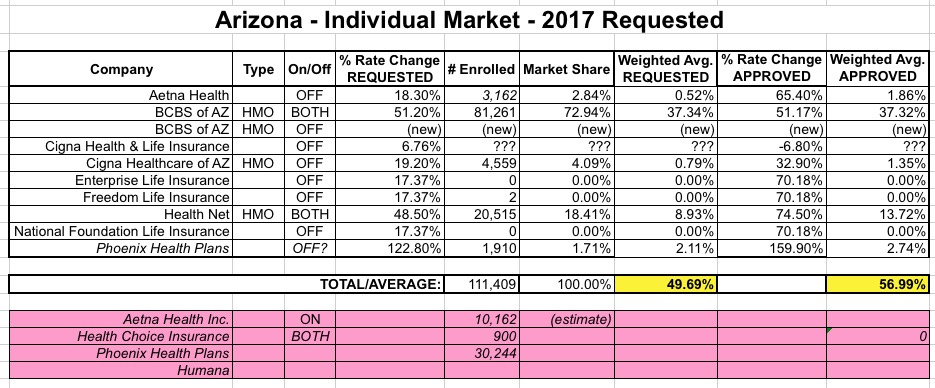

The ACA exchange in Arizona has hadsome prettydramaticturns over the past month or so. When the dust settled, every county in the state will still have at least one carrier offering plans on the exchange...although only one. Anyway, today the AZ DOI joined Pennsylvania and Michigan in releasing their final approved rate hikes for both the individual and small group markets:

Right on top of Pennsylvania, the Michigan Dept. of Insurance has issued their final approvals for 2017 individual and small group market rate increases. As has been pretty typical this year, the final approved rates aren't all that different from what was requested; a little nip/tuck here and there, and the 17.2% average requested has been slightly trimmed to 16.7% approved for the indy market. Meanwhile, the small group average is barely noticeable: 2.6% requested, 2.5% approved. Unlike most states, the MI DOI has already done most of the heavy lifting for me, so I don't even have to use my own spreadsheet to calculate the weighted average.

(thanks to commenters "M E" and "joe" for the heads up).

The state Dept. of Insurance has released their approved rate hikes for 2017, and it's bad news in two different ways. First, the overall full-price average rate increase looks like it'll be roughly 32.5%...over 8 points higher than the original rates requested by the carriers. Secondly, even with those higher increases, two more indy market carriers (Keystone Health Plan and Geisinger Quality Options) are pulling off the exchange, although both will continue to offer off-exchange plans.

It's important to be careful with the full carrier names here, because they often operate under several different very similar ones (Keystone Health Plans vs. Keystone Health Plan East, for instance, which is not pulling off the exchange).

When I originally calculated the average requested rate hike for New Hampshire, I came up with a weighted estimate of around 13.1%. A month later, the average dropped a few points...but not for a good reason: One of the remaining ACA-created Co-Ops, Community Health Options, decided to pull out of New Hampshire (they started out as a Maine-only operation, expaneded into nearby NH for the 2nd and 3rd year, but are pulling back to Maine-only again). Since CHO would otherwise have been requesting a more than 40% increase, them dropping out actually lowered the average increase for everyone else. This obviously illustrates a major caveat with my "average rate increase" methodology: It only applies to those who are able to renew their existing plans. The moment a carrier pulls out of parts/all of a state, or drops PPOs (while keeping HMOs), etc, I have to remove a portion of the existing enrollees from the equation completely.

For 2017, only Blue Cross Blue Shield of Alabama will participate in the exchange. In August 2016, the carrier filed rate increases for 2017 that average 36.1 percent (with a range from 20.6 percent to 38.3 percent). This was a revised rate filing, and was slightly lower than the average rate increase proposal of 39.3 percent that the carrier initially filed in June.

The Alabama Department of Insurance approved the 36.1 percent average rate increase in October 2016, and the new rates will take effect in January 2017. AL.com reports that pre-subsidy rates for Bronze plans will increase between 20 percent and 23 percent, while Silver and Gold plans will increase in price between 32 percent and 38 percent.

Blue Cross Blue Shield of North Carolina originally requested an 18.8% rate hike back in June, but after the Aetna pullout, they revised their request upwards to 24.3%. Cigna, which is expanding onto the ACA exchange next year, followed suit by bumping up their request from 7% to 15%.

I haven't seen any formal announcement from the NC Dept. of Insurance yet, but BCBSNC just posted the following blog entry announcing their 2017 rates...and it certainly looks like the 24.3% request was indeed granted as is:

Blue Cross and Blue Shield of North Carolina customers purchasing ACA plans on the individual market will see an average increase of 24.3 percent in their premiums for 2017, compared to this year’s rates. That’s higher than our original rate filing back in May (an 18.8 percent increase).

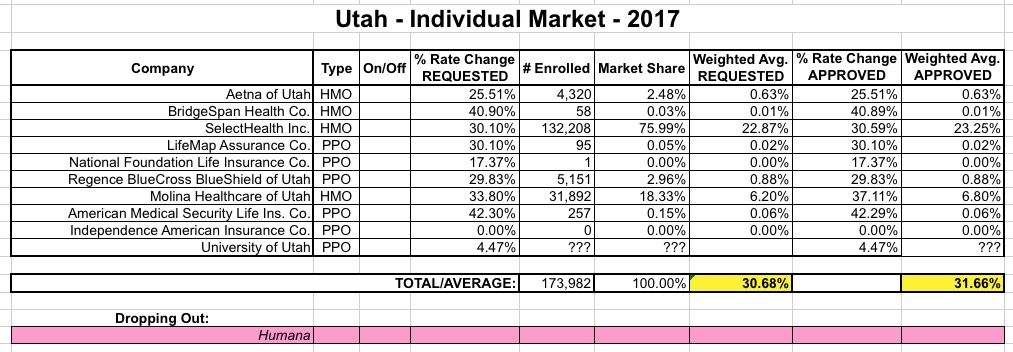

When I plugged the numbers in for Utah way back in June, I came up with a weighted average request of around 30.7%.

Louise Norris gave me a heads up that the approved rates were in for UT, and sure enough she's correct. Not a whole lot to report, however; most of the requests were approved as is, with only minor modifications; the approved average is slightly higher:

Regular readers may be a bit confused here, as Oregon's insurance dept. had already approved 2017 rates back in early August, for a statewide average of around 23.8%.

But when four carriers (Atrio, BridgeSpan, Providence, and — off-exchange — Regence) agreed in August to cover a broader service area than they had originally intended for 2017, state regulators also allowed them to further increase their premiums due to the increased risk they would be shouldering. Final approved average rate increases for Oregon’s exchange carriers are as follows:

Atrio Health Plans: 29 percent (up from the originally-approved 20.8 percent).

BridgeSpan: 23 percent (up from the originally-approved 18.9 percent).

Kaiser Permanente: 14.5 percent (range is from 10.9 to 22 percent).

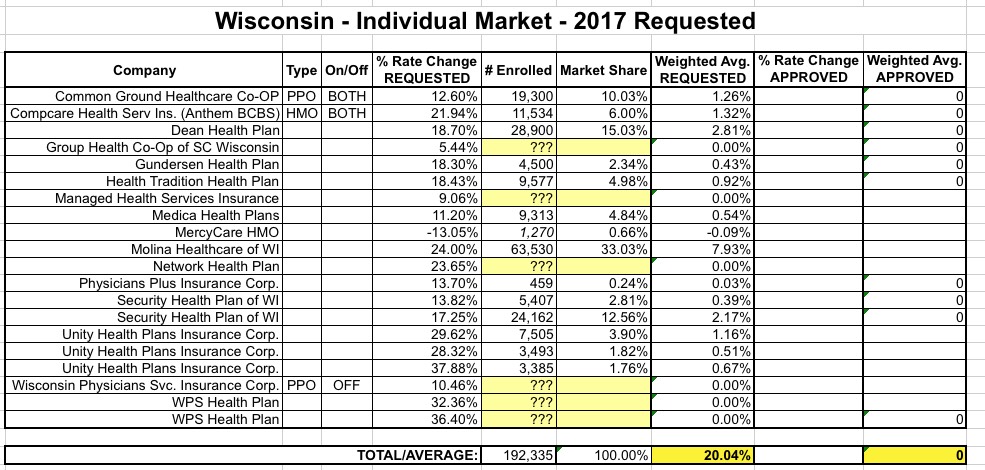

I originally estimated the requested average rate hike for Wisconsin indy market carriers back in August. I came up with a weighted average of around 20%...but this was questionable due to my not being able to come up with the actual enrollment figures for 4 of the 15 carriers in the state (note: several of these have more than one entry for different types of plans):

A couple of days ago, the Wisconsin Insurance Dept. announced the approved rate increases. Unfortunately, the articles about it don't provide hard numbers for either the rate change or enrollment figures for each carrier either, but they did provide the overall weighted average increase, which is really what I'm trying to calculate anyway, so there you go:

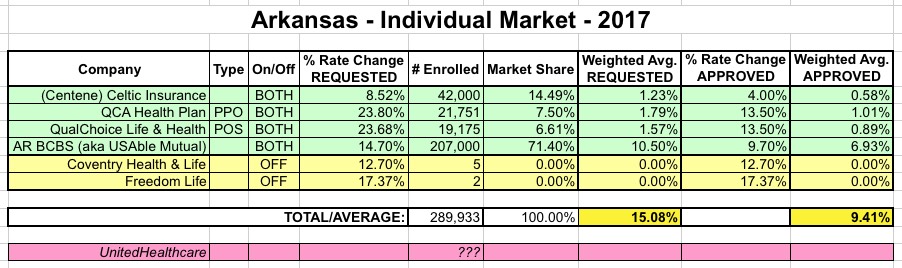

This is a minor update, but with all the bad rate hike news this year, I'll take any good news I can get. A couple of weeks ago, the Arkansas Insurance Dept. approved rate hikes for the 4 carriers participating in the ACA exchange next year, including significant reductions for all of them:

In mid-August, all of the carriers that offer plans in the Arkansas exchange proposed new rate increases for 2017, all of which were lower than their initially filed rates. Rate increases were then reduced even further for QualChoice and QCA: