This week, HHS’s office of the Assistant Secretary for Planning and Evaluation (ASPE) is also releasing a report analyzing new survey data that showed the uninsured rate fell in 2021 after the American Rescue Plan and outreach efforts took effect. According to the report, the uninsured rate for U.S. population was 8.9% for the third quarter of 2021 (July – September 2021), down from 10.3% for the last quarter of 2020 – corresponding to roughly 4.6 million more people with coverage over that time period. Coverage gains occurred among both children and working age adults, with the largest coverage gains for those with incomes under 200% of the poverty level (roughly $27,000 for a single adult or $56,000 for a family of four).

A couple of years ago, Washington became the first state to implement their own "Public Option" ACA healthcare plan...sort of. The actual version of the PO which was implemented ended up being considerably less impressive than the original vision, but hey, it was a start.

Record Numbers of Washingtonians Sign Up for Health Care Coverage During 2021 Special Enrollment Period

LATEST DATA SHOWS IMPACT OF AMERICAN RESCUE PLAN ACT SAVINGS. NEARLY HALF OF ALL CUSTOMERS PAY LESS THAN $100 PER MONTH.

Washington Health Benefit Exchange (Exchange) announced on Tuesday more than 57,000 Washingtonians signed up for health care coverage between February 15 and August 15 on the state’s insurance marketplace, Washington Healthplanfinder. The Exchange opened a Special Enrollment Period in February in response to the COVID-19 Public Health Emergency. This allowed any individual in Washington the opportunity to apply for coverage or compare and upgrade their existing insurance.

CMS Thursday (July 15) announced a new advertising campaign that will run in the final 30 days of the special enrollment period slated to end Aug. 15, and the agency also confirmed Inside Health Policy’sreport that the agency plans to auto-adjust tax credits for consumers who do not return to the federal marketplace starting Sept. 1.

Oklahoma's Medicaid Expansion will Provide Access to Coverage for 190,000 Oklahomans

Nearly 120,000 People Will Begin Receiving Full Medicaid Benefits on July 1

The Centers for Medicare & Medicaid Services (CMS) announced today that approximately 190,000 individuals between the ages of 19-64 in Oklahoma are now eligible for health coverage, thanks to Medicaid expansion made possible by the Affordable Care Act (ACA). On June 1, 2021, the state began accepting applications, and to date, over 120,000 people have applied for and were determined eligible to receive coverage. On July 1, these individuals will receive full Medicaid benefits, including access to primary and preventive care, emergency, substance abuse, and prescription drug benefits. Thanks to the American Rescue Plan (ARP), Oklahoma is eligible to receive additional federal funding for their Medicaid program, estimated to be nearly $500 million over two years. It is estimated that an additional 70,000 people in Oklahoma who have not yet applied are now eligible for coverage under Medicaid.

The Washington Health Benefit Exchange (Exchange) reports that tens of thousands of Washingtonians now pay less each month for healthcare coverage. Within two months of the American Rescue Plan Act (ARPA) becoming federal law, the Exchange passed on the expanded savings it made available to new and current customers on the state’s insurance marketplace, Washington Healthplanfinder.

“There has never been a better time to sign up for healthcare coverage in Washington,” said Pam MacEwan, Chief Executive Officer of the Exchange. “We’ve been hearing from people across the state who are saving hundreds or in some cases more than a thousand dollars per month.”

Tracy Roberts from Seattle posted to Facebook, “I just opened my bill for July and it’s $242 less than I presently pay . . . That’s incredible! Absolutely incredible and completely unexpected. Life will be a little easier for now.”

This, again, is a Big Deal for this year. Paired with the beefed-up APTC table, what it means is that if you're on unemployment this year you effectively don't have to pay anything for a benchmark Silver plan. I'm not sure if you have to be unemployed for the full year or not...the wording above sounds like even someone who's only on unemployment for one or two weeks would still be counted as having 133% FPL.

Sure enough, just about anyone who is either currently receiving unemployment benefits or who did earlier this year (or later this year, for that matter) is likely eligible for a FREE ($0* Premium) Silver CSR 94 plan...otherwise known as #SecretPlatinum:

Sec. 9663 – Application of premium tax credit in case of individuals receiving unemployment compensation during 2021

For 2021, provides advanced premium tax credits as if the taxpayer’s income was no higher than 133 percent of the federal poverty line (FPL) for individuals receiving unemployment compensation as defined in section 85(B) of the Internal Revenue Code.

This, again, is a Big Deal for this year. Paired with the beefed-up APTC table, what it means is that if you're on unemployment this year you effectively don't have to pay anything for a benchmark Silver plan. I'm not sure if you have to be unemployed for the full year or not...the wording above sounds like even someone who's only on unemployment for one or two weeks would still be counted as having 133% FPL.

...there's also another small but critical detail included in the table above which escaped my attention last summer in H.R. 1425.

Take a look at the first line of Rep. Underwood's 2019 version (H.R 1868):

Over 100.0 percent up to 133.0 percent

Now take a look at the first line under both H.R. 1425 and H.R. 369:

Up to 150.0 percent

Notice the difference? I'm not talking about the "up to 150%" part. I'm talking about the removal of the "Over 100.0 percent" part.

If this were to pass the House & Senate and be signed into law by President Biden using this exact language, it would apparently eliminate the Medicaid Gap...albeit with a couple of major caveats.

Single Parent; Nuclear Family; Empty Nesters w/College-age kid; 60-yr old couple

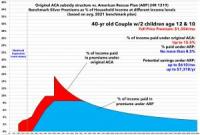

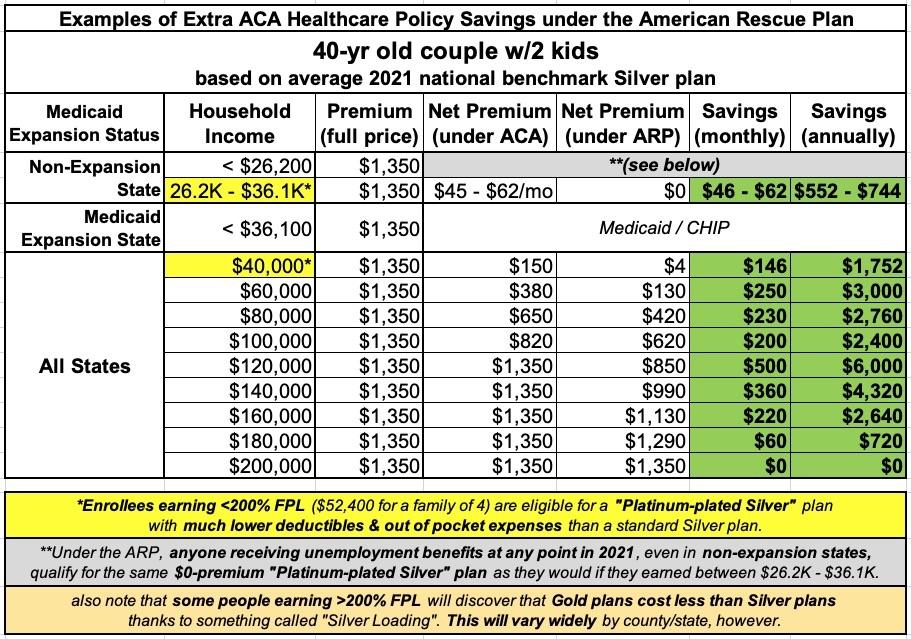

Here's how much the "Nuclear Family of four" example (40-yr old ocuple with 2 children) would theoretically save, assuming they choose the avg. national benchmark Silver plan: