Illinois Senate voted unanimously to override the Governor's veto of a bill to limit short-term health plans to 6 months. Protecting consumers and insurance markets from long-term short-term plans does not appear to be a partisan issue. https://t.co/fJ4NVV4LRQ

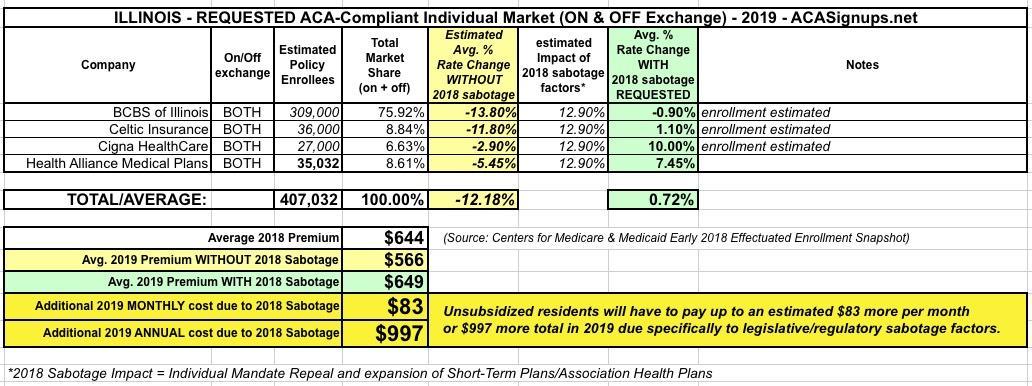

I ran the numbers for Illinois' requested 2019 ACA individual market rate changes back in August. At the time, the weighted year-over-year average was a mere 0.7% increase, with Cigna and Health Alliance's 10% and 7.5% being mostly cancelled out by Celtic's 1.1% and especially Blue Cross Blue Shield's slight drop of 0.9%. Since BCBSIL holds something like 3/4 of the state's individual market share, that alone mostly wiped out the other increases.

Unfortunately, I don't have access to the hard enrollment numbers, so this was a rough estimate based on 2017's breakout. Here's what it looked like at the time:

Ensure that young adults can continue to remain on their parents’ health insurance plans until age 26

Prohibit insurers from using applicants’ gender to set premiums

Prohibit insurers from rejecting an application based on an applicant’s medical history, or imposing coverage exclusions based on pre-existing conditions.

Today, however, there were major developments regarding #ShortAssPlan restrictions (and a few other important patient protection bills) in three states: Two positive, one negative.

Illinois has the same four ACA indy market carriers participating next year as they do this year. All four rate filings specificlaly call out Mandate Repeal and #ShortAssPlans as significant factors in their rate requests, but none of them break out the actual amount, so I'm relying on my standard assumption of 2/3 of the Urban Institute's projections.

In Illinois' case, that's 2/3 of 19.4%, or around a 12.9% #ACASabotage premium increase for unsubsidized enrollees.

I should also note that only one of the four carriers (Health Alliance) specifies just how many enrollees they have; for the other three I'm basing my estimates on last year's numbers for now. The two carriers with what I assume are still the largest market share (BCBS and Celtic) are basically keeping rates flat year over year, while the other two are 7.5% and 10% apiece, for an average rate increase of just 0.7% statewide.

Unsubsidized Illinois residents are currently paying $644/month on average, so a 12.9% sabotage effect means that each of them will have to pay nearly $1,000 extra next year. Ouch.

Over the past few weeks I've noted that a half-dozen states or so (Maryland, New Jersey, Vermont, Hawaii, California and Illinois) have been pushing through a long list of bills/laws at the state level to either protect the ACA from sabotage or even strengthen it. Meanwhile, other states have either expanded Medicaid under the ACA (Virginia, of course) or have locked in ballot measures to do so this fall (Utah, Idaho). Finally, several states have announced they're joining dozens of others to take advantage of "Silver Loading" or full-on "Silver Switching".

This evening brought three major pieces of ACA-related news out of three different states:

First, in California, the State Senate passed SB-910, which wouldn't just limit short-term plans, but would outright prohibit them altogether. To my knowledge, CA would be the only state* where STPs wouldn't be allowed at all:

(*Correction: It turns out that New York, New Jersey and Massachusetts also ban Short-Term Plans as well, although according to Dania Palanker of the Center on Health Insurance Reforms at Georgetown University, California would be the first state to explicitly outlaw short-term plans as opposed to simply stating that all policies have to meet certain standards.)

SACRAMENTO – Today, the State Senate approved passage of Senate Bill 910, which prohibits the sale of short term limited duration health insurance in California.

Even before President Donald Trump announced plans last week to nix Obamacare subsidies, the Illinois Department of Insurance raced over the summer to get insurers on board with a strategy to minimize the financial pain of such a move.

...Trump on Oct. 12 ordered the federal government to stop paying the cost-sharing subsidies provided to insurers to defray the cost of covering low-income people. But the Rauner administration has found a way to make the federal government pick up the tab anyway.

Up until a week ago, the possibility of Donald Trump pulling the plug on Cost Sharing Reduction reimbursement payments was a looming threat every day. While it hadn't actually happened yet, most of the state insurance commissioners and/or insurance carriers themselves saw the potential writing on the wall and priced their 2018 premiums accordingly (or at the very least prepared two different sets of rate filings to cover either contingency).

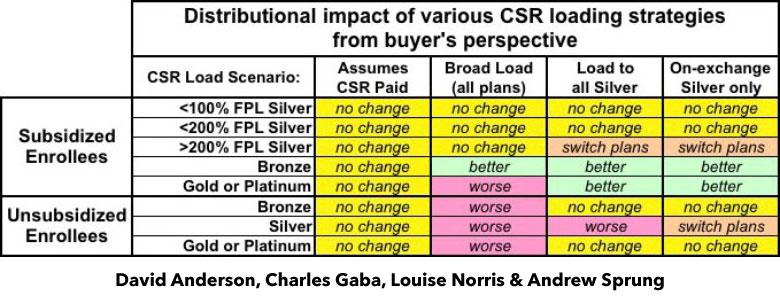

A few spread the extra CSR load across all policies, both on and off the exchange. This seems like the "fairest" way of handling things on the surface, but is actually the worst way to do so, because it hurts all unsubsidized enrollees no matter what they choose for 2018 and can even make things slightly worse for some subsidized enrollees in Gold or Platinum plans.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

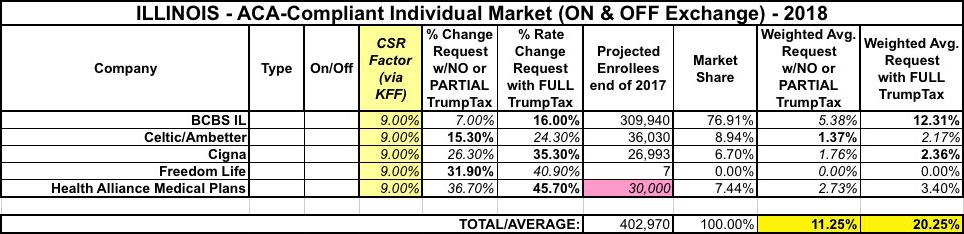

Another major state: Illinois. I've decided to scrap the "Low/High Increase" columns since they just confused people and made the table too wide, but replaced them with a new column showing the CSR factor estimate according to the Kaiser Family Foundation. Note that the percent listed will be smaller than Kaiser's estimate for each state, because their numbers only apply to silver plans, not all metal levels.

For instance in Illinois, Kaiser estimates that carriers would have to raise rates by 14% on Silver plans to cover their CSR losses. However, only 64% of Illinois exchange enrollees have silver plans to begin with, so I'm only plugging in about 9%. There are 5 carriers operating on the Illinois individual market (well, really 4, since "Freedom Life" doesn't count). I have the hard enrollment numbers for 4 of the 5; for Health Alliance Medical Plans I used 30,000 based on their 2016 number. Overall, Illinois is looking at around 11.3% w/partial sabotage, 20.3% with full sabotage: