About a month ago, when I first plugged in the average requested 2017 rate hikes for Georgia's ACA-compliant independent market, I came up with an overall weighted average of around 27.7%. However, there was one major gap in the data: I had trouble finding Ambetter/Peach State's enrollment numbers or even their average rate hike request, so I reluctantly left them out of the calculation completely.

When Aetna announced that they were dropping out of the Georgia exchange-based independent market, I went back and removed them from the mix. Since Aetna's request had been 15.5% on a substantial share of the market, this meant that the rest of the statewide average shot up to 32.0%.

Today I was able to track down the missing Ambetter/Peach State data--both the average requested rate hike (around 8.0%) as well as the number of current enrollees impacted...around 73,000:

OK. Last week I wrote up a post speculating about the potential impact to the state- and national-level average rate hike requests of Aetna dropping out of the ACA exchanges in 11 states. My conclusion was that the average will increase in some states...but may actually drop in others, since Aetna would otherwise have asked for rate hikes higher than the average requested by the other carriers in that state. Of course, this isn't really a positive development, since their current enrollees are still losing their plans entirely, and since a 50% hike from Aetna could still end up costing less than a 10% hike from one of the other carriers...but as always, this is the best I can do here.

According to a release from the company on Tuesday, the firm will no longer offer individual market plans through the Affordable Care Act in Dallas, Texas, and New Jersey.

..."We hope to return to these markets as we carry on with our mission to change healthcare in the US."

The "we hope to return" part suggests that Oscar will continue to be available off the exchange in New Jersey, since completely pulling out of a state means a carrier has to wait at least 5 years before re-entering. So...there's that, anyway.

...Oscar currently covers 7,000 people in Dallas and 26,000 in New Jersey.

As noted a couple of weeks ago, all three of the major insurance carriers participating in Tennessee's individual market ACA exchange asked for massive rate hikes this year, ranging from 44-62%. Blue Cross Blue Shield asked for 62% in the first place; Cigna and Humana resubmitted their original requests for higher ones.

Tennessee's insurance regulator approved hefty rate increases for the three carriers on the Obamacare exchange in an attempt to stabilize the already-limited number of insurers in the state.

...BlueCross BlueShield of Tennessee is the only insurer to sell statewide and there was the possibility that Cigna and Humana would reduce their footprints or leave the market altogether.

This was a double headache: First, because the actual enrollment numbers were only available for 3 out of 11 carriers via the filings; I had to get the rest from the MA exchange's monthly dashboard report. Secondly, even with the dashboard report, I had to merge together 2 different enrollment numbers for each carrier due to MA's unique "ConnectorCare" program.

There are a few states which have technically expanded Medicaid under the ACA, but have done so using an approved waiver which allows them to actually enroll expansion-eligible residents in private Qualified Health Policies (QHPs)...using public Medicaid funding to do so. To be honest, this has always struck me as being essentially no different than someone simply receiving 99.9% APTC/CSR subsidies for enrolling in an exchange policy anyway; it's just a question of which pool of federal funds the subsidies come from. The two states which I know for a fact do it this way are Arkansas and New Hampshire, with Arkansas calling their "Private Medicaid Option" program the "Health Care Independence Program".

In any event, AR "Private Option" enrollees may be categorized as "Medicaid expansion" in the official reports, but for purposes of estimating the risk pool, they're included in with every other ACA-compliant private individual policies, whether on or off the ACA exchange.

Amidst my Aetna Postapalooza yesterday, there's one important point which other outlets have brought up which I haven't addressed yet: Pinal County, Arizona.

Since participation in the ACA exchanges has always been voluntary for carriers selling ACA-compliant individual policies (except for the District of Columbia (and until recently, Vermont), where carriers are legally required to only sell individual policies via the exchange), there's always been the danger that sooner or later there might be a situation where no carriers are selling on the exchange. Not "a few", not "only one"...zilch.

In my mind, I've always thought of this problem in statewide terms; it wasn't until 2015 that I even realized that many carriers only sell policies in some of the counties in a given state, not all of them. That makes the list of 300+ exchange carriers nationwide a bit misleading; some of the carriers listed for a given state might only be selling in a few or just a single county, making the scenario above far more likely to happen.

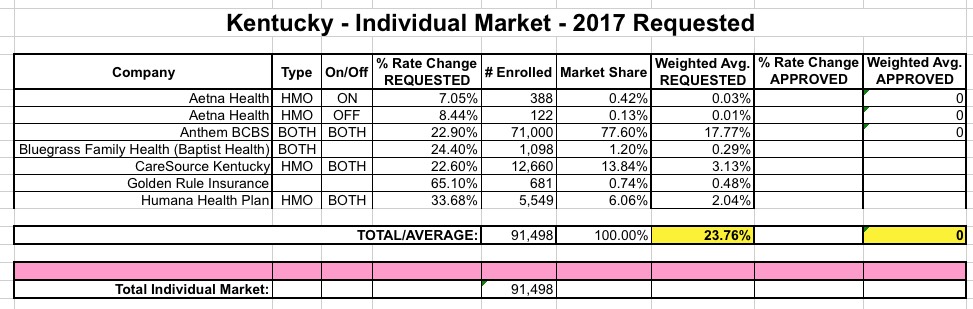

When I ran Kentucky's average requested rate hike numbers for the individual market back in May, I came up with a weighted average of 23.8%, but also cautioned that the weighting was likely based on less than 50% of the total ACA-compliant individual market state-wide.

Since then, it looks like a couple of the carriers resubmitted their filings with slightly different average requests, although nothing major. In fact, even Aetna dropping off the exchange doesn't change much, since it looks like they only have around 400 enrollees there anyway (plus, Aetna says they're sticking around the off-exchange market in "most" of the regions they're bailing on next year). Finally, as far as I can tell, Kentucky is among the states that Humana is not abandoning (though they might be reducing their footprint there?).

Anyway, just moments ago, according to SHADAC, the Kentucky DOI has posted their approved rates for the individual market:

(Updated to add Jeffrey Young to the headline/body...I missed his name on the byline originally, apologies to him!)

Ever since Aetna dropped the bombshell 10 days ago that they were abandoning their previously-announced intention of expanding into additional state ACA exchanges next year and instead might even drop out of some of the states they're already participating in, plenty of people have smelled something fishy about the timing of the 180º turn, given that the original expansion announcement came in mid-May, followed by the Dept. of Justice annoucing that they were suing Aetna to prevent them from merging with Humana in July.

Health insurer Aetna Inc. will stop selling individual Obamacare plans next year in 11 of the 15 states where it had been participating in the program, joining other major insurers who’ve pulled out of the government-run markets in the face of mounting losses.

Here's the full list of states Aetna is pulling up stakes in:

Arizona, Florida, Georgia, Illinois, Kentucky, Missouri, North Carolina, Ohio, Pennsylvania, South Carolina and Texas

Here's the 4 states where Aetna will still be selling exchange-based policies: