...With the recent trend of more & more states (most recently including Georgia) splitting off from the Federally Facilitated Marketplace (FFM) hosted via HealthCare.Gov, it's hardly surprising...but it's still a pretty big deal, especially given that Illinois is the 6th largest U.S. state by population. Via Amy Lotven of Inside Health Policy:

Illinois’ Department of Insurance would be authorized to operate a state-based exchange, starting in plan year 2026, under legislation introduced late Thursday by the Illinois Democratic House Majority Leader Robyn Gabel. Sources earlier this week told IHP they had heard state officials were working with lawmakers on exchange legislation and the bill could be unveiled by this week.

I had heard that this was in the works, and with the recent trend of more & more states (most recently including Georgia) splitting off from the Federally Facilitated Marketplace (FFM) hosted via HealthCare.Gov, it's hardly surprising...but it's still a pretty big deal, especially given that Illinois is the 6th largest U.S. state by population. Via Amy Lotven of Inside Health Policy:

Illinois’ Department of Insurance would be authorized to operate a state-based exchange, starting in plan year 2026, under legislation introduced late Thursday by the Illinois Democratic House Majority Leader Robyn Gabel. Sources earlier this week told IHP they had heard state officials were working with lawmakers on exchange legislation and the bill could be unveiled by this week.

I'd never heard of Illinois state Senator Laura Fine before now. I know absolutely nothing else about her besides her being a Democrat who represents IL Senate District 9.

MICHIGAN: Another One (Mostly) Bites The Dust; 12th CO-OP Drops Off Exchange, May Go Belly-Up

It appears that East Lansing-based Consumers Mutual Insurance of Michigan could wind down operations this year as it is not participating in the state health insurance exchange for 2016.

But officials of Consumers Mutual today are discussing several options that could determine its future status with the state Department of Insurance and Financial Services, said David Eich, marketing and public relations officer with Consumers Mutual.

Consumers Mutual CEO Dennis Litos said: "We are reviewing our situation (financial condition) with DIFS and should conclude on a future direction this week.”

While Eich said he could not disclose the options, he said one is “winding down” the company, which has 28,000 members, including about 6,000 on the exchange.

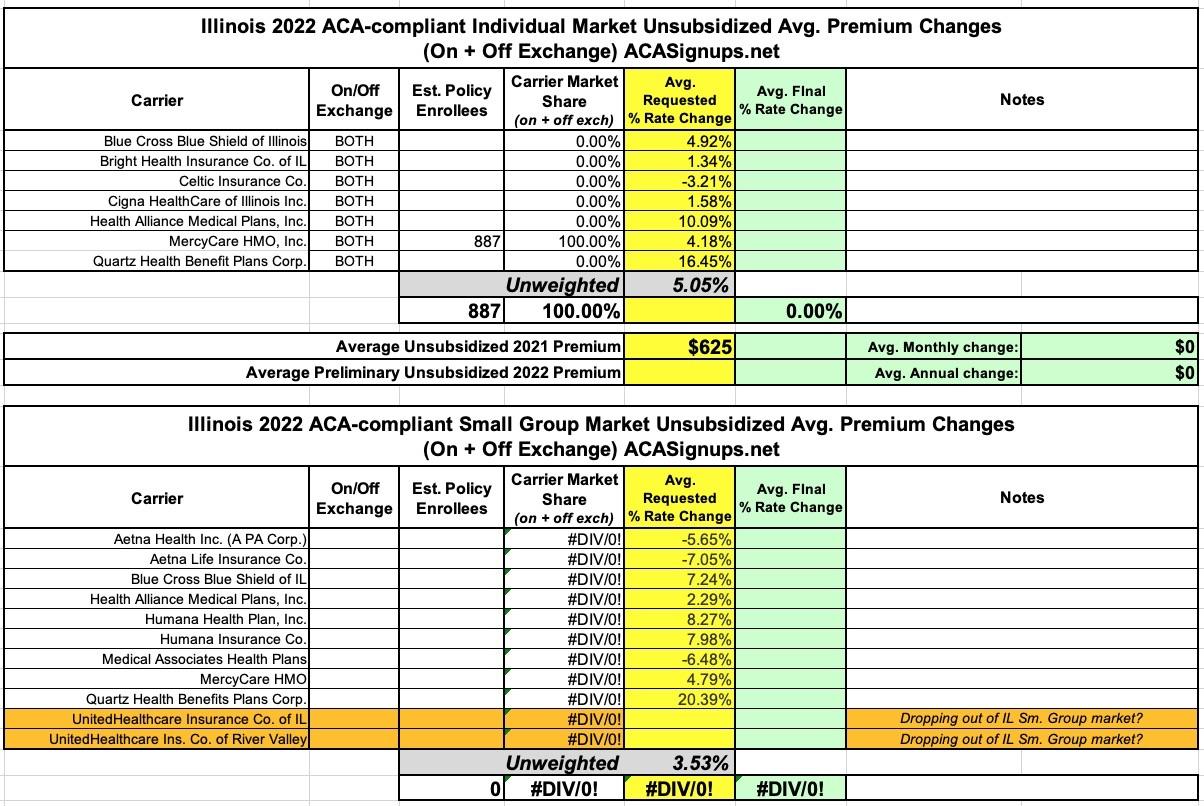

Unfortuantely, Illinois is another state which doesn't make it easy to analyze annual health insurance premium rate filings.

There's no details on their insurance department website, their SERFF listings don't seem to include the actuarial memos or URRT forms, and even the federal Rate Review listings only include the average requested rate changes; the actuarial memos there are mostly heavily redacted.

Illinois' total individual market enrollment should be roughly 330,000 people. Fortunately, three of the carriers do reveal their 2022 enrollment, including the biggest one in the state (Blue Cross). This allows me to make an educated guess as the the enrollment of the other 7, which in turn means I can make an estimate of the weighted rate increase of roughly 6.9%. The unweighted average is 8.9%.

For the small group market I have to go with the fully unweighted average of 6.8%.

UPDATE 11/03/22: With the official 2023 Open Enrollment Period underway, Illinois final/approved rate filings have been posted to the federal rate review website. Not much changed, however...most of the filings have been approved as is, with the exception of MercyCare HMO and Oscar Health Plan.

As I noted last night, thanks to the federal Rate Review website finally being updated to include the final, approved 2022 rates for both the individual and small group markets in all 50 states (+DC), I've been able to fill in the missing data for my annual ACA Rate Change Project.

As I note there, the overall weighted average looks like it'll be roughly +3.5% nationally.

Normally I write up a separate entry for both the preliminary and approved rate changes in each individual state, but it seems like overkill to create 14 separate entries at once. Besides, in many of these states there's been few if any changes between the preliminary and approved rate changes.

Unfortuantely, Illinois is another state which doesn't make it easy to analyze annual health insurance premium rate filings. There's no details on their insurance department website, their SERFF listings don't seem to include the actuarial memos or URRT forms, and even the federal Rate Review listings only include the average requested rate changes; the actuarial memos there are mostly heavily redacted.

The unweighted average rate changes requested for 2022 come in at +5.1% for the individual market and +3.5% for small group plans. It's worth noting that neither of the UnitedHealthcare listings from 2021 (on the small group market) show up in the federal database, which either means they're pulling out of the Illinois market entirely or they just haven't been added to the listings yet. Given that it's mid-October, the former seems more likely.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In some states I've been able to get more recent enrollment data from state websites and other sources.

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

{kind=link}