The good news is that Wisconsin has one of the most robust and competitive exchange markets in the country. The bad news is that, contrary to popular opinion, "competition" doesn't by itself magically lower prices, at least not by enough. Both Anthem and Molina are leaving the ACA exchange (although Anthem is technically sticking around off-exchange), but there's over a dozen other carriers still duking it out.

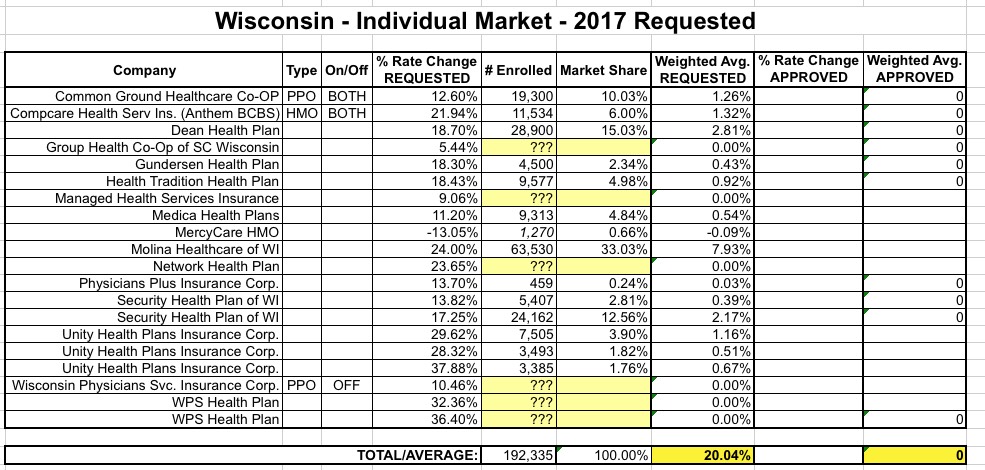

According to the 11 carriers I have enrollment numbers for, the statewide average rate increase being requested is around 20.8% assuming CSR payments are made; using the Kaiser Family Foundation estimates, that translates into roughly 32.4% assuming they aren't made. Unfortunately, I can't seem to dig up the enrollment data for four carriers: Aspirus, Compcare, Wisconsin Physician Service and WPS (I think the last two are actually subsidiaries fo the same company). Wisconsin's total individual market should be roughly 280,000 people, and when you add up all the numbers I have (including Anthem/Molina) it only comes to around 180,000, so there appear to be roughly 100,000 enrollees missing among those 4 carriers, or over 35%.

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

I originally estimated the requested average rate hike for Wisconsin indy market carriers back in August. I came up with a weighted average of around 20%...but this was questionable due to my not being able to come up with the actual enrollment figures for 4 of the 15 carriers in the state (note: several of these have more than one entry for different types of plans):

A couple of days ago, the Wisconsin Insurance Dept. announced the approved rate increases. Unfortunately, the articles about it don't provide hard numbers for either the rate change or enrollment figures for each carrier either, but they did provide the overall weighted average increase, which is really what I'm trying to calculate anyway, so there you go:

Arise Health Plan, a subsidiary of WPS Health Solutions, said Thursday that it will not sell health plans on the marketplaces set up through the Affordable Care Act next year, becoming the latest company to abandon the market.

Arise and WPS Health Insurance also will sell only high-deductible health plans for individuals and their families off the marketplace, and those plans will be available only in a limited number of counties.

...For now, the marketplace for Milwaukee County next year will have four companies offering health plans: Molina Healthcare; Network Health Plan, owned by Ascension Wisconsin and Froedtert Health; Common Ground Healthcare Cooperative; and Children’s Community Health Plan.

Waukesha County tentatively will have those companies as well as Anthem Blue Cross and Blue Shield in Wisconsin and Dean Health Plan.

...Arise Health Plan has a relatively small share of the market in southeastern Wisconsin.

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

Wisconsin's total individual market was around 260,000 people in 2014 and is likely up to around 300,000 today (not including grandfathered/transitional enrollees), with about 224,000 enrolled on ACA exchange policies as of March 2016, plus an unknown number off-exchange. That means that the table below is likely missing around 1/3 of the total ACA-compliant market.

A source who doesn't wish to be named attended the annual meeting of the Wisconsin Common Ground Co-Op the other day (Common Ground is one of the 11 Co-Ops which survived last year's Risk Corridor Massacre), and forwarded a few tidbits of info:

CG is open to considering outside investment funding now that CMS is allowing the Co-Ops to pursue it, but isn't scrambling to seek it out just yet. They did note that Wisconsin has a law applying to the Co-Op which requires that all board members use it for their own insurance (which makes total sense, actually). Since any outside investor would likely be on the board, they'd also have to utilize CG coverage.

I was also provided with an image of their overall financials for 2015 (see below). They didn't have much to say about this year since it's only May but seemed comfortable with how things are proceeding so far, and said their MLR (medical loss ratio) is "dropping" although from what to what I have no idea.

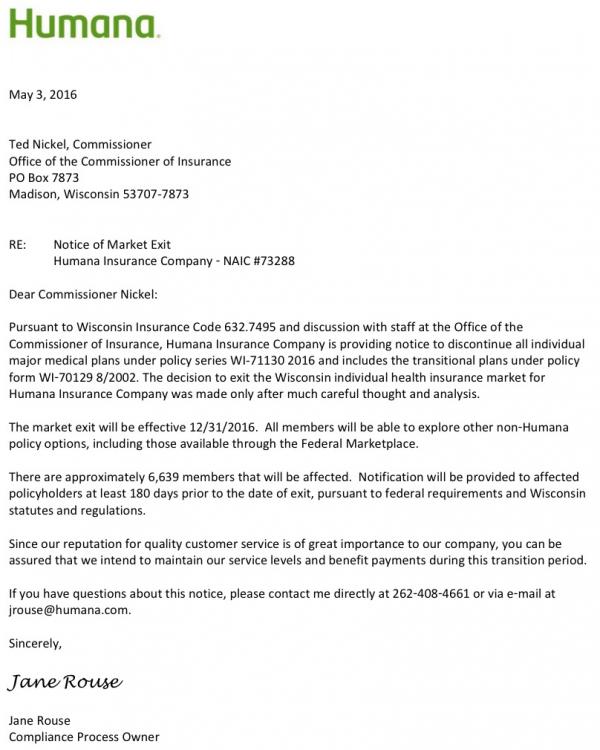

This is really just a summary of my last 4 posts. I've combed through the SERFF databases for every state which uses the system for rate filings, and while very few have the actual 2017 rate filing requests listed yet, at least 4 of them have official individual market exit letters submitted for 2017 from Jane Rouse, the Product Compliance Process Owner for Humana Insurance Co:

This list may grow as additional state filing data and/or press releases come out from Humana, but assuming these are the only 4 states Humana is bailing on, the news isn't quite as bad as it appears at first.

To be clear, I'm not saying this is a good development; when you combine it with the recent UnitedHealthcare Dropout Odometer it's more of a drip-drip-drip sort of thing. But it isn't disasterous for the exchanges either (at least not yet).

UPDATE: I've been informed by a reliable source that Humana is also dropping out of the individual market in Nevada next year, although I don't have any actual enrollment data there. Humana is not currently participating on the Nevada exchange, however, so any dropped enrollments would be OFF-exchange only. In fact, I'm pretty sure that the only individual market enrollees Humana has in Nevada are grandfathered policies anyway, so the numbers should be pretty nominal there.

If you're one of the ACA-created CO-OPs which isn't going out of business, I have to imagine that it's a tough enough job convincing current enrollees to stick with you right now, much less convincing new customers to give you a shot. I mean, look at it from the perspective of someone needing coverage; they're probably gonna be jumpy about signing up with one of the CO-OPs, fearing that they might be shut down just a few weeks/months later, right?

Well, for Common Ground, the Wisconsin CO-OP, which isn't going out of business and which is accepting both renewals as well as new customers right now, this can't be helping matters (from an email just sent to me today):

Copy of email sent by Common Ground Healthcare Co-op (Wisconsin)....

November 3, 2015

If you called the Marketplace and were told that our plans are not available for 2016, you were given INCORRECT information.

I've held off posting an estimate of the weighted average rate increase for the final state on my list, Wisconsin, until now because there's a major gap in the data which likely makes my estimate off by quite a bit.

However, given that open enrollment is coming up a week from today, "window shopping" on HealthCare.gov is (supposedly) going live at any minute and the fact that with 49 other states (+DC) already included, I finally decided to go ahead and post this, along with a major caveat warning.

As y ou can see from the table below, there are two issues here. The first is a minor one: I have no idea what the rate change request from the Common Ground CO-OP is, except that it's under 10%. I also don't know exactly what Common Ground's enrollment figure is, other than "between 30,000-40,000" according to this article from February.