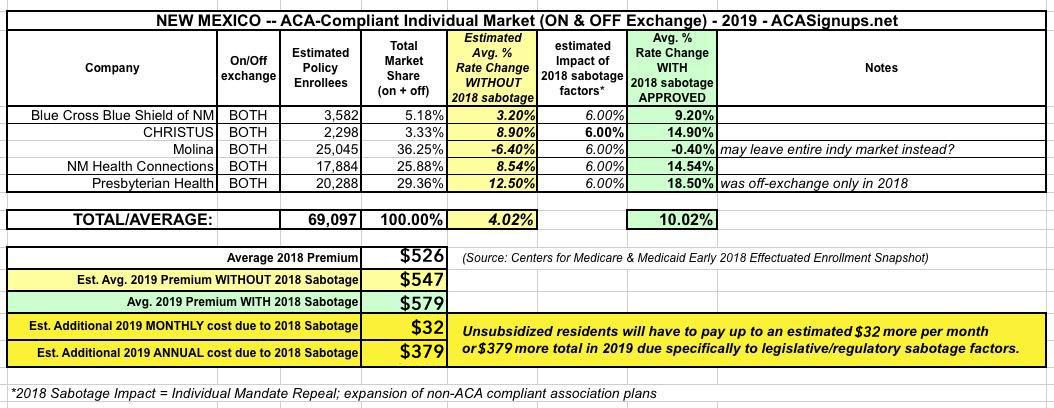

New Mexico was one of the earlier states to post their initial, requested 2019 ACA individual market premium hikes back in June. At the time, the five carriers asked for rate increases ranging from a slight drop (-0.4% for Molina) to as high as an 18.5% increase for Presbyterian Health, which is currently only offering off-exchange policies this year. Based on their preliminary filings, New Mexico was looking at a weighted average increase of around 10.0% next year, which would have been more like 4% if not for this years sabotage efforts by Trump and the GOP (mandate repeal & expansion of #ShortAssPlans):

Rate filings were due in New Mexico by June 10, 2018, for insurers that wish to offer individual market plans in 2019. Insurers that offer on-exchange coverage have been instructed by the New Mexico Office of the Superintendent of Insurance (NMOSI) to add the cost of cost-sharing reductions (CSR) only to on-exchange silver plans and the identical versions of those plans offered off-exchange (different silver plans offered only off-exchange will not have the cost of CSR added to their premiums).

Insurers That Filed Wrong Rates Told By CMS They Can't Sell Plans Through Mid-November

An issuer whose final CMS-approved rates don’t account for the loss of cost-sharing reduction payments is being told by the agency that they won’t be able to sell plans until healthcare.gov data is refreshed– even though this would mean the carriers are even more crunched for time to sell their plans during the shortened open enrollment period.

UPDATE: It looks like this issue may be limited to a single carrier in New Mexico; I've changed the headline and graphic accordingly...but it might be an issue in other states as well; if so I may have to change it back again...

Insurers That Filed Wrong Rates Told By CMS They Can't Sell Plans Through Mid-November

An issuer whose final CMS-approved rates don’t account for the loss of cost-sharing reduction payments is being told by the agency that they won’t be able to sell plans until healthcare.gov data is refreshed– even though this would mean the carriers are even more crunched for time to sell their plans during the shortened open enrollment period.

Back in July, I had originally estimated the requested rate increases for New Mexico to average roughly 24.2% with partial Trump Administration sabotage or 37.2% with full sabotage (no CSR payments, full mandate enforcement threat). However, figuring out NM's approved rate hikes is proving to be frustrating.

On the one hand, they have a handy database lookup tool right there on the NM Insurance Dept. website, and they even have the actual premium amount listings for every plan from every carrier in every rating area available. Unfortunately, the premium listings don't give a year over year comparison (or an average percent increase), and the database tool seems not to have been fully updated as of this writing, making it kind of useless. I have some info for a couple of the individual carriers but even that's a bit confusing.

New Mexico Health Connections, the nonprofit co-op insurance company formed under the Affordable Care Act, is selling its small group and commercial business to a for-profit company under a restructuring plan that will create a new insurance company that will be able to go after business the struggling nonprofit couldn’t.

...The Washington, D.C.-based Evolent will acquire NMHC’s 22,000 commercial members. NMHC will continue to exist with a few employees and presumably continue to sell individual policies on the New Mexico Health Insurance Exchange. NMHC has 10,000 individual members through the insurance exchange.

...Hickey told ABQ Free Press that the deal will allow the new firm to go after business that NMHC couldn’t, things like Medicare Advantage, federal employees and, eventually, Medicaid. It also gives the new firm capital reserves that NMHC didn’t have, he added.

A week ago, Vox's Sarah Kliff reported that the Trump Administration was slashing the 2018 Open Enrollment Period advertising budget by 90% and the navigator/outreach grant budget by nearly 40%. As I noted at the time, the potential negative impact of these moves on enrollment numbers this fall--coming on top of the period being slashed in half, the CSR reimbursement and mandate enforcement sabotage efforts of the Trump/Price HHS Dept. and the general confusion and uncertainty being felt by the GOP spending the past 7 months desperately attempting to repeal the ACA altogether could be significant. In states utilizing the federal exchange (HealthCare.Gov), 2017 enrollment was running neck & neck with 2016 right up until the critical final week...which played out under the Trump Administration, which killed off the final ad/marketing blitz.

Result? A 5.3% total enrollment drop (or 4.7% if you don't include Louisiana, which expanded Medicaid halfway through the year) via HC.gov, while the 12 state-based exchanges--which run their own marketing/advertising budgets--saw a 1.8% increase in total enrollment year over year.

The database at the link above doesn't include the enrollee market share numbers; for that I had to dig up the actual filings at the SERFF database. Blue Cross Blue Shield and Presbyterian seem to be assuming no significant TrumpTax next year (which makes sense, since both will be off-exchange only, thus not subject to CSR payment concerns). Molina's filing is kind of odd--they seem to assume that CSR payments will be made...but that the individual mandate won't be enforced, which seems rather backwards to me (most TrumpTax filings assume neither will be enforced, or that the mandate will but CSR payments won't).

New Mexico is one of five states (also including Nevada, Oregon, Hawaii and Kentucky) which technically operate their own state-based ACA exchange, but utilize HealthCare.Gov as their website enrollment platform. As such, their enrollment numbers are usually only released along with the other three dozen states on the federal exchange.

However, once in awhile they post the enrollment numbers themselves; today is such a day:

@charles_gabaNMHIX: 52,006 total signups - almost as much as last year. Still anticipating a surge as NMHIX continues ads and outreach.

The breakout here is 36,579 renewals + 15,427 new enrollees, or a 70/30 split.

Last year, New Mexico's total came in at 54,865 QHP selections, so they've hit 95% of that so far.

My original target for New Mexico for this year was 60,000, though I've knocked this down to 57,000 more recently. They're at around 91% of that so far, with less than a week to go. They'll have to add another 5,000 people in the final surge, which seems unlikely, but who knows?

In New Mexico, assuming 57,000 people enroll in private exchange policies by the end of January, I estimate around 25,000 of them would be forced off of their private policy upon an immediate-effect full ACA repeal, plus another 260,000 enrolled in the ACA Medicaid expansion program, for a total of 285,000 residents kicked to the curb.

As for the individual market, my standard methodology applies: