New Hampshire: Avg. 2017 rate hike request revised down to 11.8% (but it's not good news)

Mon, 09/05/2016 - 12:06pm

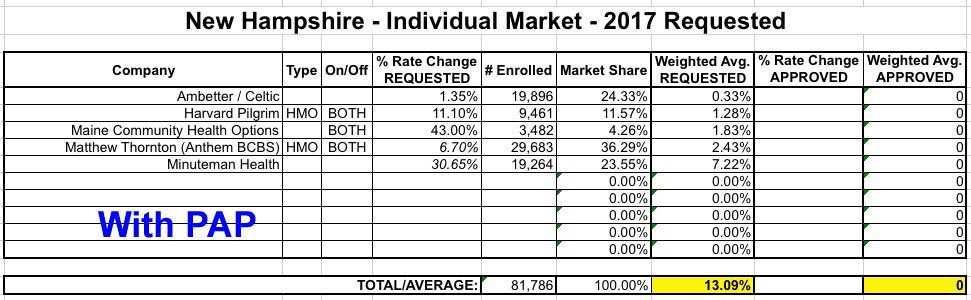

Last month I estimated that the weighted average rate hike requested by New Hampshire carriers for the individual market was around 13.1% when you include the Premium Assistance (PAP) enrollees:

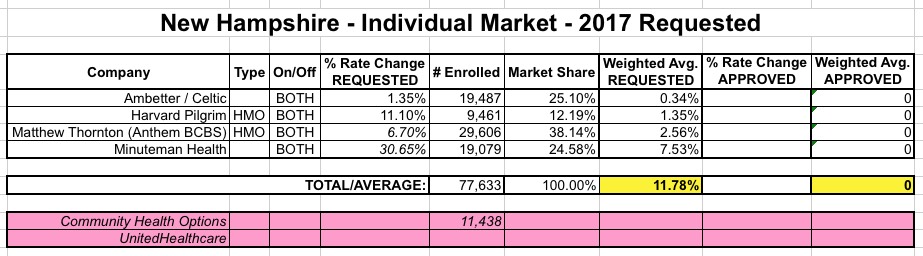

Today, I'm revising this estimate down a bit to 11.8%. Unfortunately, the reason behind this is not positive:

Community Health Options, a Lewiston-based health insurance cooperative, has gotten approval to withdraw from the New Hampshire insurance market in 2017.

The plan was approved this week by the Maine Bureau of Insurance, which has been monitoring CHO’s finances as it tries to recover from a $31 million loss in 2015. The nonprofit cooperative has set aside more than $45 million in reserves to try to avoid another big loss this year.

In 2014, CHO was the only cooperative in the nation set up to operate under the Affordable Care Act to turn a profit. But as it expanded in 2015, including a move into the New Hampshire market, its losses snowballed.

As of July 31, the insurer had 11,438 customers in New Hampshire and 65,188 in Maine. It has about 72 percent of the individual insurance market in Maine.

“Withdrawal from New Hampshire will allow Health Options to focus on its primary market in Maine and on rebuilding its reserves,” Maine’s insurance superintendent, Eric Cioppa, said in a statement announcing the decision. “In the past year, the company has worked to reduce expenses, improve operations and better align premium rates with claims experience. Consolidating their business is expected to further improve the company’s stability.”

The reason for the discrepancy between the 3,482 figure I had and the 11,438 number in the article is most likely because the higher number includes off-exchange enrollees. If so, this is highly unusual, since most of the other Co-Ops (which only came into existence since 2014 under the ACA) focus most of their efforts on exchange-based enrollment. However, this is a bit of a moot point since I now have to remove CHO from the New Hampshire spreadsheet entirely, giving a revised table like so:

CHO only has a small portion of the NH indy market, but they had been asking for a whopping 43% rate hike. By removing them completely, the weighted average for the other 4 carriers still participating in the market drops a bit...but it still means over 11,000 more people will have to shop around for new coverage.

On the other hand, unlike most of the other Co-Op woes, this one sounds like it really isn't too serious--they're really just reverting back to their original base in Maine, and there's a second Co-Op still operating in New Hampshire anyway (Minuteman):

In its latest update on CHO’s finances, the bureau said the cooperative is continuing to track closely to the plan laid out at the beginning of the year to restore its financial stability. It posted its second quarter results Wednesday.

Paid and incurred claims were both lower than the plan expected in July, and expenses were slightly higher than the plan for the month, but are lower on a year-to-date basis. The cooperative’s net loss for the month was 13 percent better than the plan, but is 5.6 percent worse for the year to date.

“In summary, CHO’s reported year-to-date results for 2016 business and operations through the first seven months of 2016 were generally consistent with its plan,” the bureau concluded.

Advertisement