New Mexico's final/approved 2022 premium rate changes are now live, though the searchable database seems to be having some technical layout glitches. For some reason there's a good 5-6 entries for each carrier instead of just 2 (one for the individual market, one for small group plans); I think this is because New Mexico requires separate filings for on- and off-exchange policies, although there seem to be duplicates even then.

In any event, of the 30+ states I've written up so far, New Mexico has by far the highest average unsubsidized rate increases, at 15.5%. Most of this is due to Molina Healthcare's shocking 25.6% increase, which seems to have been approved as is. True Health is also asking for double-digit increases on the individual market.

The Small Group market in the Land of Enchantment is also in the double digits, at +11.5% on average. Presbyterian not only has two small group entries, they seem to have dramatically different enrollment numbers for each; I'm not sure what to make of that.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In some states I've been able to get more recent enrollment data from state websites and other sources.

Today I'm presenting New Mexico.

For enrollment data from January 2021 on, I'm relying on adjusted estimates based on raw data from the New Mexico Dept. of Health.

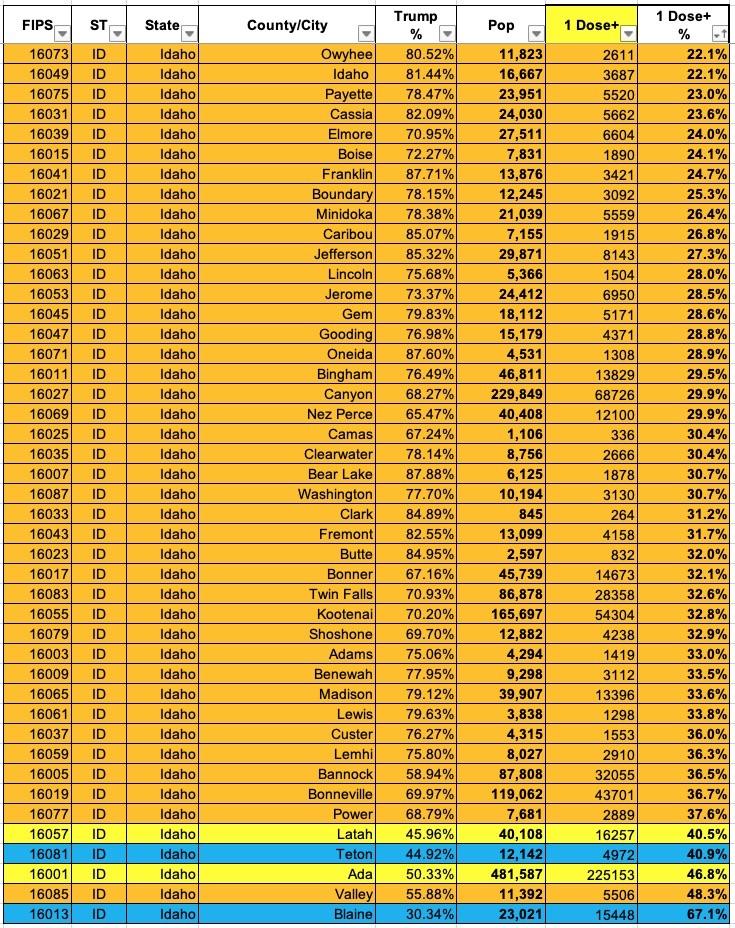

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

WARNING: The CDC lists ~199,000 New Mexico residents (a whopping 25% of the total fully vaccinated) whose county of residence is unknown. This could easily skew the actual results below one way or the other.

NOTE: This is an updated version of a post from a couple of months ago. Since then, there's been a MASSIVELY important development: The passage of the American Rescue Plan, which includes a dramatic upgrade in ACA subsidies for not only the millions of people already receiving them, but for millions more who didn't previously qualify for financial assistance.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

New Mexico would raise a state health-insurance tax and dedicate the new revenue to programs intended to make health care more affordable under a proposal that passed the state House on Sunday.

Rep. Deborah Armstrong, D-Albuquerque, described the legislation as an unusual opportunity to generate more revenue for health care without increasing the total amount consumers now pay.

The increased state tax would partially replace a federal tax that’s being repealed, she said, meaning health insurance carriers would actually be charged less in taxes than they are now, even after the state increase.

The legislation, House Bill 278, would raise about $125 million in annual revenue when fully phased in — the bulk of it dedicated to a new fund for health care affordability, according to legislative analysts.

New Mexico Superintendent of Insurance Announces Premium Decreases for 2021

Santa Fe, NM –New Mexico Superintendent of Insurance Russell Toal announced today that health insurance premiums will decrease significantly for individuals and families purchasing their own coverage through beWellnm (New Mexico’s Health Insurance Exchange). Average plan prices dropped in the Bronze, Silver, and Gold plan categories across the state. Silver plans, the most common plan purchased on the individual Exchange, will decrease between 8.1 and 13.5 percent on average. Small businesses will experience a 6.7 percent average premium decrease on beWellnm.

The Office of Superintendent of Insurance (OSI) reviews health insurance filings annually to determine whether rates are reasonable and fair.

“After a rigorous review of health insurance filings, our office is pleased to report that premiums are going down in 2021,” said Superintendent Toal. “Not only are rates decreasing, but New Mexico will have more health plans competing in the marketplace than ever before”

New Mexico is the latest state to post their preliminary 2021 rate change filings for both the individual and small group markets. There's several key things to note here:

As I explained, the HIT is one of a several taxes/fees which were originally included in the Affordable Care Act which have either never actaully been enforced or whcih have only been enforced sporadically, and which have now been completely eliminated going forward.

The impact of repealing these taxes on the federal deficit/federal debt is obviously not good...this will collectively increase the already-runaway national debt by several hundred billion dollars over the next decade. That's a whole separate discussion.

In the short term, however, this raises a fascinating one-time opportunity for states to step in and generate some much-needed revenue to be used to reduce healthcare costs for tens of thousands of their residents.

A couple of weeks ago, BeWell NM, the name of the New Mexico ACA health exchange, held their latest board meeting. There's two key things to keep in mind about New Mexico:

First, they've been officially operating as a state-based exchange while "piggybacking" off of HealthCare.Gov since the very first Open Enrollment Period in 2013-2014...but they announced over a year ago that they're following Nevada's (and Idaho's) lead in splitting off onto their own full exchange, starting in 2021.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

{kind=link}