Yesterday I noted that the Centers for Medicare & Medicaid Services (CMS) has published a new database which updates the official effectuated ACA exchange enrollment data for all 50 states (+DC) through February 2026.

This means that I finally have comprehensive effectuated enrollment data for the first two months of the year for every state, as opposed to only having Open Enrollment Period (OEP) plan selections, which aren't the same thing.

While there are still four months of effectuated enrollment data missing, this still fills in a lot of the missing pieces of the year over year enrollment puzzle, since this new database also includes state-level effectuations from August - December 2025 as well (previously I only had the national total for those months).

But actually, he thought as he re-adjusted the Ministry of Plenty’s figures, it was not even forgery. It was merely the substitution of one piece of nonsense for another. Most of the material that you were dealing with had no connexion with anything in the real world, not even the kind of connexion that is contained in a direct lie. Statistics were just as much a fantasy in their original version as in their rectified version. A great deal of the time you were expected to make them up out of your head.

For example, the Ministry of Plenty’s forecast had estimated the output of boots for the quarter at 145 million pairs. The actual output was given as sixty-two millions. Winston, however, in rewriting the forecast, marked the figure down to fifty-seven millions, so as to allow for the usual claim that the quota had been overfulfilled. In any case, sixty-two millions was no nearer the truth than fifty-seven millions, or than 145 millions.

Yesterday morning on CNN's "State of the Union," host Kasie Hunt talked to Oklahoma GOP Sen. James Lankford about the enhanced ACA tax credits which are currently scheduled to expire exactly 10 days from now.

This gets into the weeds a bit, so I'm breaking it into two separate posts; I'll be publishing the second part tomorrow.

The crux of the CNN appearance was Langford claiming that "Obamacare" (the Affordable Care Act...guys, he's been out of office for nearly 9 years now, let it go willya?) "caused prices to skyrocket in the marketplace" and that the expiration of the enhanced tax credits put into place in 2021 during the COVID pandemic is simply "exposing the real issues" within the ACA.

First of all, let's clear up this "they were only put in place due to the COVID pandemic" talking point which Republicans keep tossing around (the implication being that since the COVID pandemic is over, the subsidy upgrade should end as well).

Get it straight: Eliminating the 400% FPL subsidy cliff and beefing up the tax credit formula is something which Democrats always intended to do when they had the ability to do so.

Company’s HR Manager Really Pushing Infinite-Deductible Health Care Plan

During a meeting with new hires Wednesday to discuss employee benefits, Radian Analytics human resources manager Ellen Schultz is said to have strongly pushed the company’s infinite-deductible health care option.

According to sources in attendance, Schultz described the low-premium, infinite-deductible plan as the simplest and most convenient choice available to employees, and said it works the same whether plan members need to visit their primary care physician, fill a prescription, or be admitted to a hospital, allowing them in each case to pay 100 percent of the incurred medical expenses.

With the ongoing budget battle approaching the Sept. 30th federal government shut down deadline, U.S. Senator Patty Murray (D-WA) and U.S. Representative Rosa DeLauro (D-CT-03) have formally introduced a bicameral Continuing Resolution bill to fund the government for an extra month to buy more time to negotiate and avoid a shutdown by the Republican-controlled federal government:

Today, Senator Patty Murray (D-WA), Senate Appropriations Committee Vice Chair, and Congresswoman Rosa DeLauro (D-CT-03), House Appropriations Committee Ranking Member, introduced a continuing resolution (CR) to keep the government funded and allow negotiations to continue over full-year bills that ensure Congress, not President Trump or Russ Vought, decide how taxpayer dollars are spent. The CR also addresses the health care crisis Republicans have single-handedly created and protects Congress’ power of the purse, rejecting President Trump’s illegal “pocket rescission.”

Our survey of voters in the most competitive Congressional Districts shows Republicans have an opportunity to overcome a current generic ballot deficit and take the lead by extending the healthcare premium tax credits for those who purchase health insurance for themselves. Without Congressional action, the tax credit expires this year.

Ever since the MAGA Murder Bill (officially H.R. 1, the so-called "One Big Beautiful Bill Act") was passed by Republicans in the U.S. Senate & House and signed into law by Donald Trump a few days ago, I've seen a growing conventional wisdom taking hold on social media: People keep claiming that either all, "nearly all" or at least "most of" the budget cuts & other gutting of various programs and departments won't actually kick in until after the November 2026 midterms.

Now, don't get me wrong--most of those making these claims are well-intentioned; they're saying this cynically, to underscore how disingenuous Congressional Republicans are by back-loading the pain until the midterms are safely in their rearview mirrors. And, to be fair, much of the damage won't being until well after next November.

Over at The New Republic, Greg Sargent has taken this thinking one step further, noting that by delaying so much of the ugliness of the new law until 2027 or beyond...

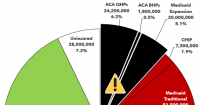

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

Political battles are usually won based on appealing to emotion, not to facts, policy or logic.

However, you should still have those facts at your disposal for two reasons: First, they still help you craft appeals to emotion. Second, they also help you craft the actual policy. Besides, I'm a data guy; my primary job is to help put facts & policy into easily-understandable context.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.