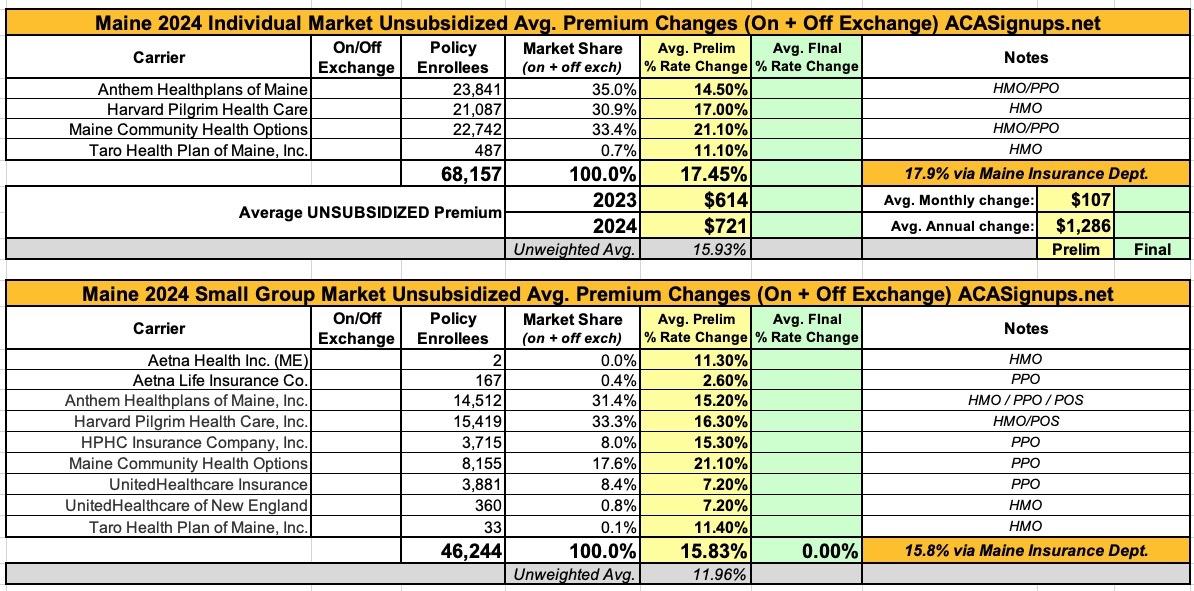

Maine: Preliminary avg. unsubsidized 2024 #ACA rate changes: +17.9%

Thu, 06/22/2023 - 4:19pm

Each year insurers that sell Individual and Small Group plans in Maine's pooled risk market must submit their proposed forms and rates to the Bureau of Insurance, using the System for Electronic Rate and Form Filing (SERFF). Details of the filings submitted to the state since June 10, 2010 can be viewed in the system.

To see details of a filing, click on the Search Public Filings button below and paste or type in the relevant SERFF Tracking Number listed in the table (no need to complete the rest of the form).

Anthem Health Plans of Maine:

Drivers of Rate Increase

The primary drivers of premium increases are associated with increased cost of benefit expense for this ACA compliant block and the changes in the regulatory requirements. Increased cost of benefit expense is driven by increases in the price of services primarily from hospitals, physicians and pharmacies, coupled with members increasing their use of health care services, also called “utilization”. Increases in the price of services are driven by technological advances, new specialty medications, and a variety of other factors. Increased utilization is driven by member level utilization and selection patterns in the Guaranteed Issue, Community Rated ACA market. The changes in the regulatory requirements includes the reduction of the coverage from the Maine Guaranteed Access Reinsurance Association (MGARA) program as result of the merging of the Individual and Small Group ACA markets in Maine, and the new mandated benefits.

Rates are in accordance with the regulatory framework and insurer participation in the market as of June 16, 2023. To the extent emerging data, changes to practice patterns, or requirements show that COVID-19 vaccinations, testing, and treatment are impacting costs significantly different than assumed or if there are changes in regulation or insurer participation, then these rates may no longer be appropriate and will be evaluated for resubmission.

Harvard Pilgrim Health Care:

Harvard Pilgrim is filing updated plans for 2024 to comply with the 2024 Clear Choice Designs published by the Bureau of Insurance in accordance with Rule 851. The existing 2023 enrollees have been mapped to the most similar 2024 plan in considering the rate increases for 2024. With these changes the increases by plan will vary, with some plans receiving higher increases and some receiving lower increases than the average. The average increase for renewing members is 17.0%.

The primary drivers of the rate increase include:

- Medical cost trend reflecting anticipated increases in both unit cost and use of services for

- inpatient, and outpatient settings

- Difference in actual to projected experience

- Impact of new mandated benefits

- Changes in benefit design and product mix

- Change in the MGARA reinsurance program

- Anticipated changes in risk adjustment

- Changes in administrative expenses

The rates for silver plans offered on the Exchange include a load of 12% to cover the cost of CSR which is no longer being funded by the Federal Government.

Maine Community Health Options:

The rate changes are driven by the following key changes in rating from 2023 to 2024:

- Effective January 1, 2024, the MGARA parameters will increase and expected recoveries under that program are expected to be significantly reduced.

- Medical cost trend assumed to equal 7.1%

Financial Experience

CHO’s financial experience for the most recent three years is presented below. These results reflect the impact of MGARA and risk adjustment.

CY 2020

- Collected Premium: $123,736,132

- Earned Premium: $123,736,132

- Incurred Claims: $68,507,499

- Incurred Loss Ratio: 55.4%

CY 2021

- Collected Premium: $83,901,797

- Earned Premium: $83,901,797

- Incurred Claims: $69,612,109

- Incurred Loss Ratio: 83.0%

CY 2022

- Collected Premium: $122,862,473

- Earned Premium: $122,862,473

- Incurred Claims: $105,418,467

- Incurred Loss Ratio: 85.5%

Benefit Changes

Benefits change effective January 1, 2024 to comply with the Clear Choice plan designs required under Rule 851. The impact of these changes is not a significant driver of the requested rate increases.A new fertility benefit will be included in all plans effective January 1, 2024 as described by Rule 865.

Administrative Costs and Anticipated Profits

CHO allocates all of its expenses to plans using a constant percent of premium.Total retention included in the 2024 rates is equal to 15.76% of premium. This is comprised of 13.78% for general administrative expenses, 1.5% profit and risk load, and 0.49% for taxes and fees. Retention included in the 2023 rates was equal to 19.29% of premium. Note that the 2023 retention included the $4 MGARA fee but it is excluded from retention in the 2024 pricing.

Taro Health:

Reason for rate increase

The rates for these products are being adjusted for the reasons outlined in this section.

BENEFIT DESIGN CHANGES

Benefit design changes were made to a number of cost-sharing parameters, including updating maximum out-of-pockets and deductibles according to Clear Choice limits. See the accompanying AV calculator screenshots for more detail on plan benefits.MANUAL RATE CHANGES

We have updated our approach to develop the manual rate using the latest available information on risk adjustment and publicly available data submitted in connection with Maine individual and small group rate filings for the 2022 and prior plan years. This also includes an update to the underlying direct primary care contracted fees and assumed member effectuation, based on experience and known changes to-date. The manual rate development section contains additional information.MEDICAL TREND

The claim cost assumptions have been adjusted to reflect expected increases in unit cost and utilization. The manual rate development section contains additional information.

Advertisement