The ACA's language didn't account for the possibility that some states might not expand Medicaid, which is why the lower-end range of exchange plan subsidy eligibility starts off at 100% FPL...

Unfortunately, those earning less than 100% FPL are still stuck without any viable options besides either "going bare" and praying they don't get sick or injured or possibly buying a junk plan of some sort. According to the Kaiser Family Foundation, there's around 2.2 million Americans still caught in the "Medicaid Gap", where they don't qualify for Medicaid but don't earn enough to be eligible for subsidized ACA exchange policies (Kaiser estimates another 1.8 million uninsured adults in these states in the 100 - 138% "overlap" cateogory, plus around 356,000 who are eligible for Medicaid but still haven't enrolled for one reason or another).

NOTE: This is an updated version of a post from a couple of months ago. Since then, there's been a MASSIVELY important development: The passage of the American Rescue Plan, which includes a dramatic upgrade in ACA subsidies for not only the millions of people already receiving them, but for millions more who didn't previously qualify for financial assistance.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

Republican lawmakers blocked Medicaid expansion funding from reaching the Missouri House floor on Wednesday, posing a setback for the voter-approved plan to increase eligibility for the state health care program.

The House Budget Committee voted along party lines not to pass a bill allowing Missouri to spend $130 million of state funds and $1.6 billion in federal money to pay for the program’s expansion. Under the Affordable Care Act, the federal government picks up 90% of the tab on expanding Medicaid.

The expanded eligibility would allow estimated 230,000 additional low-income Missourians to be covered. It is set to go into effect in July after voters approved a ballot question last August with a 53% majority.

The American Rescue Plan does plenty to make private ACA-compliant health insurance dramatically more affordable for everyone earning more than 100% of the Federal Poverty Level. For those below 100% FPL, however, it takes an indirect approach. As I wrote a few weeks ago:

One possible "solution" would have been to simply remove the lower-bound income cut-off point for ACA exchange subsidy eligibility (that is, to lower the threshold from 100% FPL to 0%)...However, this would create two new problems: First, Medicaid is far more comprehensive than nearly all ACA plans...Secondly, if the lower-end subsidy cut-off were removed, it's almost certain that quite a few states which have already expanded the program would reverse themselves and allow Medicaid expansion to expire, in order to save the 10% portion of the cost that they have to pay.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

If you have a fairly healthy year, you really could go the entire year without paying a dime in healthcare costs while still taking advantage of many of these free services, and also having the peace of mind that in a worst-case scenario, at least you wouldn't go bankrupt. Not perfect, but a lot better than going bare especially since you wouldn't pay a dime in premiums.

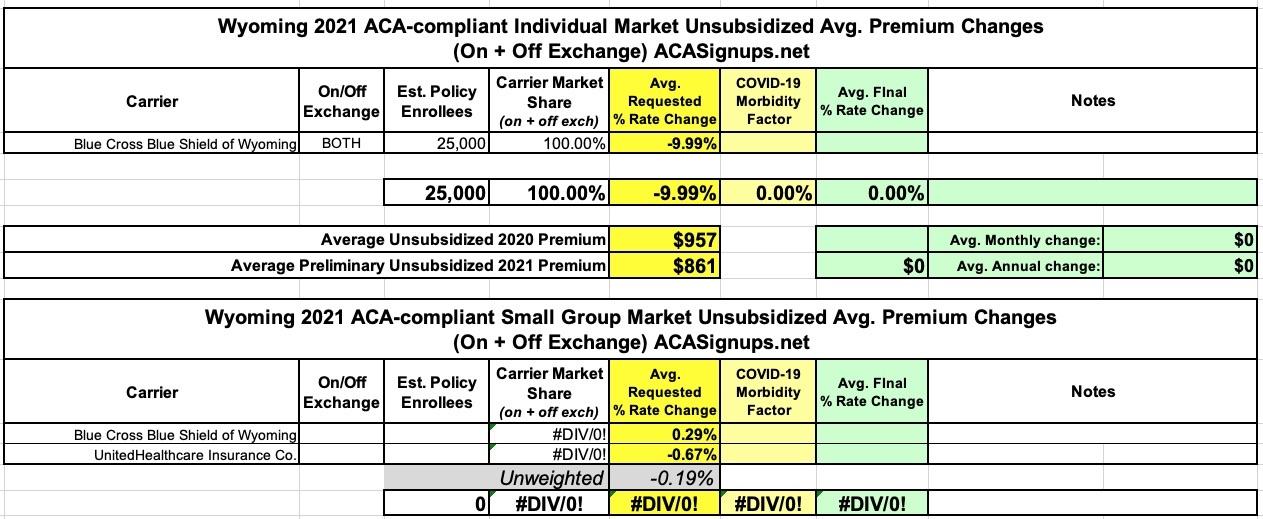

Not much to this one: Wyoming has just a single carrier selling ACA-compliant individual market policies to their 577,000 residents, Blue Cross Blue Shield...which, after raising rates 1.6% for 2020 is now reducing them by a solid 10% on average for 2021. The ~25,000 enrollment figure is an estimate.

For the small group market there are two carriers: BCBSWY and UnitedHealthcare, asking for an unweighted average rate reduction of 0.2% (I don't have a clue how many enrollees either one has).

Louisiana's 2020 Presidential primary was scheduled for April 4th, but the other day Democratic Governor John Bel Edwards and Republican Secretary of State Kyle Ardoin agreed to reschedule it for June 20th...which is actually later than the last previously-scheduled primary in the U.S. Virgin Islands on June 6th:

The presidential primary elections in Louisiana slated for April will be delayed by two months, the latest in a series of dramatic steps government leaders have taken to slow the spread of the new coronavirus.

Secretary of State Kyle Ardoin, Republican, and Gov. John Bel Edwards, a Democrat, both said Friday they would use a provision of state law that allows them to move any election in an emergency situation to delay the primary.

The presidential primary elections, initially scheduled for April 4th, will now be held June 20th. Ardoin said in a press conference he does not know of any other states that have moved elections because of the new coronavirus, or COVID-19.

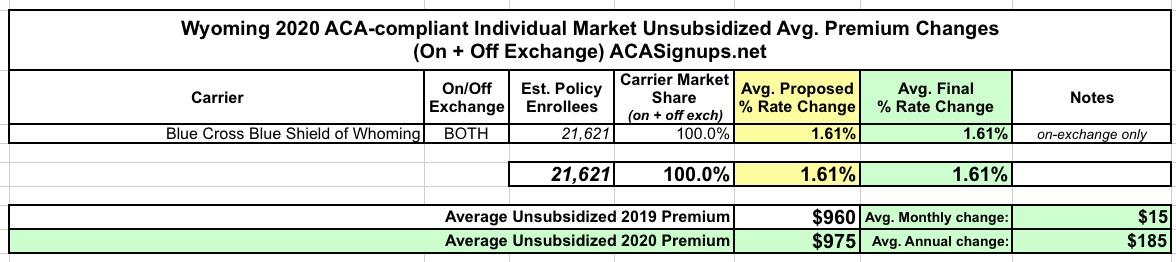

Not much to this one: Wyoming has just a single carrier selling ACA-compliant individual market policies to their 577,000 residents, Blue Cross Blue Shield...which is raising rates 1.6% on average for 2020. No change from their requested increase a few months earlier.

Former Wyoming Blackjewel LLC coal miners who have been out of work since July 1 and without health insurance since their group health plan was canceled Aug. 31 can sign up for the federal health insurance marketplace retroactively to Sept. 1.

The Wyoming Department of Insurance has successfully lobbied the Centers for Medicare and Medicaid Services (CMS) to make an “exceptional circumstances” special enrollment period through Oct. 30, said Denise Burke, an attorney with the state Department of Insurance.

The exception allows former Blackjewel coal miners an option to buy health insurance off the marketplace and made it retroactively effective to Sept. 1, which means workers and family members with ongoing health issues can continue treatment as if they never lost insurance.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions: