Last week I urged Democrats to demand Congressional Republicans rein in the Trump Regime's out-of-control dictatorial rampage as well as going big on healthcare policy as part of the "government shutdown" battle...but that to the extent that they do make the main focus healthcare policy, at the very least to not settle for simply bumping out the enhanced ACA tax credits by a year or two:

You know I'm a pretty mainstream Democrat. I'm not demanding Medicare for All here. What I am urging on the healthcare front is for three clear demands:

This is gonna be one of the stranger references I've made on this site, but bear with me.

Back in 1996 there was an HBO movie called "The Late Shift" which told the story of the Late Night TV show battle between David Letterman and Jay Leno over who would succeed Johnny Carson as host of The Tonight Show. As stupid as this may sound today, this was actually a Really Big Deal in the '90's...one of those absurd pop culture stories which dominated the headlines and the tabloids for several years.

The movie itself was decent, with some interesting casting including Kathy Bates and Treat Williams, but nothing special. The main problem is that the audience is expected to root and feel sympathy for a couple of dudes who were already rich & famous and who would both continue to be rich & famous no matter how the story played out. The stakes weren't exactly the fate of the world, is what I'm saying.

The looming disaster on Obamacare subsidies keeps looking worse

Congressional Democrats are confronting a ticking time bomb that threatens both the health security of millions of Americans and Democrats’ own political security in the midterm elections. If they don’t act fast, it’s going to explode.

...Now, another group of Democrats outside Washington is getting increasingly nervous about this prospect. Democratic governors, many of whom are up for reelection this year, don’t want to watch while Congress makes life more difficult for their constituents.

Underscoring the point, a group of Democratic governors has released a new letter imploring congressional leaders to extend the enhanced subsidies.

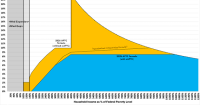

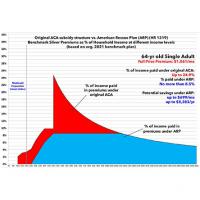

Once again, here's what the Affordable Care Act's premium subsidy tables look like under the original ACA itself and under the American Rescue Plan (ARP). The premium caps are the maximum percent of household income which a household has to pay for the benchmark Silver plan at various income ranges.

The ARP table is currently scheduled to sunset at the end of December, at which point, without legislation passing Congress & being signed into law by President Biden, it will revert back to the original ACA subsidy table:

Again, here's what the subsidy tables look like under the ACA itself and under the American Rescue Plan. The premium caps are the maximum percent of household income which a household has to pay for the benchmark Silver plan at various income ranges:

The Biden-Harris Administration is announcing that, beginning today, as many as 720,000 pregnant and postpartum people across the United States could be guaranteed Medicaid and Children’s Health Insurance Program (CHIP) coverage for a full 12 months after pregnancy thanks to the American Rescue Plan (ARP). Medicaid covers 42 percent of all births in the nation, and this new option for states to extend Medicaid and CHIP coverage marks the Biden-Harris Administration’s latest effort to address the nation’s crisis in pregnancy-related deaths and maternal morbidity by opening the door to postpartum care for hundreds of thousands of people.

New Mexico would raise a state health-insurance tax and dedicate the new revenue to programs intended to make health care more affordable under a proposal that passed the state House on Sunday.

Rep. Deborah Armstrong, D-Albuquerque, described the legislation as an unusual opportunity to generate more revenue for health care without increasing the total amount consumers now pay.

The increased state tax would partially replace a federal tax that’s being repealed, she said, meaning health insurance carriers would actually be charged less in taxes than they are now, even after the state increase.

The legislation, House Bill 278, would raise about $125 million in annual revenue when fully phased in — the bulk of it dedicated to a new fund for health care affordability, according to legislative analysts.

For years now, I've been a tireless advocate for dramatically expanding & improving the Affordable Care Act's Advance Premium Tax Credit (APTC) formula. This is the table which determines a) just how generous the ACA's health insurance premium tax credits are at different income levels and b) how far up the income ladder those financial subsidies extend.

Just over a year ago, the American Rescue Plan (ARP), passed by Democrats in Congress and signed into law by President Biden, did exactly what I've been clamouring for all this time: It made ACA subsidies far more generous while also removing the completely arbitrary income eligibility cut-off threshold (otherwise known as the "Subsidy Cliff."

As a refresher, the way the ACA subsidies work is as follows:

A new Covered California analysis describes the potential impact to consumers if the increased health insurance subsidies that were part of the American Rescue Plan are allowed to expire at the end of 2022.

In California, all consumers would face premium increases, including 1 million lower-income consumers (individuals earning less than $32,200 per year), who would see their premiums more than double.

In addition, middle-income individuals and families (for individuals, those earning more than $51,520 per year), would no longer be eligible for any financial help and would face higher monthly premium costs that for many will mean annual cost increases in the thousands of dollars.

The increase in costs could force more than 150,000 people in California and more than 1.7 million nationally to drop their health insurance.