CMS approved a postpartum coverage extension state plan amendment (SPA) for Wyoming to extend postpartum coverage for a full year for individuals enrolled in Medicaid. The opportunity to extend postpartum coverage was made possible under the American Rescue Plan and made permanent in the Consolidated Appropriations Act, 2023. Wyoming’s approval marks 37 states, D.C., and the U.S. Virgin Islands that have extended postpartum Medicaid coverage to a full year. This approval supports the CMS Maternity Care Action Planand Biden-Harris Maternal Health Blueprint.

A decade ago, when conservatives were attacking President Barack Obama’s Affordable Care Act as government encroachment in health care, they worked to amend state constitutions around the country to affirm a broad right for people to control their own medical decisions.

“Each competent adult shall have the right to make his or her own health care decisions,” reads section 38(a) of the Wyoming constitution’s Declaration of Rights, under the header “Right of healthcare access.” The provision was placed on Wyoming’s ballot by state lawmakers and approved by voters in 2012; voters saw ballot language that described the measure as preserving this right “from undue governmental infringement.”

Now these anti-ACA provisions—and their broad affirmations of a right to decide—have turned into an unlikely weapon in progressives’ fight against restrictions on abortion.

Medicaid expansion will be up for debate once again when the Wyoming Legislature convenes for its 67th session in January.

The legislature’s Joint Revenue Committee voted to advance the Medical Treatment Opportunity Act to the legislative session during a meeting this month.

It’s the same bill the legislature considered during the 2022 session, state staffers said.

The proposed legislation would allow Medicaid expansion to occur in Wyoming as long as the federal contribution to the program remains at 90 percent or higher.

The smallest of these, which is also the smallest state in the country, is Wyoming, which has had a long & storied history when it comes to Medicaid expansion fakeouts. The "Equality State" legislature has considered expanding Medicaid to the roughly 19,000 residents who would become newly eligible for the program eight times since the ACA was signed into law in 2010, only to see approval of it fail at one stage or another every time.

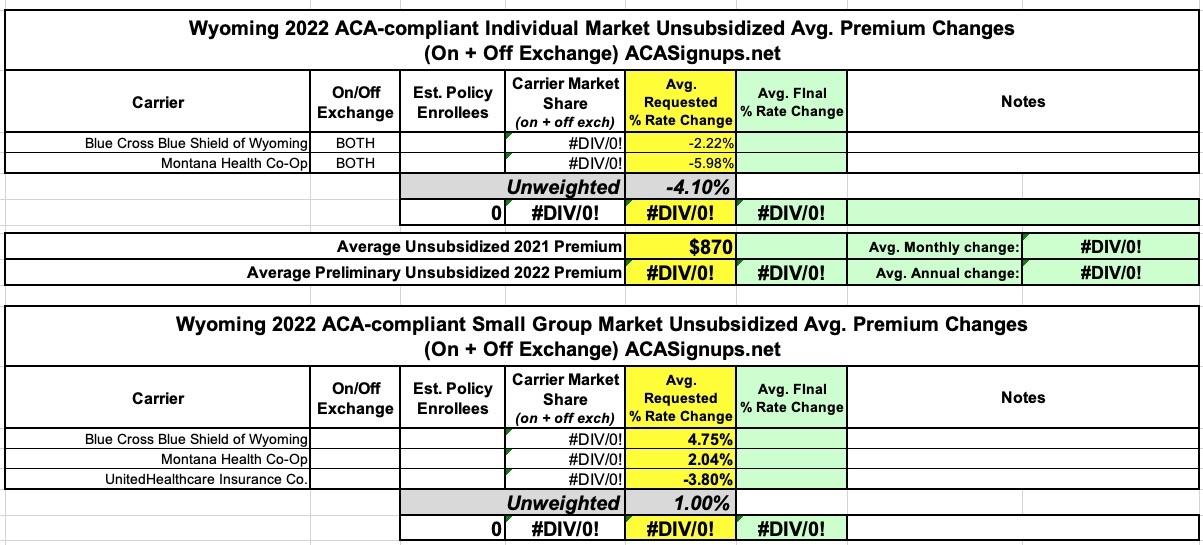

Wyoming is the smallest state and only has two carriers offering individual market policies (and just three offering small group plans). This makes it pretty simple for me.

Unfortunately, neither their insurance department website nor their SERFF filings give any indication of the enrollment numbers for any of the carriers. Fortunately, the federal rate review website does list enrollment for Blue Cross Blue Shield of Wyoming...which also has something like 95% of the individual market share in the state. By estimating the enrollment for the 2nd carrier (Montana Health Co-Op), I should be pretty close to the weighted average...a pretty ugly 18.5% average rate hike. Ouch.

It's no better on the small group side, although I don't have the actual enrollment for the other two carriers; the unweighted average is "only" an 11.9% increase, but it's over 20% for BCBSWY enrollees.

As I noted last night, thanks to the federal Rate Review website finally being updated to include the final, approved 2022 rates for both the individual and small group markets in all 50 states (+DC), I've been able to fill in the missing data for my annual ACA Rate Change Project.

As I note there, the overall weighted average looks like it'll be roughly +3.5% nationally.

Normally I write up a separate entry for both the preliminary and approved rate changes in each individual state, but it seems like overkill to create 14 separate entries at once. Besides, in many of these states there's been few if any changes between the preliminary and approved rate changes.

Wyoming is the smallest state and only has two carriers offering individual market policies (and just three offering small group plans). This makes it pretty simple for me.

Unfortunately, neither their insurance department website nor their SERFF filings give any indication of the enrollment numbers for any of the carriers, making it impossible to calculate a weighted average for either market. Then again, assuming a roughly even market share split, the unweighted averages should be pretty close: -4.1% individual market, +1.0% small group.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In most states I've been able to get more recent enrollment data from state websites and other sources. Unfortunately, Wyoming isn't among them, though I've estimated January enrollment based on CMS's just-released Monthly Medicaid & Chip report (which use a slightly different methodology than the MBES reports).

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

Medicaid expansion will not happen in Wyoming this year.

The state’s Senate Labor, Health and Social Services Committee killed a bill Wednesday morning to expand the federal insurance program, which would have insured an estimated 25,000 additional Wyomingites.

Lawmakers have defeated similar proposals for nearly a decade. Advocates hoped this year might be different. Many House Republicans voiced a change of heart after the COVID-19 pandemic and the decline of fossil fuels rocked the state’s economy, leaving many without health coverage. This session was the first in which a bill to expand the program passed a legislative chamber.

{kind=link}