But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

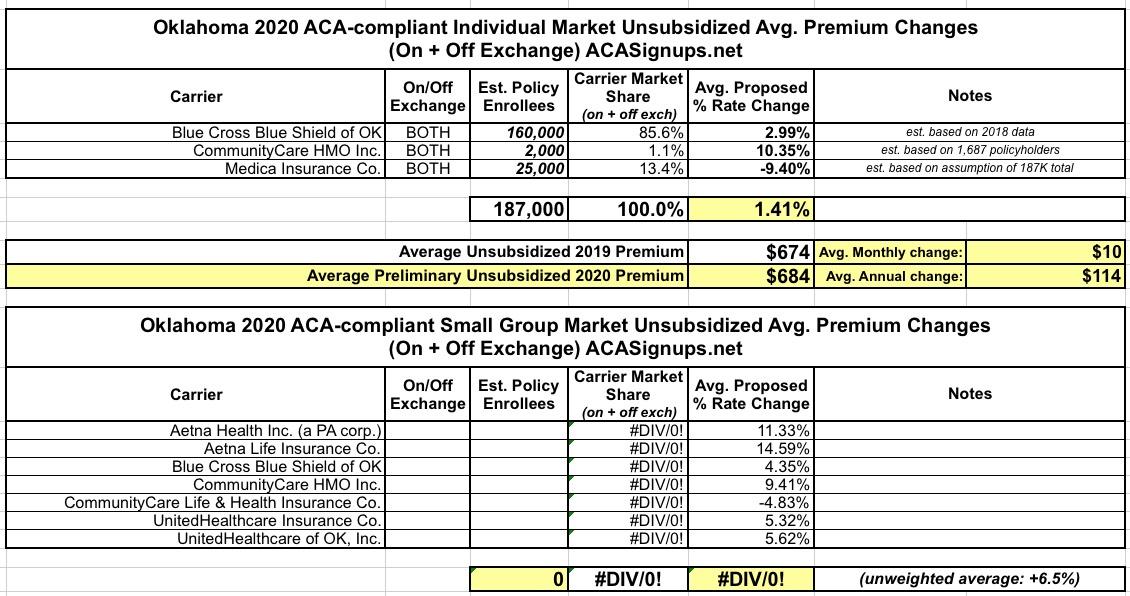

Oklahoma has three carriers on the Individual Market these days. Once again, all three rate filing memos are redacted, but I was able to dig up the number of current policy holders for one of them (CommunityCare HMO).

I've bumped that number up a bit to account for the total number of covered lives to an even 2,000. For the other two carriers, I'm assuming Blue Cross Blue Shield still holds the lion's share of enrollees and that the total on+off-exchange market is around 187,000 people.

If this is all correct, the weighted average rate increase for unsubsidized enrollees is around 1.4% statewide.

Meanwhile, the unweighted average rate hike for the small group market is 6.5%.

Bill expanding ‘Insure Oklahoma’ program passes Senate committee

A Senate bill seeking to expand the Insure Oklahoma program has advanced out of committee Monday morning.

Senate Bill 605, authored by Sen. Greg McCortney, R-Ada, directs the Oklahoma Healthcare Authority to implement "the Oklahoma Plan" within Insure Oklahoma. An agency spokesperson said the program provides premium assistance to low-income working adults employed by small businesses.

The latest numbers from Insure Oklahoma show less than 19,000 are enrolled.

According to McCortney, the intent of his bill is to provide insurance for Oklahomans who would qualify for Medicaid in states which opted to expand but are currently not insured.

Bill expanding ‘Insure Oklahoma’ program passes Senate committee

A Senate bill seeking to expand the Insure Oklahoma program has advanced out of committee Monday morning.

Senate Bill 605, authored by Sen. Greg McCortney, R-Ada, directs the Oklahoma Healthcare Authority to implement "the Oklahoma Plan" within Insure Oklahoma. An agency spokesperson said the program provides premium assistance to low-income working adults employed by small businesses.

The latest numbers from Insure Oklahoma show less than 19,000 are enrolled.

According to McCortney, the intent of his bill is to provide insurance for Oklahomans who would qualify for Medicaid in states which opted to expand but are currently not insured.

It isn't often that I write about anything Oklahoma-related, and it's rarer still that I post good news out of the...um..."labor omnia vincit" state (that's their slogan, I looked it up...), so today's a rare day indeed.

Oklahoma is pretty clear cut: BCBSOK holds nearly all of the ACA-compliant market share, with CommunityCare HMO having a small number of off-exchange enrollees (the numbers are estimates based on last year's figures).

The Urban Institute projected an 18.4% rate increase due to #MandateRepeal and #ShortAssPlans. BCBSOK doesn't go into specifics about the impact, but does list both of these as significant factors. Knocking 1/3 off this projection gives around 12.4%.

Unsubsidized Oklahoma enrollees are paying an average of $694/month in 2018. Without ACA sabotage, they'd likely see this drop to around $595; instead, they're likely looking at paying roughly $681/month, or an additional $1,033 apiece.

A couple of weeks ago, a joint letter was sent to all four Congressional leaders from AHIP (America's Health Insurance Plans), the BlueCross BlueShield Association, the American Academy of Family Physicians, the AMA, the American Hospital Association and the Federation of American Hospitalsm warning them, in no uncertain terms, of what the consequences of repealing the individual mandate would be:

We join together to urge Congress to maintain the individual mandate. There will be serious consequences if Congress simply repeals the mandate while leaving the insurance reforms in place: millions more will be uninsured or face higher premiums, challenging their ability to access the care they need. Let’s work together on solutions that deliver the access, care, and coverage that the American people deserve.

Still, I don't like loose ends, and those 8 missing states are bugging me, so I still want to fill them in for completeness' sake. The only big state remaining is Texas, but I'm also missing Alabama, Hawaii, Iowa, Missouri, New Hampshire, Oklahoma and Wyoming.

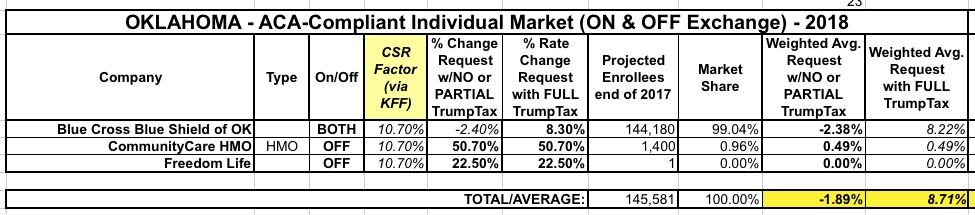

Last year, Blue Cross Blue Shield of Oklahoma, as the only carrier participating on the ACA exchange in the state, jacked up their premiums by a jaw-dropping 76%. This resulted in the highest statewide average rate hike in the country of 71% overall.

Well, that certainly seems to have done the trick: This year BCBSOK (still the only on-exchange player and holding over 99% of the market anyway) is requesting a (relatively) modest 8.3% average rate increase...and their filing specifically calls out both the CSR and mandate enforcement factors as being major reasons. Assuming the Kaiser Family Foundation's estimates are accurate, that means that if the CSR payments were guaranteed for 2018, BCBSOK should actually be lowering their rates slightly, to the tune of around 2.4%.

Adding in the steep hikes from off-exchange only CommunityCare (which only has 1,400 enrollees) brings the averages in at a 1.9% rate drop if CSRs are paid, and an 8.7% increase if they aren't.

While I've been embroiled in the sturm und drang at the national level, Louise Norris of healthinsurance.org has been reporting on some important stuff happening at the state level:

As of 2017, Hawaii no longer has a SHOP exchange for small businesses. The State Department of Labor and Industrial Relations has an FAQ page about this.

...Hawaii’s waiver aligns the ACA with the state’s existing Prepaid Health Care Act. Under the Prepaid Healthcare Act, employees who work at least 20 hours a week have to be offered employer-sponsored health insurance, and can’t be asked to pay more than 1.5 percent of their wages for employee-only coverage (as opposed to 9.69 percent under the ACA in 2017).