Nebraska doesn't even bother listing indy/small group plan rate filings on their own insurance department website...the link goes directly to the federal Rate Review database. The problem with this is that very few filings here are unredacted, which means it's difficult to acquire the policy enrollees for many carriers needed to run a weighted average.

Fortunately, Nebraska has only 3 carriers for 2022...one of which is brand new to the state (Oscar Health), and of the other two, Medica's filing summary does include an exact number of enrollees. That leaves just Bright Health, and since I know (roughly) how many enrollees are in Nebraska's overall indy market, voila: 8.6% average rate increases.

On the other hand, I don't have the enrollment for any of the 4 Small Group market carriers. It also looks like UnitedHealthcare is pulling out of the NE sm. group market, but it might just be that the federal database doesn't have them listed yet (I doubt this since it's so close to the Open Enrollment Period). The unweighted average rate change is a 2.1% reduction:

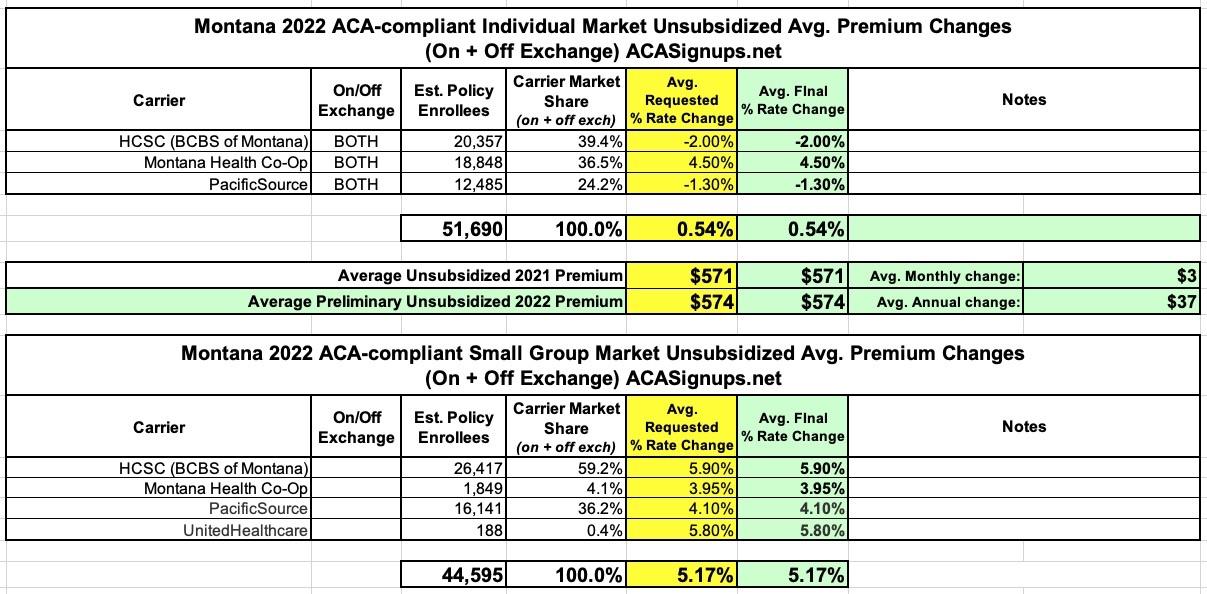

Seriously, if every state displayed their annual rate filing data in as simple and clear-cut a fashion as Montana does, I'd be a much happier man. Admittedly, several others do, but the trickiest issue is usually getting the estimated enrollment numbers.

In any event, not much to say about Montana's ACA markets in 2022: No new carriers are jumping in, no current ones are dropping out, and the rate changes are pretty straightforward: +0.5% on the individual market, +5.2% on the small group market.

UPDATE 10/22/21: Well, it looks like the Montana Insurance Dept. has signed off on all 7 rate filing requests without making any changes, so I guess these are the approved rate changes as well:

Georgia's health department doesn't publish their annual rate filings publicly, but they don't hide them either; I was able to acquire pretty much everything via a simple FOIA request which was responded to within a few hours of my asking.

As of 2021, there are six insurers that offer exchange plans in Georgia. Five additional insurers plan to join them for 2022: Friday Health Plans, Bright Health, Aetna, UnitedHealthcare, and Cigna (Aetna, UHC, and Cigna all participated in Georgia’s exchange previously, but left at the end of 2016).

It's worth noting that each market has a new entrant for 2022: Aetna is joining the individual market while Cigna is jumping into the off-exchange Small Group market.

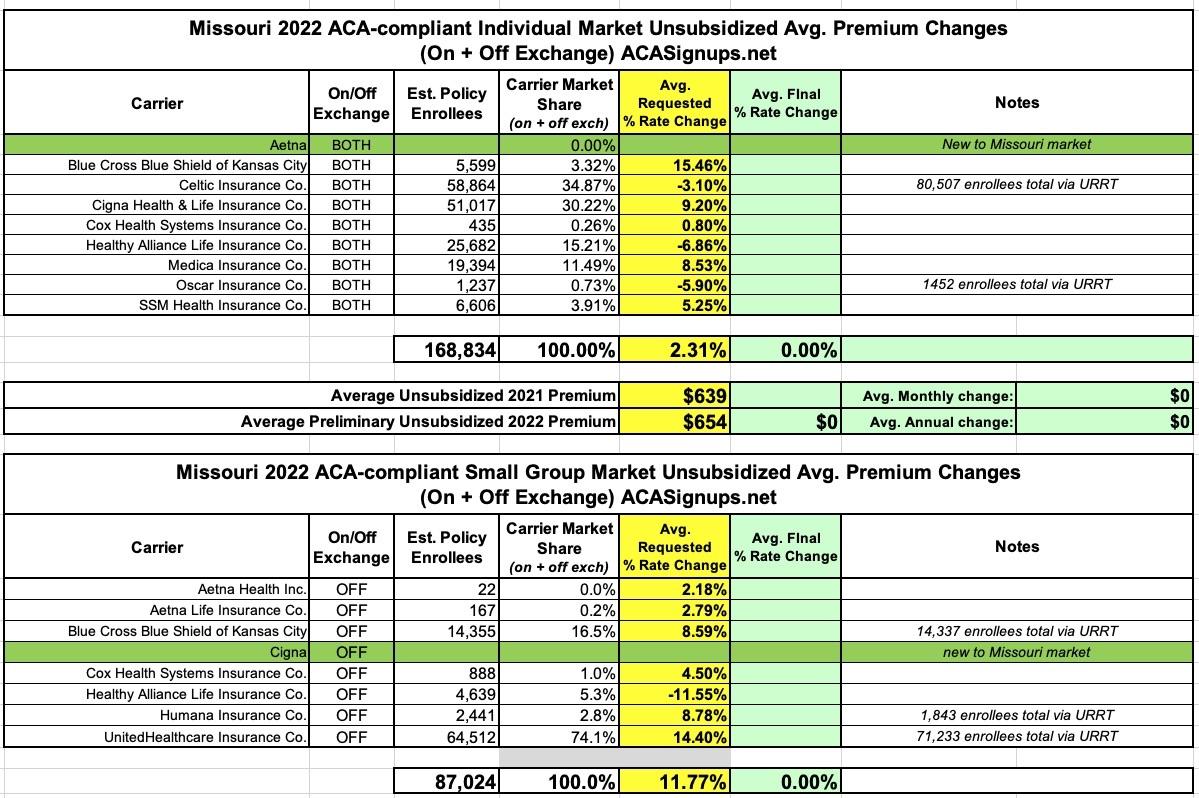

The differences in enrollment noted for some carriers is likely due to some product lines being discontinued--for instance, if Celtic drops premiums by 3.1% on most of their policies but discontinues some others entirely, those enrolled in the discontinued lines won't have any official rate change to their existing policies.

Florida state law apparently gives private corporations wide berth as to what sort of information, which is easily available in some other states, they get to hide from the public under the guise of it being a "trade secret."

In the case of health insurance premium rate filing data, that even extends to basic information like "how many customers they have."

Cigna is joining the Mississippi exchange for 2022, bringing the total number of participating insurers to three. According to ratereview.gov, the following average rate changes have been proposed by Mississippi’s current exchange insurers:

The Minnesota Commerce Dept. has posted preliminary 2022 ACA rate filings for the individual and small group markets. Final/approved rate changes will likely be posted in just a few weeks.

Overall I don't see any significant changes to the offerings from 2021 other than PreferredOne appearing to eliminate one of their two lines on both markets. Also, UnitedHealthcare of Illinois appears to be scrapping their entire line of existing plans on the small group market and replacing them with all-new policies, which means there's technically no current rates for them to compare against.

The other important thing to keep in mind for the small group market is that I can't seem to find the actual current enrollment data for each carrier, so I'm basing the weighted average on 2020 enrollment, which could be way off if there's been significant market share shifts this year.

State Receives Marketplace Modernization Grant, Awarded by Centers for Medicare & Medicaid Services (CMS) Under American Rescue Plan Act

ALBANY, N.Y. (September 17, 2021) – NY State of Health, the state’s official health plan Marketplace, today announced it has been awarded a Marketplace Modernization Grant by the Centers for Medicare & Medicaid Services (CMS). This funding, a total of $1.1 million dollars, the maximum awarded to state-based marketplaces, has been made available by the American Rescue Plan Act (ARPA) of 2021 for the purpose of modernizing or updating state technology systems and/or conducting targeted consumer outreach activities that can improve access to health coverage for consumers.

Access Health CT Awarded $1.1M Grant From The Centers For Medicare and Medicaid Services

Grant funding supports the implementation of the American Rescue Plan Act in Connecticut and several technology upgrades improving the consumer experience

HARTFORD, Conn. (September 20, 2021)—Access Health CT (AHCT) announced today it was recently awarded $1.1 million of grant funding from the Centers for Medicare and Medicaid Services (CMS). The grant will be used to financially support the implementation of the American Rescue Plan Act (ARPA) helping to make health insurance more affordable for Connecticut residents, along with technology modernization projects that will enhance consumer experiences within the online customer portal. The grant funding was made possible through the ARPA.

CMS Extends Open Enrollment Period and Launches Initiatives to Expand Health Coverage Access Nationwide

The Biden-Harris Administration, through the Centers for Medicare & Medicaid Services (CMS), is taking a number of steps that will make it easier for the American people to sign up for quality, affordable health coverage and reduce health disparities in communities across the country. Beginning this year, consumers will have an extra 30 days to review and choose health plans through Open Enrollment, which will run from November 1, 2021 through January 15, 2022, on HealthCare.gov.