As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

Obamacare premiums will raise a staggering 76 percent on average for Oklahoma residents, and the state's top insurance regulator says the state's insurance exchange set up by the law is on "life support."

Oklahoma's Insurance Department said on Tuesday that increases in individual marketplace plans will range from 58 percent to 96 percent.

"These jaw-dropping increases make it clear that Oklahoma's exchange is on life support," said Insurance Commissioner John Doak, in a statement. "Health insurers are losing massive amounts of money. If they don't raise rates they'll go out of business. This system has been doomed from the beginning."

Lots of stuff happening fast & furious these days as #OE4 approaches. Instead of individual posts, I'm gonna cram 7 state updates into a single one...and am also cheating a bit by cribbing off of excellent work by Louise Norris over at healthinsurance.org (which is fair, since she also gets some of her data from me as well):

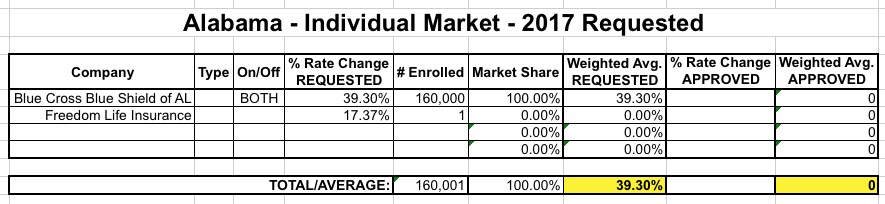

ALABAMA: Here's what my requested rate hike table looked like for Alabama on August 1st:

Oklahoma's entire individual market (including grandfathered/transitional plans) was around 172,000 people in 2014. Assuming it's grown roughly 25% (in line with the national increase), it should be up to perhaps 215,000 people by today, of which perhaps 195K are ACA-compliant.

This is significant because there appear to be only 3 carriers offering individual policies in Oklahoma next year...one of which is the infamous "Freedom Life Insurance Co." which I wrote about last night. Since Freedom Life has (as usual) only a single enrollee in the state, it's really a nonfactor for calculating the weighted rate hike average.

That leaves Blue Cross Blue Shield of Oklahoma, which has a whopping 170,000 enrollees...and CommunityCare (which is in turn broken into HMO and PPO divisions)...unfortunately, their rate filing doesn't include their enrollment number; all it says is that it's "too small to be credible" to be used as the basis of their rate hike request. In addition, UnitedHealthcare is dropping out of the OK indy market; I don't know how many enrollees they actually have.

The conventional wisdom when it comes to taxes is that Republicans are always for cutting 'em while Democrats are always for raising 'em. The reality, of course, can be far more complicated--it's not just about cutting or raising taxes, it's also about who's getting the increase/decrease and what the money would/no longer would be used for. Even so, this is an odd-sounding story at first glance.

Just last week, the Big News Shocker out of Oklahoma was the blood-red Republican-controlled state legislature and governor were actually considering a) raising taxes (!!!) and b) expanding Medicaid via the ACA (!!!) in order to dig themselves out of their self-dug financial hole:

So, in what would be the grandest about-face among rightward leaning states, Oklahoma is now moving toward a plan to expand its Medicaid program to bring in billions of federal dollars from Obama's new health care system.

What's more, GOP leaders are considering a tax hike to cover the state's share of the costs.

Despite bitter resistance in Oklahoma for years to President Barack Obama's health care overhaul, Republican leaders in this conservative state are now confronting something that alarms them even more: a huge $1.3 billion hole in the budget that threatens to do widespread damage to the state's health care system.

So, in what would be the grandest about-face among rightward leaning states, Oklahoma is now moving toward a plan to expand its Medicaid program to bring in billions of federal dollars from Obama's new health care system.

What's more, GOP leaders are considering a tax hike to cover the state's share of the costs.

"We're to the point where the provider rates are going to be cut so much that providers won't be able to survive, particularly the nursing homes," said Republican state Rep. Doug Cox, referring to possible cuts in state funds for indigent care that could cause some hospitals and nursing homes to close.

In a classic case of missing the forest for the trees, I posted two very wonky, detailed entries over the past couple of days about Minnesota and Connecticut's latest enrollment numbers...but completely missed one crucially important data point.

Just how grim the state’s budget situation has become was apparent Wednesday morning as the state House of Representatives discussed and ultimately agreed to a bill that would cut 111,000 Oklahomans, most of them women, from Medicaid.

Oklahoma is an example of how frustrating this rate review stuff can be, even when there's only a handful of companies involved and much of the data is easily accessible.

According to RateReview.Healthcare.Gov, Oklahoma only has a single company asking for rate hikes greater than 10%: Blue Cross Blue Shield of OK.

The main listing gives the requested rate increase as a jaw-dropping 43.95%...but the description below it says that "the range of rate increases by product is 22% to 34%".

Now, there are two additional BCBSOK listings on the Rate Review site which do appear to be included in the first one (all 3 list the total "members affected" as exactly 137,506)...but the other two have 22.64% and 33.83% listed as the "official" requested rate increase, both of which are still well below 44%.

How on earth you can have the individual product rate hikes range from 22-34% but average 43.95%, I have no idea. Obviously I'm missing something here.