The Dead Pool: Paul Ryan's ACA replacement hinges on Concentrating those w/pre-existing conditions into separate Camps.

Fri, 01/13/2017 - 10:01am

Hat Tip To:

Alphonse Beliavsky via Twitter for the too-clever-by-half headline

UPDATE 4/6/17: It looks like the GOP is trying one more time to cram through their much-hated "American Health Care Act" (aka Trumpcare 2.0) bill. The twist this time is that in addition to allowing states to kill off Community Rating and Essential Health Benefits (with the key phrase being "kill"), they'd also make High Risk Pools part of the mix (HRPs were already allowed in the earlier version, but apparently they'd be specifically mandated this time around...I think).

Given this development, I'm re-pinning this entry to the front of the site again.

(Update: Thanks to Griffin Cupstid, MD for the link to the CNN transcript, which allowed me to make some minor wording edits below).

I wrote up a long-ass Twitter thread last night. I've reformatted it for a blog entry this morning:

So, I watched the ACA-related segments of Republican House Speaker Paul Ryan's CNN Town Hall thing last night. He took several questions about the ACA (Obamacare, remember) and Medicare, but I'm just gonna focus on the first one here. The questioner was a self-described lifelong Republican who used to hate the idea of the ACA...right up until he was diagnosed with cancer and given just months weeks to live. Pre-ACA he would have been denied coverage for the pre-existing condition and would have died. He profusely praised the ACA and flat-out thanked President Obama for saving his life. The actual question was "why would Ryan repeal the ACA without a replacement in place."

QUESTION: I was a republican and I worked for the Reagan and Bush campaigns. Just like you, I was opposed to the Affordable Care Act. When it was passed, I told my wife we would close our business before I complied with this law. Then, at 49, I was given six weeks to live with a very curable type of cancer. We offered three times the cost of my treatments, which was rejected. They required an insurance card. Thanks to the Affordable Care Act, I'm standing here today alive.

Being both a small business person and someone with pre-existing conditions, I rely on the Affordable Care Act to be able to purchase my own insurance. Why would you repeal the Affordable Care Act without a replacement?

RYAN: Oh, we -- we wouldn't do that. We want to replace with something better. First of all, I'm glad you're standing here. I mean, really -- seriously.

QUESTION: Can I say one thing? I hate to interrupt you...I want to thank President Obama from the bottom of my heart, because I would be dead if it weren't for him.

After small talk about where they each grew up, Ryan stated--completely contrary to everything that the GOP has been saying over the past couple of weeks--that why yes, they absolutely will have a replacement plan in place at the same time the repeal goes through! Absolutely! You betcha!

For the most part, Ryan's response focused heavily on High Risk Pools. And, to his credit, he was pretty damned blunt about exactly what the Republican philosophy is when it comes to those with expensive pre-existing conditions: Treat them like lepers. Seriously. Watch the clip above again; he stresses at least 3-4 times how vitally important it is to separate out cancer patients (or really, anyone with a highly expensive ailment) into a separate High Risk Pool in order to lower the price for everyone else. Then, you provide a hunk of money to cover those people without "ruining it for everyone else".

Now it's true that once you isolate/quarantine high-expense patients from the rest of the poulation, the cost to treat everyone else does drop significantly...except there's a few problems with this:

First, it still costs just as much to treat the high risk people. Splitting them off hasn't magically made their conditions any less expensive to treat. So the total amount of money to treat everyone is exactly the same, just split up differently. Where does that money come from?

Well, Ryan is proposing a $25 billion risk pool fund over a 10 year period. That sounds like a lot, but it only averages $2.5 billion per year (I presume it's less the first few years, more later on via inflation). According to this article by Ian Milhiser at Think Progress, to adequately cover 875,000 high-risk patients would have cost seven billion per year...and that was in 2008. That's 2.8x as much as Ryan is proposing, and that was 9 years ago (10, if we assume the new plan doesn't go into effect until 2018). I have to imagine that $7B would be up to at least $10B by then, and that's for 875,000 patients.

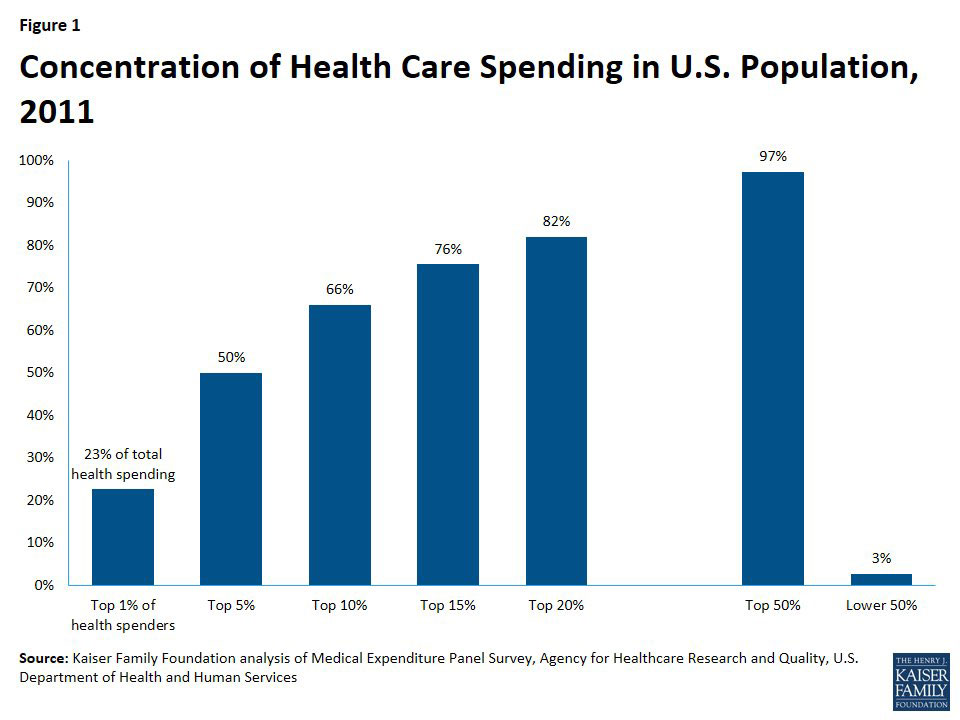

Now, they want to kick up to 30 million people off their policies (I'm not even going to get into the remaining ~28 million uninsured). According to this study by the Kaiser Family Foundation about High Risk Pools (HRPs), 5% of the general population accounts for fully 50% of total healthcare spending, with the other 95% costing the other 50%:

Now, Ryan himself admits that 8% of people under 65 have "the same type" of pre-existing condition that the questioner has...in other words, batshit-expensive ailments like cancer/etc. 8% of 30 million is 2.4 million people. If it costs $10 billion per year for 875K, that's a good $27.5 billion per year for 2.4 million of them. That's eleven times as much as Ryan's plan is promising.

Now, here’s the thing: Ryan claims that state-based high risk pools have “worked well”. Perhaps…IF they're properly funded. If Ryan and the rest of the Republicans move the decimal point to the right by a notch, perhaps we can talk.

But is it really "only" $27.5 billion/year? I wrote a full piece about this a couple weeks back. Here’s what a 2014 Commonwealth Fund study found:

The GOP's "solution" to this is to shove those people off to the side into a separate "High Risk Pool"...which they plan on funding with anywhere between $1 billion - $2.5 billion per year...except that it would actually cost anywhere from 70 - 180 times that much to actually pay for treating these folks:

Price would also use high risk pools to provide coverage for those with pre-existing conditions who couldn't get policies on the individual market. In addition to current funding, he would provide $1 billion annually over three years. This is significantly less than Ryan's plan, which calls for $25 billion in funding over 10 years.

Covering the majority of uninsured Americans with pre-existing conditions through a national high risk pool would cost an estimated $178 billion a year, according to a 2014 Commonwealth Fund report.

Now, the Commonwealth study was referring to covering “the majority of uninsured americans w/pre-existing conditions", which (at the time) was more like 45-50 million people. In this case we're only talking about 30 million, so let's lop that down by 40% and call it $106 billion. Hell, let's cut it down to an even $100 billion. Per year. To cover "most" of those with pre-existing conditions.

Now, you can certainly argue that the Commonwealth numbers are insane, but it sure sounds like we're looking at anywhere between $27 - $100 billion per year just for these 2.4 million people. The point is, it's orders of magnitude higher than Ryan's $2.5 billion.

Oh, but wait, there's more: As I noted a couple weeks ago, some of those "great" (according to Ryan) state HR pools included WAITING LISTS. For a high risk pool. In fact, get this:

Pre-existing condition exclusions – Nearly all state high-risk pools excluded coverage of pre-existing conditions for medically eligible enrollees, usually for 6-12 months. This made coverage less attractive for people who needed coverage specifically for their pre-existing conditions.

(Yes, that's right...even the high-risk pools, designed specifically for those with pre-existing conditions...denied those with pre-existing conditions from enrolling for up to a year. Tough luck if you've been diagnosed with a type of cancer which will kill you in less than a year without treatment).

Lifetime and annual limits – Thirty-three pools imposed lifetime dollar limits on covered services, most ranging from $1 million to $2 million. In addition, six pools imposed annual dollar limits on all covered services while 13 others imposed annual dollar limits on specific benefits such as prescription drugs, mental health treatment, or rehabilitation.

...A small number of states capped or closed enrollment to limit program costs, though enrollment caps were not allowed for HIPAA-eligible individuals. Limiting enrollment, directly or indirectly, was a key strategy to limit the cost of high-risk pools to states. By design, all state high-risk pools experienced net losses – that is, expenses greater than premium revenue.

But hey, they'd receive "access" to coverage "to some degree or another".

There’s a simple reason why GOP loves high risk pools: Even if the total dollar amount remains the same, they can cut funding to HRP, sentencing those 5% to their doom without raising rates on everyone else. Isolate ‘em from the herd. It’s clever if you have no soul.

OK, let's go back to the 5% / 50% thing. Let’s say you have 1 million people in the #ACA exchange pool today, costing $10K/year on average.

That’s $10 billion/year total, with 50,000 of them racking up $5 billion and the other 950,000 racking up the other $5 billion.

So, you isolate those 50K into a HRP. The rates for the other 950K drop nearly in half (from $10K/yr to $5,263/yr). Hooray!

Meanwhile, the 50K HR people cost $100K/year apiece ($5B total) Again, as long as that HRP is fully funded, that's perfectly fine. EXCEPT:

- Assuming it’s fully funded, where does that $5 billion come from? That’s right…taxes. Which presumably includes some taxes on the other 950K…which means they’re still paying *some* of that $5 billion in a different form. But the larger problem...and the truly disturbing part of the HRP concept is this:

- Legislators can now EASILY underfund the HRP right off the bat (as Ryan's plan would), and slash the funding even further down the line, presumably when few people are paying attention. Sure, you’re dooming 5% of the voters, but you’ve made the other 95% oh so happy!

Of course, if you do that at the federal level, it'll probably attract some attention; 2.4 million people being put out on ice floes to die are a big deal, especially when many of them live in blue states where most people actually give a crap about the most vulnerable among us.. But what about at the state level? By an amazing coincidence, Ryan's HRP plan just happens to...turn over control of the HRPs back to the states! Just like they used to do pre-ACA! And while blue states will probably pony up a few more bucks to try and cover the massive funding gap, quite a few red states probably won't bother.

One other thing: In my 5% / 95% example above, we're assuming that the total cost for all 1 million people would remain the same, meaning the 950,000 "normal people" would see their costs drop from $10,000 to just $5,300...a 47% drop, right?

Well, not necessarily. The ACA includes the 80/20 Medical Loss Ratio provision which requires insurance carriers to spend at least 80% of premiums on actual healthcare costs, as opposed to CEO bonuses, marble floors for their headquarters or exotic corporate junkets to Tahiti. If I'm wrong about this point I'll issue a correction, but I'm willing to bet that Paul Ryan's "Better Way" does not impose the same 80% on carriers. After all, "the invisible hand of the free market!" and all that, right?

Not to mention that Ryan's plan strips away most (all?) of the requirements for what has to be covered by the policies the other 950,000...so sure, they could see their rates plummet...along with their coverage, right back to the mini-med junk policies of old.

But I want to go back to my original point: Watch the clip again. Scroll to 6:15.

Ryan rattles off a bunch of (somewhat cherry-picked) high rate hikes, and then says,

“There is a better way to fix that problem without giving EVERYBODY ELSE all these MASSIVE premium increases.”

He’s literally saying “YOU’RE the one fucking it up for the rest of your neighbors!”

Then, at 7:15 he says it again:

“So we, obviously, want to have a system where they can get affordable coverage without going bankrupt because they get sick. But, we can do that without DESTROYING the rest of the healthcare system FOR EVERYBODY ELSE."

Again at 7:30:

"So, by financing state high-risk pools to guarantee people get affordable coverage when they have a pre-existing condition, like yourself, what you're doing is, you're dramatically lowering the price of insurance FOR EVERYBODY ELSE. So, if we say let's just, as taxpayers -- and I agree with this -- finance the coverage for those eight percent of Americans under 65 in a condition like yours -- they don't have to be covered or paid for by their small business or their insurer who is buying the rates for the rest of the people in their insured pool, and you'd dramatically lower the price for the other 92 percent of Americans.

Let's just directly fix that so that EVERYBODY ELSE can get more competitive rates and they don't have to pay for insurance to try to cover for THOSE KINDS OF REALLY EXPENSIVE PEOPLE."

Remember he’s talking TO A CANCER PATIENT IN FRONT OF HIM.

I dunno about anyone else, but that’d make me feel really bad about myself.

As one oncologist put it:

I always make sure my cancer patients know how hard they are making it for the rest of us. https://t.co/AIlCRubJAC

— David Hedrick (@DrHedrick) January 13, 2017

Welcome to Trumpublican America, folks.

UPDATE: Oh for heaven's sake: I just realized that the math here is even simpler than that.

$25 billion over 10 years = $2.5 billion per year. Assuming 2.4 million high risk pool enrollees, that's just $1,041 per person per year.

A thousand dollars per year, per enrollee. In a high risk pool. You know...the pool specifically intended for very expensive-to-treat enrollees.

The average cost for healthcare per person nationally is nearly $10,000 per year (hey, my example above was dead on target!).

UPDATE: Thanks to Jill Burcum and Lynn Blewett for bringing this study of the pre-ACA Minnesota high risk pool (from 2011) for some context:

In 2007, 34 states had individual high-risk pools, which covered more than 200 000 people at a total cost of $1.8 billion.

We examine the experience of the largest and oldest pool in the nation, the Minnesota Comprehensive Health Association, to document key issues facing state high-risk pools in enrollment and financing. We also considered the role and future of high-risk pools in light of national health care finance reform.

OK, right off the bat, that's $1.8 billion (in 2007 healthcare dollars) for 200,000 people, or $9,000 per enrollee per year.

The 200K figure is obviously far lower than my 2.4 million estimate above. Of course, that only includes 34 states; the national number is presumably up to 50% higher (depending on whether this includes large states like California and/or small states like Wyoming). There's also some population growth since 2007. Call it at least 300,000 people who'd need HRP coverage nationally. Plus, of course, the "6-12 month waiting period" annual/lifetime caps and high premiums relative to the rest of the market likely artifically lowered the numbers anyway. I have to imagine that at least another 100K tried to get into a state-based HRP but were denied or simply couldn't afford it....say 400,000 or so overall?

The Kaiser Family Foundation report mentioned above says there were 35 states (one more than Blewett's report) with HRPs just before the ACA went into effect. These were termporarily replaced by a federal HRP which acted as a sort of holding pen until the ACA exchanges could launch:

PCIP was operational in all 50 states by the fall of 2010. By late 2012, just over 100,000 individuals were enrolled and program expenses had consumed nearly half of the $5 billion appropriation. For the final 12-month period for which PCIP expense data were reported, net losses for the program were over $2 billion. (Table 1)

In 2012, average per enrollee claims costs for PCIP were $32,108, or more than 2.5 times higher than average per enrollee claims costs ($12,471) under traditional state high-risk pools, all of which continued to operate that year.9 Compared to traditional state high-risk pool enrollees, PCIP enrollees tended to have more immediate and intensive health care needs, including higher hospital admissions, likely due to the six-month prior uninsurance requirement and lack of pre-existing condition exclusions.

Again, the numbers enrolled were only in the low six figure range, but it sounds like a lot of people were moving around at the time. Both the $32K and $12.5K figures are in 2012 dollars; I presume they'd each be up to around $35K and $14K by 2018 (the absolute earliest that I would imagine a Republican HRP could go into effect).

Even if you assume there's only 400,000 people who would have to enter such an HRP (since they'd be denied anywhere else), $35,000/year x 300K would still be $14 billion...or 5.6x higher than Ryan's budget (and 14x higher than Tom Price, who only wants to spend $1 billion/year on his HRP plan).

If the numbers are closer to the 2.4 million noted earlier, then even at the $14,000 level, you'd be talking about $33.6 billion per year...13x Ryan's allowance, 33x that of Price.

In short, no matter how you slice it, Ryan & Price's High Risk Pool "solutions" suck.

UPDATE: Good grief. I've been informed that Price's version not only limits high risk pool funding to $1 billion per year, but that's only for 3 years...after which he would cut off all federal HRP funding entirely.

UPDATE 1/17/17: Former Vermont Governor, Presidential Candidate and DNC Chair Dr. Howard Dean and Steven Brill, who wrote the definitive backstory behind the development of the Affordable Care Act, were interviewed by Lawrence O'Donnell last night regarding Trump's "Insurance for Everyone!" nonsense but also discussed the "High Risk Pool" bullet point that Ryan & Co. keep trying to push.

Crooks & Liars has the video & full transcript, but I wanted to focus on the HRP portion; Brill confirms my main point here:

BRILL: It's ridiculous. Besides the issue with health care, as Dr. Dean knows, is not the insurance companies because they pay for health care, the issue is the price of health care that we pay as patients and that insurance companies pay.

The other thing I think they're gonna do and I think we need to educate everyone in the country though, beware of three words "high-risk pools." That's what they are going to sell. They are going to provide "insurance for everybody" by putting people who are sick and with pre-existing conditions into high-risk pools. That's exactly what was done before Obamacare.

There were waiting lists. There were caps on coverage, $50,000 a year, $100,000 lifetime, depending on the state. Everybody had to pay premiums of 150, 200% more than everybody else. If you take all the sick people and put them into one pool and the healthy people in another pool, the healthy people get lower premiums because they are in a pool with just healthy people but sick people suffer and that's the opposite purpose of insurance which is to spread the risk. That's the scam of high-risk pools. It never worked.

Advertisement