They break out the filings not between Individual and small group markets or on- vs. off-exchange policies, but between rate increases over and under 10%. Normally that would be fine, but they also have multiple listings within each market for several carriers; HMO Louisiana, in fact, has 11 entries, each for a different product line, making it tedious and difficult to piece together the weighted average rate change and current enrollment for the carrier as a whole.

In addition, it looks like the state regulators have given final approved rate changes for 2022 in some cases but not others...even within the same carrier and market.

As a result, my weighted averages below may be off somewhat.

With that in mind, it looks like Louisiana's individual market is looking at final average rate hikes of 4.75%, while their small group market carriers are seeking preliminary increases of around 6.9%.

Well, this was inevitable: I got so far behind on my annual ACA rate filing project that the final/approved rates have started to be released before I even get around to some of the preliminary/requested rate filings.

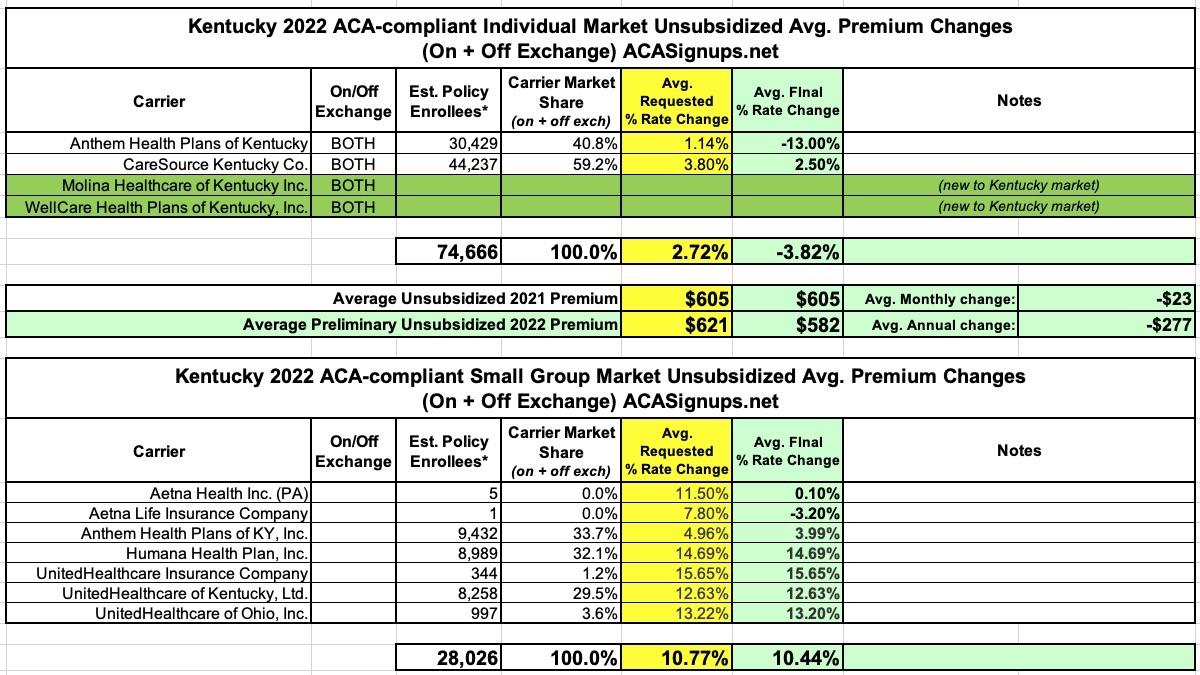

The Kentucky Insurance Dept. has posted both the requested and approved 2022 rate filings for the individual and small group markets, and in addition to drastically slashing the average premiums for Anthem's individual market offerings and Aetna's small group offerings, there's also two new entrants into Kentucky's individual market: Molina and WellCare.

Overall, individual rates are dropping by around 3.8% on average (the carriers had requested a 2.7% increase), while small group market plans are increasing by 10.4% on average (very close to the 10.7% average request).

Back in late July, I posted an analysis which looked at the COVID-19 vaccination rate across all 3,144 U.S. counties, parishes & boroughs by two additional criteria: Population Density and Urban/Rural Status.

As I noted at the time, it's reasonable to assume there might be a strong correlation by these criteria, since it's presumably a lot more difficult to get vaccinated if you live out in the middle of the boonies where the nearest hospital, clinic or pharmacy is 50 miles away or whatever...not to mention that if you're the only one for miles around, you might be less likely to see getting vaccinated as a high-priority task regardless of your ideology.

Therefore, the reasoning goes, instead of looking at the partisan lean of each county, it would make much more sense to see how much correlation there is based on population density or whether it's a more urban or rural region, right?

Methodology reminders, including some important updates:

I go by FULLY vaccinated residents only (defined as 2 doses of the Pfizer or Moderna vaccine or one dose of the Johnson & Johnson vaccine).

I base my percentages on the total population, as opposed to adults only or those over 11 years old.

For most states + DC I use the daily data from the Centers for Disease Control, but there are some where the CDC is either missing county-level data entirely or where the CDC data is less than 90% complete at the county level. Therefore:

For California, I'm using the CDC data for most counties and the state health dept. dashboard data for the 8 small counties which the CDC isn't allowed to post data for.

The 5 major U.S. territories don't vote for President in the general election, preventing me from displaying them in the main graph, but I have them listed down the right side.

An estimated 138,000 Californians face significantly higher health insurance premiums when their federal COBRA subsidies come to an end on Sept. 30.

Covered California opened a special-enrollment period to give eligible COBRA recipients an opportunity to switch their coverage and potentially save hundreds of dollars a month on their health insurance.

Many of those consumers will be able to stay with their same brand-name insurance company when they switch to Covered California.

People who sign up by Sept. 30 will have their coverage start on Oct. 1.

SACRAMENTO, Calif. — Covered California announced a special-enrollment period for Californians who will soon be losing the federal financial help that is allowing them to continue receiving health insurance through the Consolidated Omnibus Budget Reconciliation Act, better known as COBRA. Under one provision of the American Rescue Plan, Californians have been eligible for financial help that pays 100 percent of their COBRA premiums from April 1 through Sept. 30.

Aside from the massive public health fallout, this fact has all sorts of poltiical implications as well, of course. Most of those involve pundits speculating about "the blame game" and so on; will voters in states like Florida and Texas blame their governors for doing everything possible to stymie reasonable pandemic safety measures such as mask mandates, or will they blame the Biden Administration for...I don't know, not tying people to a chair and manually forcing the COVID vaccine into their arms?

For weeks now, however, people have been asking me an even more basic, crass question about the impact of political tribalism on the 2022 midterm election:

For the past couple of months now, most of my COVID scatter-plot charts...whether measuring vaccination rates, new case rates or new death rates...have been based primarily on partisan lean. That is, at both the state and county levels, I've been using the percent of the 2020 Presidential vote won by Donald Trump as the basis for comparison.

I've also looked at vaccination rates by other criteria, of course: Population density, urban vs. rural status, education level and median household income levels...but none of these have had nearly as high a correlation as sheer partisan lean has (although I haven't checked any of those in over a month; perhaps the situation has changed by now).

A couple of years ago, Washington became the first state to implement their own "Public Option" ACA healthcare plan...sort of. The actual version of the PO which was implemented ended up being considerably less impressive than the original vision, but hey, it was a start.

I've gotten a lot of attention for my COVID "scatter plot bubble graphs" over the summer, laying out the COVID vaccinationandcase/death rates across every county nationally (well, mostly; Nebraska has stopped posting county-level data entirely, and Florida has only been posting county-level case data, not deaths, since June).

Data visualization is a tricky thing, though; sometimes line graphs are the way to go (that's what I did last year); other times scatter plots are more appropriate. But some people don't "get" either of these, so today let's look at some bar graphs.

Record Numbers of Washingtonians Sign Up for Health Care Coverage During 2021 Special Enrollment Period

LATEST DATA SHOWS IMPACT OF AMERICAN RESCUE PLAN ACT SAVINGS. NEARLY HALF OF ALL CUSTOMERS PAY LESS THAN $100 PER MONTH.

Washington Health Benefit Exchange (Exchange) announced on Tuesday more than 57,000 Washingtonians signed up for health care coverage between February 15 and August 15 on the state’s insurance marketplace, Washington Healthplanfinder. The Exchange opened a Special Enrollment Period in February in response to the COVID-19 Public Health Emergency. This allowed any individual in Washington the opportunity to apply for coverage or compare and upgrade their existing insurance.