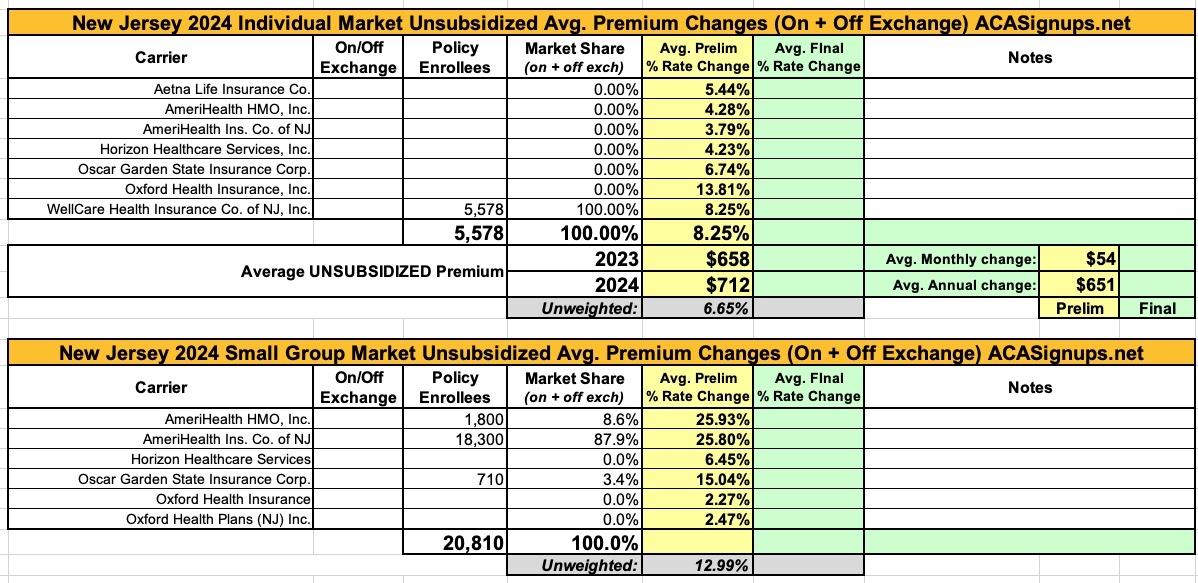

New Jersey: Preliminary avg. unsubsidized 2024 #ACA rate changes: +6.7% (unweighted)

Mon, 08/14/2023 - 12:15pm

New Jersey individual & small group market carriers are asking for unweighted average rate increases of 6.7% and 13.0% respectively for 2024. However, the unweighted averages don't tell the whole story--the carriers are asking for rate hikes ranging from as low as 3.8% to as high as 13.8% on the individual market, and from as low as 2.3% to a stunning 25.9% for small group plans.

As is the case with far too many states these days, most of the rate filing memorandums are heavily redacted in New Jersey, making it nearly impossible to get ahold of the actual enrollment numbers, which means I have no way of running a weighted average on either market.

I should note that there's one thing about the federal Rate Review website which I've never understood. This applies to many other rate filings in other states as well, but I'm using WellCare as an example since it's the only carrier which has an unredacted filing memo this year.

The Rate Review database at HealthCare.Gov clearly states that the average requested rate change for 2024 for WellCare is 8.25%, ranging from an 8.01% reduction to an 8.77% increase:

HOWEVER, according to the actual WellCare individual market filing, it's actually more than double that: 16.7%:

WellCare Health Insurance Company of New Jersey, Inc. (WellCare of NJ) is filing rates for the individual block of business, effective January 1, 2024. This document is submitted in conjunction with the Part I Unified Rate Review Template and the Part III Actuarial Memorandum.

This information is intended for use by the New Jersey Department of Banking and Insurance, the Center for Consumer Information and Insurance Oversight (CCIIO), and health insurance consumers in New Jersey to assist in the review of WellCare of NJ’s individual rate filing.

The results are actuarial projections. Actual experience will differ for a number of reasons, including population changes, claims experience, and random deviations from assumptions.

In 2022, earned premium was $566.71 per member per month (PMPM). Incurred claims in 2022 were $149.65, or 26.4% of premium. The historical administrative expenses for 2022 were $37.23 PMPM, which excludes taxes and fees. Netting risk adjustment from the claims results in an estimated loss ratio (incurred claims net of estimated risk adjustment transfers, divided by earned premiums) of 77.5%. Earned premium was $527.97 PMPM net of minimum loss ratio rebates.

We expect unit costs to increase for 2024. Further, we have updated underlying experience for the single risk pool, expected administrative expense, assumptions for federal risk adjustment, and impacts of the COVID-19 pandemic. These factors, as well as changes to the assumed morbidity of the single risk pool and medical trend, each contribute to the premium rate change.

Medical trend, or the increase in health care costs over time, is composed of two components: the increase in the unit cost of services and the increase in the utilization of those services. Unit cost increases occur as care providers and their suppliers raise their prices. Utilization increases can occur as people seek more services than before. Additionally, simple services can be replaced with more complex services over time, which is known as service intensity trend. An example of service intensity trend would be the replacement of an X-ray with an MRI scan. Replacing the service with a more intense service causes the total cost of medical services to increase.

The proposed rate change of 16.7% applies to approximately 5,578 individuals. Cost trend contributes +5.8% towards the 2024 rate change, while trended experience and updated expectations for single risk pool utilization contribute +9.6%.

The proposed rate changes by plan are as follows:

- Gold 1008: -0.8%

- Silver 1003: +15.4%

- Silver 1007: +17.2%

- Silver 1007 Off Exchange: +16.3%

I've never known what to make of this. I try to use the actual rate filings whenever possible and only rely on the federal database when I have to, but this is such a dramatic difference I have no idea which one to use, nor what it says about using the other RR.HC.gov listings.

Advertisement