Since then there have been two major changes: First, Aetna, which had been planning on entering the Maine ACA exchange, infamously pulled a complete 180 and not only decided not to expand, but actually pulled out of the exchange in most of the states they're already in. This doesn't really impact Maine since they were only available off-exchange anyway. The second change does, however: Several of the carriers submitted revised requests, pushing the average up higher, to 23.9%.

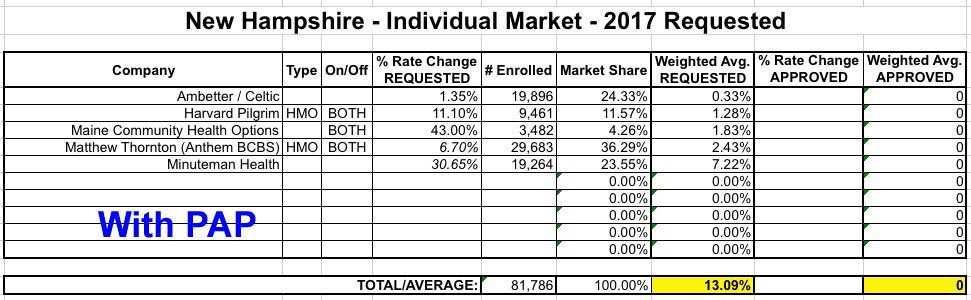

Community Health Options, a Lewiston-based health insurance cooperative, has gotten approval to withdraw from the New Hampshire insurance market in 2017.

The plan was approved this week by the Maine Bureau of Insurance, which has been monitoring CHO’s finances as it tries to recover from a $31 million loss in 2015. The nonprofit cooperative has set aside more than $45 million in reserves to try to avoid another big loss this year.

I appear to have something of a semi-exclusive here, if only because the Florida DOI isn't formally posting these documents on their website until tomorrow due ot the holiday weekend:

Office Announces 2017 PPACA Individual Market Health Insurance Plan Rates to Increase 19% on Average

TALLAHASSEE, Fla. – The Florida Office of Insurance Regulation announced today that premiums for Florida individual major medical plans in compliance with the federal Patient Protection & Affordable Care Act (PPACA) will increase an average of 19% beginning January 1, 2017. Per federal guidelines, a total of 15 health insurance companies submitted rate filings for the Office’s review in May. These rate filings consisted of individual major medical plans to be sold both on and off the Exchange. Following the Office’s rate filing review, the average approved rate changes on the Exchange range from a low of -6% to a high of 65%. This information can be located in the attached “Individual PPACA Market Monthly Premiums for Plan Year 2017*” document.

More than 75,000 Iowans will see their insurance premiums rise next year.

Iowa Insurance Commissioner Nick Gerhart has approved rate increases sought by four companies who provide health insurance in the state, Gerhart's agency announced Monday. The increases include plans covered by Wellmark Blue Cross & Blue Shield, the state's dominant health insurer.

However, the article was a little vague about some of the data, so I visited the IA DOI website and sure enough, they have separate entries for every one of the carriers (with one exception):

A week or so ago, I attempted to tally up the number of current ACA exchange enrollees who will have to shop around for a new policy this fall whether they want to or not, due to their current plan being discontinued. As a reminder, there are three main reasons for this: a) the carrier is pulling out of the exchange in their county/state (Aetna, Humana, UnitedHealthcare); b) the carrier is going out of business entirely (4 co-ops); or c) the carrier will still have policies available but is dropping the one they're enrolled in (mainly PPOs).

In addition to the 1.69 million estimate from Aetna, UnitedHealthcare, Humana and the 4 Co-Ops which are shutting down in CT, OH, IL and OR, we can also add the following (thanks to Louise Norris for the assist on some of these):

Believe it or not, Indiana's individual market situation is actually among the brighter spots this year. While three carriers are dropping off of of the ACA exchange market (and Physicians Health Plan is dropping off-exchange policies as well), they're also seeing the addition of a new carrier (Golden Rule), and one major carrier, Celtic, actually requested and received an average reduction in their monthly premiums, which is pretty rare this go around.

Unfortunately, the overall average approved statewide increase, while still lower than most of the other states so far, is actually slightly higher than the requested average. Every carrier got what they asked for with the exception of Indiana University, which asked for a 9.9% hike but was approved for a 14.9% increase. This bumped the statewide average up from 17.7% to 18.5%:

The average premiums range from an increase of 29 percent by Indianapolis-based Anthem Inc. to a decrease of 5.3 percent by Chicago-based Celtic Insurance Co.

Usually when state regulators publicize their approved rate changes for carriers on the independent market, they list the various carriers and the approved average rate changes for each. I then simply plug these into my existing spreadsheet and get a before/after comparison against how much the carriers actually requested.

In the case of illinois, it's a little trickier. Unless I'm missing something, the only official notice the IL DOI has released is this PDF, which--while including lots of useful info about rating areas and so forth--doesn't actually list the overall statewide average approved rate increases by carrier.

Instead, it lists the averages based on metal level, and even then doesn't list all of the plans, just selected ones: Lowest-price Bronze, Lowest and 2nd Lowest-price Silver, and Lowest-price Gold, like so:

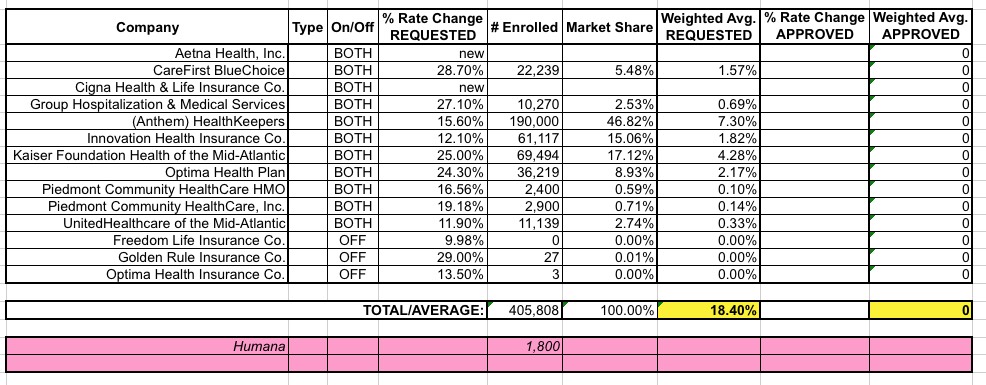

Virginia was the very first state which I ran an estimated 2017 average requested rate hike for, way back in mid-April.

Since then, aside from Humana pulling out (leaving just 1,800 current enrollees to find a new policy), Virginia's ACA exchange market has actually been remarkably calm; the state somehow managed to escape the wrath of both UnitedHealthcare and Aetna relatively intact, with both carriers still participating in the state's exchange next year as of this writing.

There have, however, been a few other changes to some of the rate filings here and there, found via this updated PDF on the VA DOI website as of July 19th. The overall average requested hikes don't really change much, but do nudge a bit higher than I had previously estimated, from 17.5% to 18.4%:

Physicians Health Plan of Northern Indiana announced Tuesday that it will quit selling individual insurance coverage next year through the federal Affordable Care Act.

The nonprofit PHP becomes the second insurer to announce it is leaving the HealthCare.gov insurance marketplace that serves residents of northeast Indiana. UnitedHealthcare said last spring it would drop out of the exchange in most states, including Indiana.

Four other insurers offered individual policies through HealthCare.gov this year in the Fort Wayne area and apparently will continue to do so in 2017. Insurers had until Tuesday to notify the state of their plans, and all four are among federal marketplace filings the Indiana Department of Insurance submitted Tuesday to the Department of Health and Human Services.

Fort Wayne-based PHP said it is paying $1.20 in medical expenses for every dollar it receives in premium payments from HealthCare.gov customers and has lost millions of dollars on the policies.

Following announcements by for-profit commercial carriers Humana and United Healthcare, nonprofits Health Alliance Plan and Priority Health are notifying agents they are pulling all PPO plans for 2017 from the Michigan health insurance exchange, Crain's has learned.

HAP has already announced it is pulling eight Personal Alliance individual preferred provider plans for individuals from the exchange and four PPO plans in the open market next year. HAP will continue to offer HMO individual plans on and off the exchange.

"We believe that these (PPO) plans do not represent the best value for the consumer," said Mary Ann Tournoux, HAP's senior vice president and chief marketing officer, in a statement. "At this time of cost-consciousness, we believe our remaining plans are the most cost-effective and offer our members and consumers greater value for their hard-earned insurance dollar."