Texas' annual health insurance rate filings are kind of a mixed bag in terms of transparecy. Hardly any of the carriers have Uniform Rate Review Template (URRT) forms or Rate Filing Justification Form Part II available (these are the documents which generally include the actual number of people enrolled in the policies for each market for that insurance carrier), and the Actuarial Memorandum (Part III) is heavily redacted for most of them, making it very difficult to lock in the actual enrollment numbers.

On the other hand, a few of them do offer one or both of the former documents, and in a few cases I was able to get the policyholder figures via the SERFF database. I'm operating on the assumption that each individual market policy has roughly 1.5 covered lives apiece on average.

Unfortunately, without having even that estimate available for half the carriers offering policies in Texas, I can't run a weighted average increase (it comes to +4.9% using what I have available), so I'm left (once again) with an unweighted average of around +1.5% on the individual market and +6.1% for small group policies.

There are 9 states where I've been unable to track down the actual enrollment data for individual market carriers. North Dakota is among them.

The unweighted average rate increase for 2022 is 6.0% for the ND individual market and 5.3% for the small group market, which consists of the same three carriers (UnitedHealthcare was a fourth participant in ND's small group market in 2021, but they aren't listed in the federal Rate Review database as of this writing, so I'm assuming they're pulling out).

Virginia has an extremely robust, competitive individual & small group insurance market...and in 2022 it's getting even more competitive, with three new carriers joining the individual market: Aetna, Bright and Innovation Health Plan.

Beyond that, I don't see any shocking or dramatic developments for 2022; average unsubsidized individual market premiums are dropping by 2.9% statewide, while average small group premiums are increasing by 3.6% overall.

West Virginia has the second-smallest ACA individual market enrollment total (Alaska has the smallest), while also being one of the only states left which has (until 2022) refused to use #SilverLoading in their premium pricing strategy to provide some relief to moderate-income indy market enrollees.

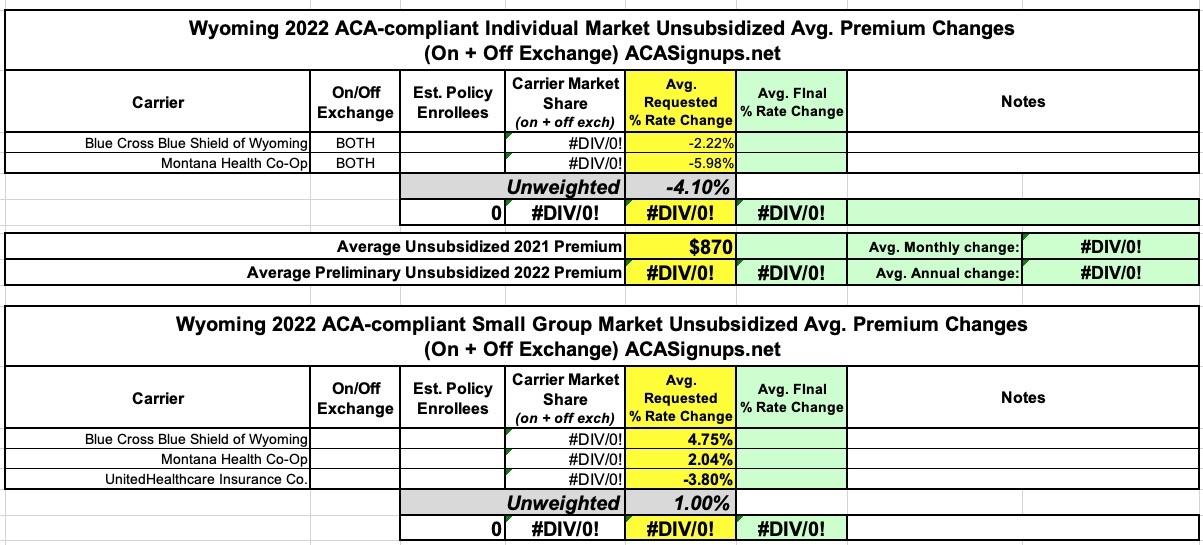

As a result of this and other factors, they now have the highest unsubsidized individual market policy premiums in the country (19% higher than the prior record-holder, Wyoming, which averaged $870/month in 2021), at $1,038/month per enrollee.

In 2022, this is gonna be even more jaw-dropping, as the approved rate increases for WV's carriers will average 12.8%, bringing the average premium up to a whopping $1,171/month per person.

I'm pretty sure Wisconsin has the most competitive ACA markets in the country, at least in terms of the sheer number of insurance carriers offering policies on both the individual and small group markets. A total of 37 are present at the moment, although 5 of the small group carriers don't appear on the federal Rate Review database as of yet.

Unfortunately, this is yet another state where the enrollment data has basically been buried, so I can only run unweighted average rate changes.

With that in mind, the individual market rates look to be nearly flat (dropping by 0.8% on average), while small group plans are going up 4.4%.

Vermont's 2022 rate filings are pretty straightforward: They only have two carriers in the state offering either individual or small group plans to begin with, and the insurance department clearly states not only the requested and approved rate changes, but the exact number of enrollees each carrier has.

There's one major change this year, however: After many years of having their individual & small group risk pools merged, Vermont has decided to unmerge the two (I believe Massachusetts is the only other state which has a combined indy/small group risk pool). The press releases for rate filings in each explains the rationale:

Utah has an elaborate, color-coded public database which lets you search for health insurance rate filings for not just the current and upcoming year, but also for years dating back nearly a decade. It can be a bit confusing (for instance, the "Latest Rate Changes" section on the main page is currently blank even though both the individual and small group plans for 2022 were all recently approved), but it's still a lot better than most states offer.

Between this database and Utah's SERFF listings, I've been able to put together the full requested and approved filings for every carrier in both markets, along with the enrollment numbers for each, allowing for weighted average increases.

Individual market enrollees are looking at roughly a 1% average unsubsidized rate increase, while small group plans are goin gup about 4.5% overall. From what I can tell, WMI Mutual is dropping off the small group market, but they don't have anyone enrolled in their policies right now anyway.

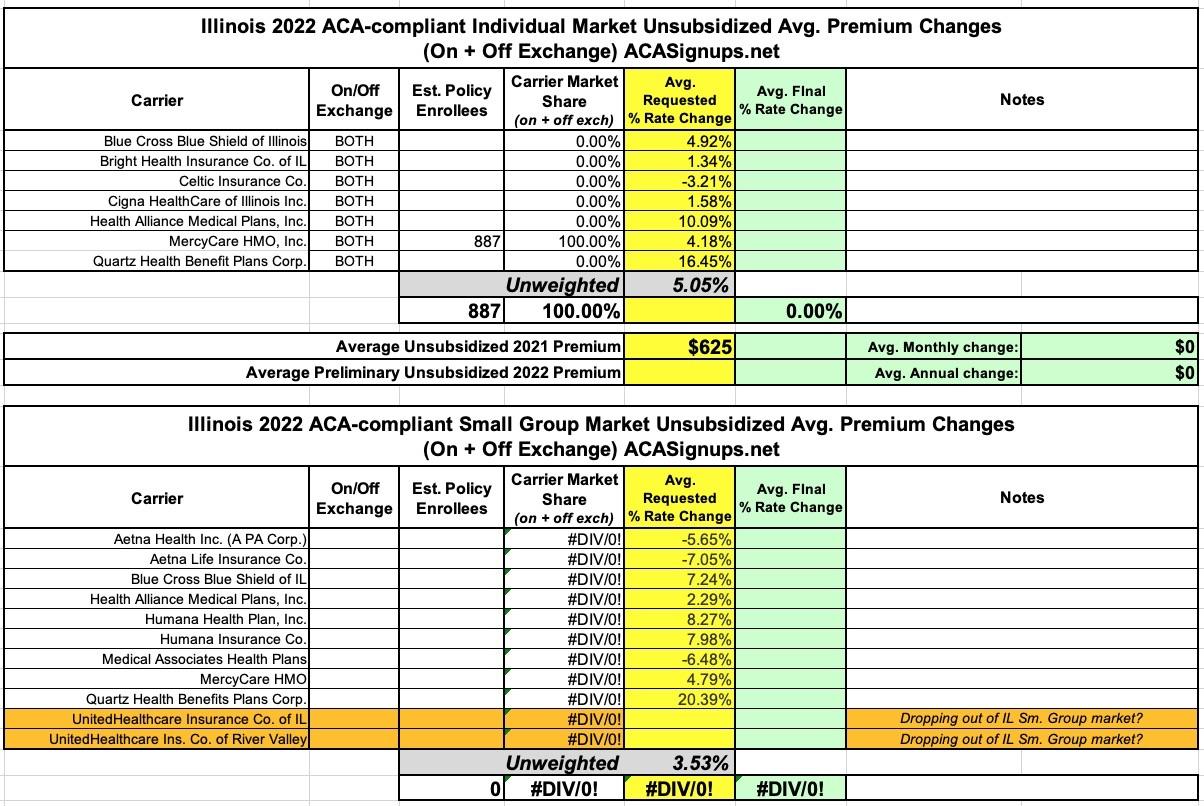

Unfortuantely, Illinois is another state which doesn't make it easy to analyze annual health insurance premium rate filings. There's no details on their insurance department website, their SERFF listings don't seem to include the actuarial memos or URRT forms, and even the federal Rate Review listings only include the average requested rate changes; the actuarial memos there are mostly heavily redacted.

The unweighted average rate changes requested for 2022 come in at +5.1% for the individual market and +3.5% for small group plans. It's worth noting that neither of the UnitedHealthcare listings from 2021 (on the small group market) show up in the federal database, which either means they're pulling out of the Illinois market entirely or they just haven't been added to the listings yet. Given that it's mid-October, the former seems more likely.

Like Wyoming, Alaska is also a sparsely populated state with only two carriers on their individual market and three (possibly four?) on their small group market. Also like Wyoming, Alaska's insurance department website is useless when it comes to getting rate filings or enrollment data; I had to use the federal Rate Review site to even get the requested rate changes.

Fortunately, Premera Blue Cross includes a summary which lists their enrollment numbers, and with Moda being the only other carrier on the market, I was able to estimate a weighted average (assuming Moda only has around 2,000 enrollees, which seems about right given Alaska's total on-exchange enrollment of roughly 18,000 people).

On the small group market, only three carriers are listed in the federal database; Premera Blue Cross isn't, which either means they're pulling out of the state's small biz market or they just haven't been added to the database yet.

Average rate change for unsubsidized enrollees in 2022 will be 10.6% on the individual market...except that almost every enrollee will qualify for financial subsidies this year. On the small group market, the unweighted average increase is 6.4%.

Wyoming is the smallest state and only has two carriers offering individual market policies (and just three offering small group plans). This makes it pretty simple for me.

Unfortunately, neither their insurance department website nor their SERFF filings give any indication of the enrollment numbers for any of the carriers, making it impossible to calculate a weighted average for either market. Then again, assuming a roughly even market share split, the unweighted averages should be pretty close: -4.1% individual market, +1.0% small group.