marketplace Open Enrollment process for consumers so they can effortlessly purchase high-quality, affordable health care coverage. CMS reports that nearly 988,000 consumers who do not currently have health care coverage through the individual market Marketplace have signed up for plan year 2025 coverage.

Over 496,000 New Consumers Selected Affordable Health Coverage in ACA Marketplace

The Centers for Medicare & Medicaid Services (CMS) is committed to creating a robust Marketplace Open Enrollment process for consumers so they can effortlessly purchase high-quality, affordable health care coverage. CMS reports that 496,000 consumers who do not currently have health care coverage through the individual-market Marketplace have signed up for plan year 2025 coverage.

Pennie Has Issued a New Request for Proposal (RFP) for an Enrollment Assister Contract to Expand Support Across Pennsylvania Communities

Pennie is seeking an organization to build grassroots awareness and provide direct enrollment assistance to Pennsylvanians seeking health coverage. Proposals due at 1 pm on June 27th.

Harrisburg, PA – May 2024 – Pennie, PA’s official health insurance marketplace, has issued a Request for Proposal for Assister Services. The awardee will collaboratively drive statewide activities to increase awareness of the financial help and health coverage available through Pennie, and work directly with community organizations to provide local, in-person enrollment assistance.