I've already noted that 17 states have launched window shopping for the 2026 ACA Open Enrollment Period (OEP), allowing residents of the following states to plug their household information into their states ACA exchange website to see just how much their net health insurance premiums are going to increase starting January 1st, 2026:

Every year, even when the ACA is running smoothly, there are always changes in market participation, as different insurance carriers enter or exit the individual market in certain states or either expand or shrink what parts of the state they offer healthcare policies in.

2026 is no exception, and given the massive turmoil the ACA exchanges are undergoing right now (due primarily to the expiring federal tax credits as well as regulatory changes made by the Trump Regime's so-called "Integrity & Affordability Rule"), there's either 13 or 32 insurance carriers throwing in the towel in one or more states, depending on how you count a carrier operating in multiple states or under multiple subsidiary brandings.

It's important to keep in mind that the following list probably isn't comprehensive--it includes the carriers which I've confirmed are pulling out statewide (with one exception: Meridian Health Plan of Michigan is only pulling out of parts of the state). There's likely one or two that I've missed, especially given that several of these have only made their final decisions within the past week or so.

OK, this is a bit embarrassing, but I just realized that the last time I wrote anything significant about about Illinois joining 20 other states in moving off of the federally-facilitated ACA marketplace (HealthCare.Gov) onto their own fully state-based platform (Get Covered Illinois) was nearly 2 1/2 years ago, when the state legislature passed the bill and Gov. Pritzker signed it into law!

For obvious reasons it feels a little weird to be writing about it at this particular moment in time, but the fact remains that yes, Illinois will be making the move starting November 1st, 2025. Here's a formal press release from August:

Get Covered Illinois Transitions to a State-Based Marketplace this November

The good news is, the Illinois Insurance Dept. now provides a handy, simple table with the actual average rate changes as well as direct links to the actuarial memos & other filing forms for every carrier, which made it easy for me to plug in the effectuated enrollment & calculate the weighted average rate hikes for every carrier in both the individual and small group markets.

The bad news is, some of the actuarial memos themselves are heavily redacted, meaning I'm unable to see how much of the rate hikes are due to the IRA subsidies expiring, CSR payments being reinstated or Trump's tariffs.

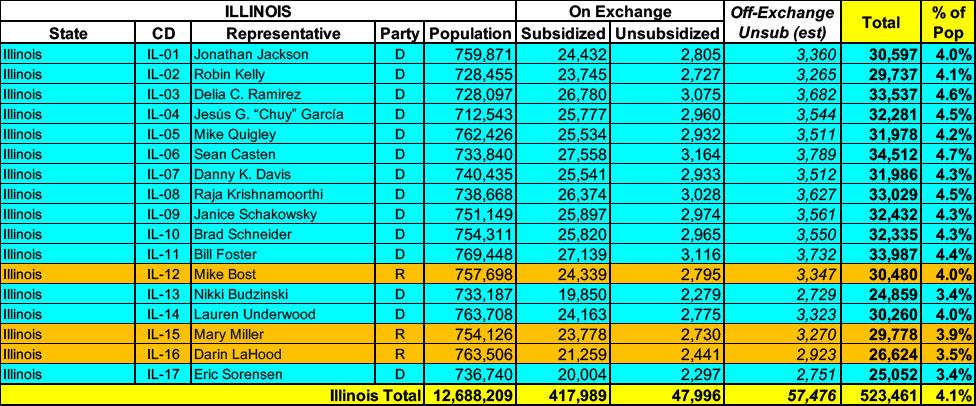

Illinois has around ~466,000 residents enrolled in ACA exchange plans, 90% of whom are currently subsidized. I estimate they also have another ~57,000 unsubsidized off-exchange enrollees.

With the pending dire threat to several of these programs (primarily Medicaid & the ACA) from the House Republican Budget Proposal which recently passed, I'm going a step further and am generating pie charts which visualize just how much of every Congressional District's total population is at risk of losing healthcare coverage.

USE THE DROP-DOWN MENU ABOVE TO FIND YOUR STATE & DISTRICT.

I've been following this bill for awhile now but never got around to writing about it until after it passed through both chambers of the Illinois legislature. That's a shame, because it's a pretty Big F*cking Deal for Illinois residents.

The Illinois House passed the Healthcare Protection Act Saturday to help curb predatory insurance practices and protect consumers.

Gov. JB Pritzker's monumental plan could make Illinois the first state to ban prior authorization for in-patient adult and children's mental healthcare. The legislation also bans step therapy, or the fail first method, where insurers force people to receive less effective treatment before moving to options initially recommended by doctors.

...The measure requires prior approval from the Department of Insurance before large group insurance plans can increase rates and states premiums must align with the actual cost of providing care as well.

Provides that beginning before or on May 1, 2026, and each May 1 thereafter, the Department of Insurance shall report to the Governor and the General Assembly on health insurance coverage, affordability, and cost trends.

Amends the Illinois Insurance Code.

Provides that any forms and rates filed for large employer group accident and health insurance shall be automatically deemed approved after 90 days after filing.

Provides that beginning plan year 2026, rate increases for all individual and small group accident and health insurance policies must be filed with the Department for approval.

Provides that unreasonable rate increases or inadequate rates shall be modified or disapproved.

Provides that beginning plan year 2025, the Department shall post all insurers' rate filings and summaries on the Department's website.

Back in February, I wrote about a bill introduced into the Illinois State Senate by Sen. Laura Fine (SD-09) which made my heart sing:

Amends the Department of Insurance Law.

Provides that the Department of Insurance shall establish the Office of the Healthcare Advocate.

Provides that the Office shall be administered by the Chief Health Care Advocate, who shall report to the Director of Insurance.

Amends the Illinois Insurance Code and the Health Maintenance Organization Act.

Provides that all individual and small group accident and health policies written subject to certain federal standards must file rates with the Department for approval.

Provides that unreasonable rate increases or inadequate rates shall be modified or disapproved.

Provides that when an insurer files a schedule or table of premium rates for individual or small group health benefit plans, the insurer shall post notice of the premium rate filings and a filing summary in plain language on the insurer's website.

Provides that the Department shall post all insurers' rate filings and summaries on the Department's website.

Provides that the Department shall open a 30-day public comment period on the date that a rate filing is posted on the website.